Frequently Asked Questions

Find answers to common questions about our credit repair services, pricing, policies, and processes.

We Assist in the Removal of

A hard inquiry (also called a hard pull) is when a lender checks your credit report because you applied for credit.

A collection account is a negative credit item that appears when a bill goes unpaid for a long period and the original creditor sends or sells the debt to a collection agency.

A late payment on a credit report is a negative mark that shows you didn't pay a credit account on time according to the lender's due date.

A student loan is borrowed money used to pay for education that you must repay—with interest—after (and sometimes during) school.

An eviction is a legal process where a landlord forces a tenant to move out of a rental property—usually because the tenant violated the lease or failed to pay rent.

A medical bill is a charge you receive for healthcare services that were provided to you—but not fully paid for by insurance (or not insured at all).

A charge-off account is a debt that a lender has decided is unlikely to be collected, so they mark it as a loss in their accounting—but you still owe the money.

A repossession (often called a repo) happens when a lender takes back property you're financing—most commonly a car—because payments weren't made as agreed.

A bankruptcy is a legal process that gives a person or business relief from overwhelming debt when they can no longer afford to pay what they owe.

A public record on a credit report is a negative legal or financial event that comes from court filings or government records and is reported to the credit bureaus because it involves unpaid obligations or legal responsibility.

ChexSystems is a consumer reporting agency that banks and credit unions use to decide whether to approve or deny you for a checking or savings account—not loans or credit cards. Think of it as a credit report for bank accounts.

Early Warning Services (EWS) is a consumer reporting agency used by banks to decide whether to approve you for checking and savings accounts and to monitor for fraud. It's similar to ChexSystems—but more powerful—and is heavily used by major banks.

Debt consolidation is a financial strategy where you combine multiple debts into one single payment, usually with the goal of lowering your interest rate, reducing your monthly payment, or simplifying your finances.

Chexsystems / Early Warnings (Sold Separately) — $500 Each Individually | $750 For Both Total Combined = $250 OFF

What Are Your Business Hours?

I do not answer random calls or text messages. The majority of commonly asked questions are already addressed in the Education Tab and FAQ Section on my website.

Most calls naturally turn into full consultations. My time and expertise are both valuable. Therefore, I reserve my time for individuals who are serious and prepared to move forward.

My website has all the information you may need. Additionally, you may utilize the Support Chat Box, conveniently located on the bottom right-hand side of the website, for faster responses or further assistance.

How Much Do You Charge?

My pricing is determined by the number of negative items appearing on your credit report, which means the total cost varies for each individual. To ensure accuracy and fairness, every client is required to book a consultation for $63 before receiving a personalized quote.

Consultation Breakdown:

• $30 covers the consultation itself, compensating me for my time and expertise

• $33 covers your enrollment in the credit monitoring service I use for all clients

Both are mandatory steps to begin the process.

If this arrangement does not work for you, I completely understand—however, it may mean we're not the best fit to work together at this time.

Sales Exception: During promotional periods or sales, the price will be set at one flat rate regardless of how many negative items appear on your report, and a consultation will not be required.

If you're serious about improving your credit, the first step is booking your consultation.

Do You Accept Payment Plans?

I accept Afterpay, Klarna, and Zip as flexible payment options.

For clients requesting a traditional payment plan, I only accept payments through an invoice that allows you to securely place your card on file for automatic billing.

Important: To avoid any discrepancies or missed payments, I strongly recommend using a card that is not locked or restricted in any way. This ensures payments process smoothly and services continue without interruption.

When a payment agreement is established with a defined timeline, it is essential that the terms of that agreement are honored.

The fee charged covers the entire credit improvement process, not an individual dispute round. While payment plans are not required, one was extended as a courtesy.

If a scheduled payment is missed, all work on your account will be paused immediately, and no updates will be provided until the outstanding payment has been received.

If our team attempts to contact you regarding a missed payment and does not receive a response within 24 hours, the process will be fully suspended. In order to resume services, the remaining balance must be paid in full.

CLEAR UNDERSTANDING:

The amount you were charged represents the cost of the entire process. Any work completed up to that point is considered final and non-refundable.

This is similar to financing a vehicle. When you enter a financing agreement—for example, over a five-year term—you are expected to fulfill the agreed-upon payments for the duration of that contract.

Even if you make payments consistently for 3 years, failure to continue those payments can result in consequences such as the vehicle being disabled (in some newer models), repossession, and potential negative reporting to your credit.

The payments already made are not refunded, as they covered the time and usage of the vehicle during that period.

Now granted you're not buying a car, but I expect the same level of respect for my business. You wouldn't call the dealership and mention how you've already made payments for 3 years in a row. Because you understand you've broken the agreement so they no longer have to give you access.

Likewise, in this process, payments made reflect the services rendered up to that point. Therefore, they are not eligible for reimbursement, And I am not required to continue service at that point.

Once services have been stopped due to missing payments—the remaining balance must be PAID IN FULL, In order to resume services.

These policies are not personal. They are necessary to protect the integrity of our business operations and ensure fairness across all client accounts.

Book A Consultation

Your credit transformation journey begins with a strategic consultation. Book your personalized session to discuss your current credit situation, explore your goals, and map the precise path to achieve exceptional results.

The consultation fee is $63 which covers:

- $30 for the consultation itself, compensating for time and expertise

- $33 for your enrollment in the credit monitoring service

Book Your Consultation

$63

One-time consultation fee to begin your credit repair journey

- Personalized credit analysis

- Custom action plan

- Credit monitoring enrollment

- Direct access to The Credit Daddy

IMPORTANT:

After you make the payment it will automatically redirect you to my booking link. PLEASE READ THE DESCRIPTION IN THE BOOKING LINK AND DO THAT PART FIRST‼

Once that part is completed you can then finish filling out the questionnaire to book your appointment.

Please choose the best time where you will have the LEAST AMOUNT OF DISTRACTIONS.

Talk to you soon! 🙌

Important Consultation Guidelines:

• All Consultations Are NON-REFUNDABLE

• You will be granted a 5 minute GRACE PERIOD. Anything after that will put me behind for the day and we will be forced to reschedule.

• If you need to reschedule, please let me know ahead of time.

• You may RESCHEDULE for FREE but a NO-CALL-NO-SHOW will result in a $50 Fee for your next appointment.

What Does The Consultation Consist Of?

Setting Expectations:

I understand you may feel like “you already know how this works” or “you don’t need this part.” However, there is a huge difference between KNOWING AND UNDERSTANDING. 97% of my clients come to me for help, which means there is something holding them back—otherwise, they wouldn’t be here.

Additionally, over 70% of Americans struggle with their credit, and that statistic cannot be ignored. Because of this, I approach every consultation as if you are starting from zero, ensuring nothing is overlooked.

How the Process Works:

- You will book a consultation, and I will ask you what your financial goals are. I will then explain why credit is the foundation to reaching those goals—regardless of what they may be.

- I will go over Myths & Facts About Credit, covering some of the biggest misconceptions most people have.

- During the consultation, we will review your credit report TOGETHER via Zoom or FaceTime. Transparency is key—I want you to see everything in real time, so you never feel like anything is being exaggerated or misrepresented.

- I will share my screen and walk you through what a GOOD credit report should look like vs. what YOUR current report reflects 🔎

- We will identify what is actually holding your profile back and discuss how I can assist you in improving it.

- I will also physically show you the financial impact of bad credit vs. the savings potential of good credit, so you clearly understand what’s at stake.

- At the end of the consultation, if you decide to move forward, I will provide a customized price based on your specific credit report, and we can select a start date from there.

How Does The Process Work / What's Included?

- We send out customized letters to the credit bureaus to challenge for removal of negative items off your file and clean up your report. Things like charge-offs, collections, late payments, inquiries, derogatory, evictions and even repossessions.

- You will be required to pay $33/month to monitor your credit until we're done with your profile. It's like a credit karma but it's more accurate and shows everything we need to see.

- Each round takes 45 days for updates and results! (approximately one and a half months) You will have access to your own personal portal to track the progress as we go! 24/7 access!

Step 1: Credit Repair

My primary responsibility is to dispute inaccurate, unverifiable, and negative items on your credit report. That is the service you are paying for.

Step 2: Credit Growth

In addition, I provide all clients with guidance on how to properly build and maintain their credit scores by giving them a TO DO LIST.

Step 3: Profile Building

I also coach clients on how to develop a strong credit profile and assist with applying for credit cards when the timing is appropriate. THIS IS ALSO INCORPORATED WITHIN THE TO DO LIST.

Step 4: Execution

This is when I assist clients who are ready to pursue business funding or apply for major financing such as a home or vehicle. While this level of involvement is not required of me, I choose to provide it because I genuinely care about my clients' long-term success.

It's important to understand that a 750 credit score alone does not automatically mean you have GOOD CREDIT. True credit strength consists of:

- A good score (typically 720+),

- A clean credit report, and

- A strong overall credit profile.

Step 5: LLC Setup / Business Funding (BONUS)

Regarding business credit, I educate clients on how to properly set up an LLC, establish relationships with banks, and position themselves to qualify for business funding. My goal is to teach clients how to apply independently. However, if you choose to have me assist directly with applications, I charge a 10% success fee based on the approved amount.

I also work with relationship managers at major institutions, including Chase, U.S. Bank, PNC Bank, Truist, Citizens Bank, the SBA, and American Express. These relationship managers are the individuals who actually review and approve applications, and I refer my clients directly to them. Additionally, I offer tradelines & shelf corporations, which function similarly to tradelines but for an LLC.

All of this is included but understand what you are paying for is CREDIT REPAIR — the process of cleaning and correcting your CREDIT REPORT. When it comes to creditworthiness, your credit report is what gets you approved — not your credit score.

When Will I Start Seeing Deletions & How Long Does Credit Repair Take?

I can't give a specific timeframe for a few reasons:

- Often times clients hold themselves back with the process by not keeping their credit monitoring up to date.

- They don't check their emails for instructions and they don't send in their most recent proof of address every month — and we need that in order to dispute on your behalf.

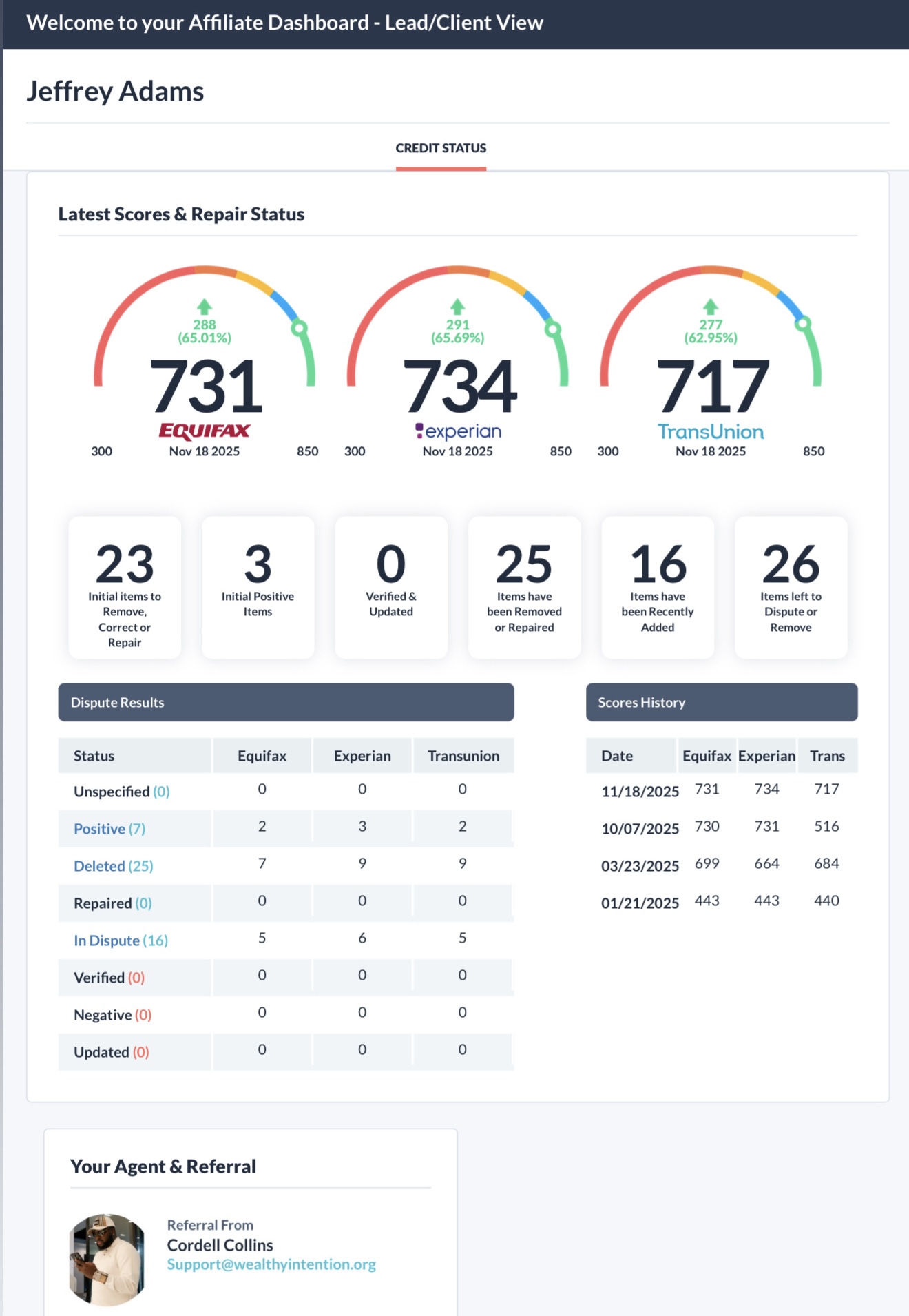

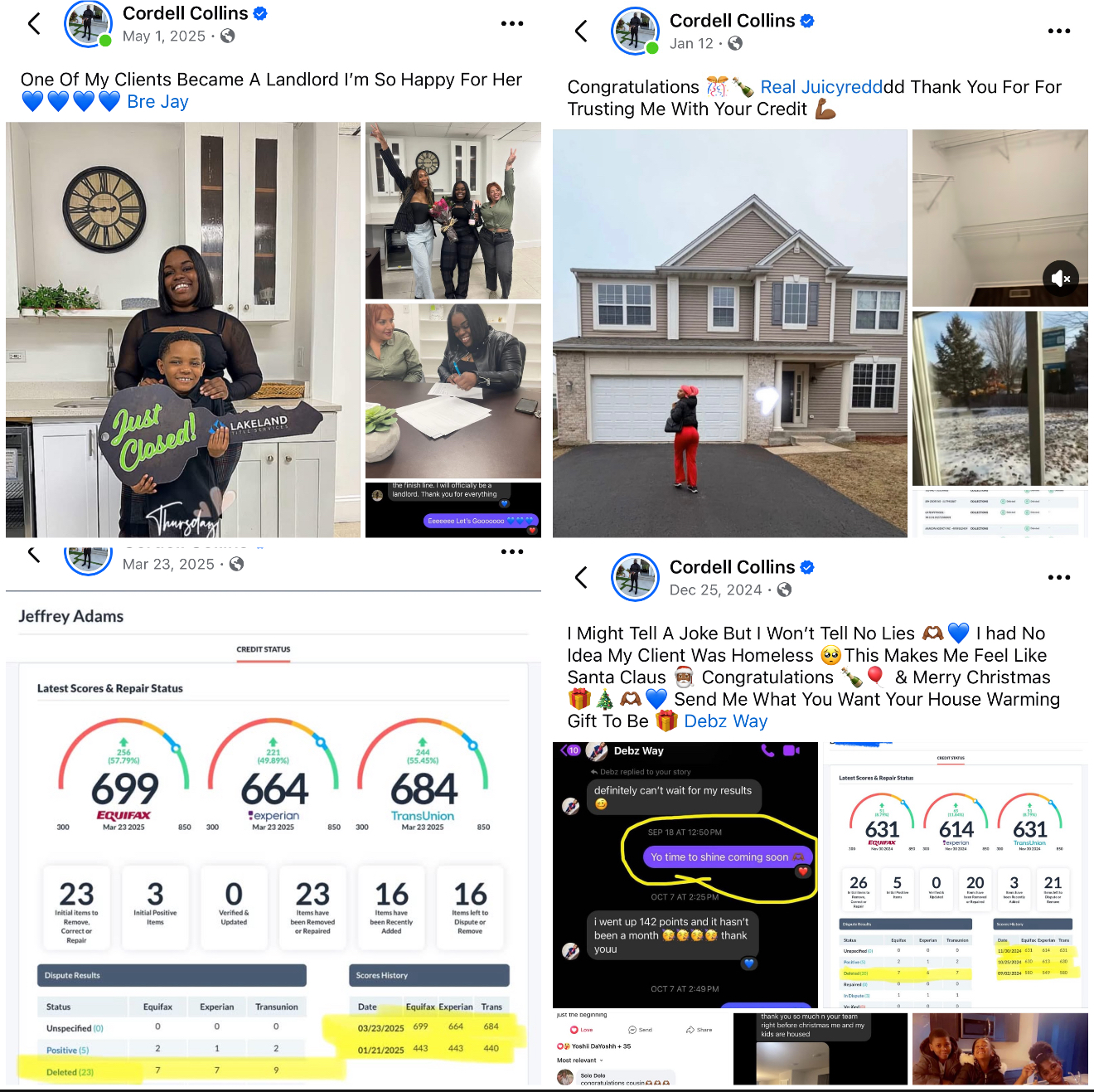

If you look at the screenshot above, you'll see that this client started with 23 negative items and we actually got 25 negative items deleted. Which means 2 additional negative items appeared after he started, and we got those removed as well — resulting in a completely clean credit report.

If you pay attention to the dates on the right-hand side, you'll see this client started Round 1 on 1-21-25 and Round 2 on 3-23-25. However, the next round did not begin until 10-7-25. From the outside looking in, it may appear that no work was done for 8 months, but that is not the case.

In most situations, delays like this happen because the client either did not maintain their credit monitoring subscription (which prevents me from accessing your credit report), or the client failed to submit an updated Proof of Address (POA) every single month.

Please understand, every time dispute letters are sent, we must verify your identity. Your Proof of Address is required for every round, and if it is not provided, I cannot proceed with the next round of disputes.

These two things alone can prolong a client's results for months or even up to a year — which would not be my fault as long as I send out emails and texts notifying them. So his total timeframe took a total of 10 months. 10 months, although it could have potentially been significantly shorter without delays.

On top of that, the credit repair timeline varies from person to person, depending on the number and type of negative items on the credit report.

Success Stories:

• Fastest deletion: Eviction removed in just 14 days

• Quickest full clean-up: 88 total negative items cleared within 45 days

That said, results like these are possible but not typical and cannot be guaranteed for every client — no one in this industry can honestly make such a promise. If they do, they're telling you what you want to hear so you feel comfortable enough to give them your money because they know you're in a rush & most likely desperate.

Realistic Expectations:

On average, credit repair takes 6 to 9 months, and in more severe cases, it can take up to a year.

I believe in full transparency: credit repair should take as long as it needs to take. Anyone guaranteeing complete results in 30–60 days is not being realistic. The average client goes through 4–7 rounds of disputes. If it were that simple, multiple rounds of disputes wouldn't even exist.

Unfortunately, many companies lie for sales, which gives credit specialists a bad reputation. My approach is different — I prefer honesty over hype. MY NAME IS MORE IMPORTANT THAN YOUR MONEY! I will let anyone walk before I tell them what they want to hear. It's not about what you want — it's about how the process actually works. Results take time, but they do come. Will it take the full 6–9 months, or even a year? Not necessarily, but you should be prepared for that timeframe.

Each dispute round lasts approximately 45 days, and after every round, you will receive a detailed PDF update outlining any deletions or changes that occurred.

See Real Results:

If you click this link you can look at the credit scores and deletions for some of my clients and kind of do the math on how long it took — do with that what you will. Also, a lot of the shares are from some of my real clients.

www.TheCreditDaddy.com/results

Inquiry Removal Pricing

Individual Inquiry Removal: $50 per inquiry

24 Hour Inquiry Removal: $150

Inquiry Removal Packages

New Negative Items Policy 🚨

When you begin the credit repair process, my goal is to dispute and address all negative items currently listed on your credit report.

Important Notice

If new negative items appear during the process — such as new collections, inquiries, or late payments — please understand that I am not required to work on those new items.

I do understand that sometimes accounts report later than expected, and I'm always willing to work with clients in good faith to keep them on track. That said, this is a professional courtesy, not an obligation.

Please note:

- Continuously applying for new credit or creating new inquiries during the repair process works against your progress and creates additional work that makes my job significantly harder.

- If we've already discussed the importance of keeping your accounts positive and you still receive new negative items, an additional charge may apply for continued credit repair services.

- If I decide to charge for additional work, I will inform you first and ask whether you wish to move forward.

- If you choose not to, all work on your file will be paused or stopped entirely.

Can You Help With ChexSystems & Early Warnings Removals?

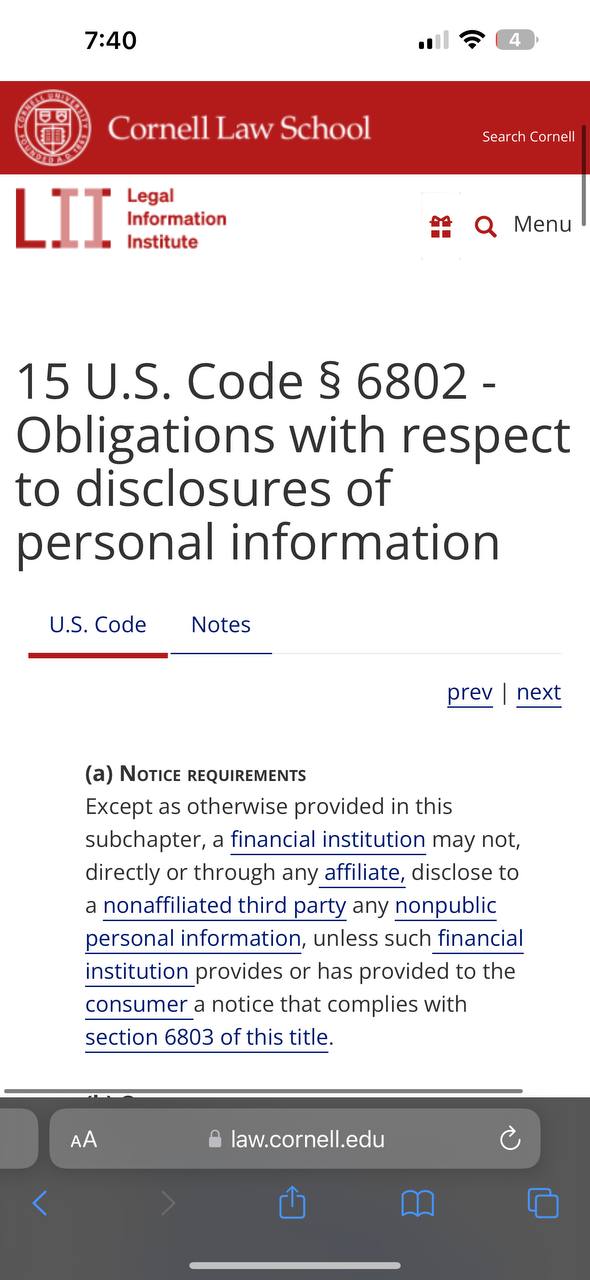

If you are in ChexSystems or Early Warning then that means that you have been violated. Read 15 USC 6802 - 15 USC 6805. If you read your terms and conditions and privacy agreements of your credit card accounts and banking information, it tells you that they do not share your personal information with any 3rd party non-affiliate…

Third Party Non-Affiliates Include:

• Lexis Nexis

• Experian

• Equifax

• Transunion

• Early Warning System

• ChexSystems

What we don't realize is when we open up these accounts, we have the option to opt out so they don't share our information — but they don't outright tell us that in plain English either. In their privacy agreements and terms and conditions, it states that they don't share your info, but yet they do anyway, which is a violation.

Request your consumer report from both websites & send me over the PDFs once you receive them.

ChexSystems:

https://www.chexsystems.com/request-reports/consumer-disclosure

Early Warnings:

https://www.earlywarning.com/faqs-requesting-your-file-disclosure

ChexSystems Customer Service: 800-428-9623

Early Warnings Customer Service: 800-745-1560

Representatives are available to assist during normal business hours 8AM to 7PM Central Time, Monday - Friday excluding federal holidays.

Payment Requirements:

• Payments must be paid IN FULL before we begin the process

• Afterpay, Klarna, and Zip are acceptable

After that, we will mark up any information you do not recognize or whatever is negative and start the disputing process. This process can take up to 3 months.

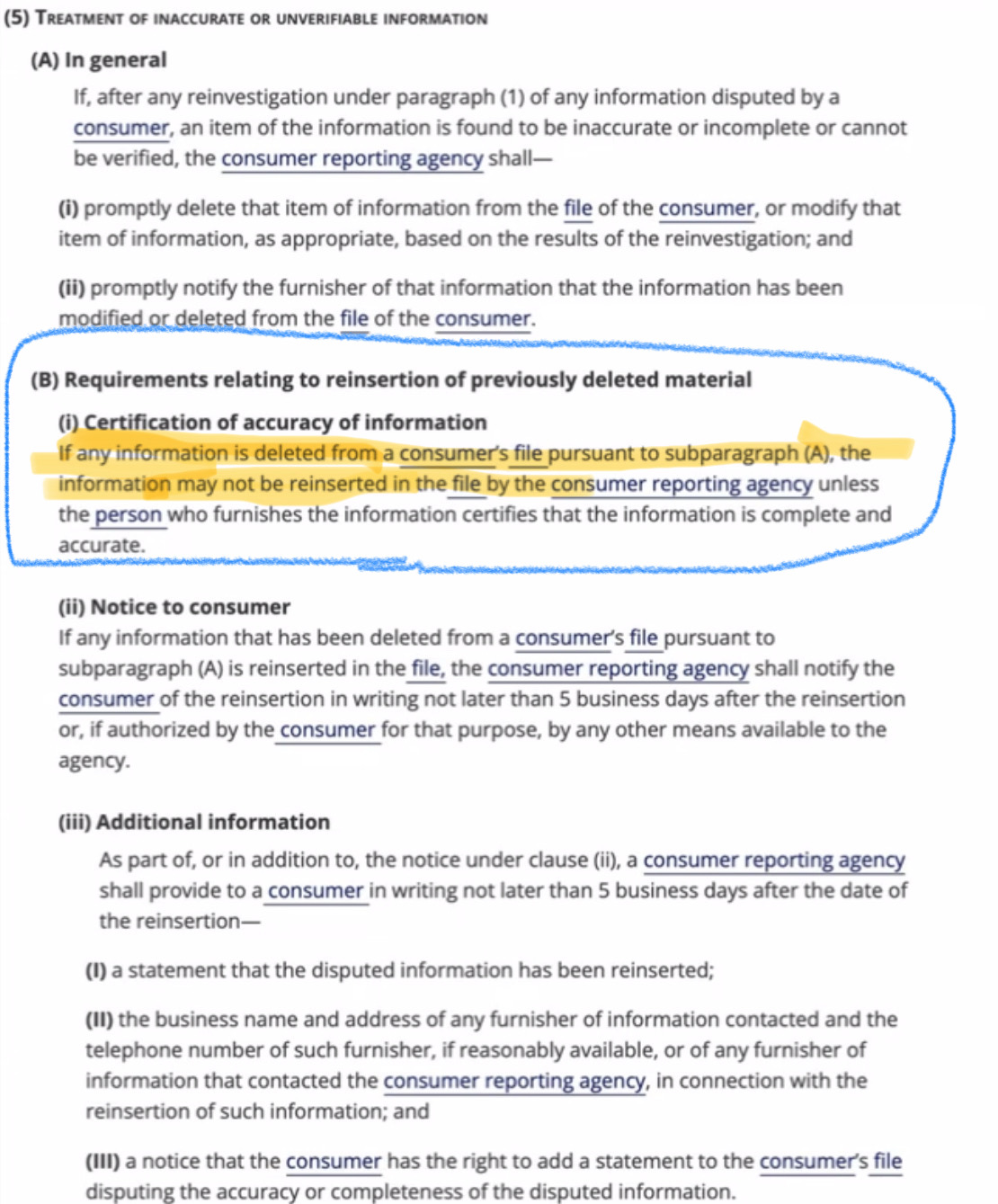

Can a Deleted Item Come Back on My Credit Report?

Credit Repair DOES NOT DELETE THE DEBT! — it only removes inaccurate, unverifiable, or outdated negative items from your credit report. However it is still important.

Think of it like a record expungement: the event happened, but lenders can no longer see it when reviewing your credit. This allows you to qualify for approvals you may have been denied before.

Important to Understand:

You may still owe the original creditor, and it would be smart to settle with them after the deletion—especially since most companies would require payment or settlement if you want to do business with them again.

However, once the item is removed from your report, it no longer holds you back from getting approved by other companies when viewing your credit report.

Once an item has been deleted from your credit report, the credit bureaus are not supposed to reinsert it. However, in some cases, if the debt remains unsettled, a creditor or collection agency may attempt to re-report the account—often assuming that consumers are unaware of their rights under the Fair Credit Reporting Act (FCRA).

Active Client Protection: If you are an active client and a previously deleted item reappears, we will dispute it again at no additional charge during your next dispute round.

After Program Completion: If you've completed your program and chose not to settle the debt, and the item later reappears, there will be a fee to reinitiate credit repair services—especially since you are being informed upfront about the possibility of re-reporting.

What Is A Debt To Income Ratio?

Debt-to-Income Ratio (DTI) is a simple but very important number lenders use to decide whether to approve you, how much to approve, and what terms you get.

Your DTI is the percentage of your gross monthly income that goes toward monthly debt payments.

In short: It tells lenders how much of your income is already spoken for.

DTI Ranges:

- Under 36% — Excellent. Most lenders consider this healthy

- 36%–43% — Acceptable for most conventional loans

- 44%–50% — Risky. Some lenders may require compensating factors

- Over 50% — Most lenders will decline

Formula: Total Monthly Debt ÷ Gross Monthly Income × 100 = DTI%

What Is The Difference Between Payment History & Credit History?

These two terms sound similar but they measure completely different things on your credit report. Understanding the difference is key to understanding your credit score.

FREE GAME ✍🏾 Bold Wordings = What Banks & Lenders Like To See 👏🏾

PAYMENT HISTORY = 35% Of Your Score

It answers the question: How Often Do You Pay Your Bills On Time when you owe?

Is It 20%, 50%, 80% Or 100% Of The Time? Meaning You Pay Your Bills On Time Every Month?

Payment History is the most important factor in your credit score.

CREDIT HISTORY (AKA Credit Age) = 15% Of Your Score

It answers the question: How Long Have You Been Establishing Credit?

Has It Been For 3 Months, 6 Months, 1 Year, 3 Years, Or 5 YEARS OR MORE?

• Calculated based on the average age of all your accounts

• Older = better for your score

Key Takeaway

Together, these two factors alone count for 50% of your total credit score.

Should I Close Credit Card Accounts I Don't Use?

❌ In most cases — NO. Do not close old credit cards.

Closing a credit card hurts your score in two ways:

- Increases your utilization — You lose that card's available credit limit, which raises your overall utilization ratio

- Reduces your credit age — Old accounts help boost your average credit history. Closing them makes your profile look younger to lenders

When It MAY Make Sense To Close:

- The card has a high annual fee and you get no benefit from it

- The account is relatively new (opened within the last year)

- You genuinely cannot control spending on it

Best practice: Keep old cards open, use them for a small recurring charge (like a Netflix subscription), and set it on autopay. Free credit history maintenance.

Would It Be Better To Just Pay My Collections Off?

The Smart Approach

Nothing wrong with settling a debt. It's just WHEN you settle it. Please allow me to explain.

- If you're ever behind on an OPEN ACCOUNT — yes, it is safe to get on a payment plan to pay it down.

- But if that account has already been closed & sent to collections, it's better to get it removed FIRST & then settle the debt.

- Even if you have to send them $20/month, I doubt they respond saying they no longer want the money. Especially since most companies require payment or settlement if you want to do business with them again.

- But if you pay them first, you'll find out the hard way that YOU STILL NEED TO GET IT DELETED — and you will be mad.

9/10 if you have a collection, your information has been passed on to a 3rd party debt collector that you NEVER did business with — so therefore you DO NOT OWE THEM ‼️

Why pay a company you don't owe?

Even if it were the original creditor, paying them DOES NOT REMOVE IT FROM YOUR CREDIT REPORT.

Every state has a statute of limitations on when a creditor can collect on a debt 💸. A lot of times consumers don't realize they're almost scot-free of paying a debt — but when they make a small payment, THE CLOCK STARTS OVER.

If you fall for that letter saying "Pay 30-40% off and we will SETTLE this for you," it will still be on your credit report as a Paid Collection / SETTLED FOR LESS THAN FULL BALANCE — which is still a negative account and DOES NOT help you.

Not only were you already behind 120-180 days, but when you finally decided to pay them, they didn't even get all of their money? It doesn't look good.

If you pay them IN FULL, it will still show up as a PAID COLLECTION — which is still a negative account and DOES NOT help you.

But What's The Problem If I Paid It?

Short Answer: Paying a collection DOES NOT HELP YOUR CREDIBILITY.

Example: I go to jail for stealing money out of Walmart's register. I do my time for it. When I get out of jail, I apply to work for Chase Bank. Do you think they'll hire me? I can't say "But I went to jail for it" because something like that should never have happened to begin with.

No different here. How the banks look at you: if you defaulted on your agreement several times already, what makes this time different? Would you continuously lend money to someone who never pays back on time?

Fun Fact: Every State Has A Statute Of Limitations On Debt Collection

Each state sets different time limits for different categories of debt. The clock doesn't run the same for everything.

Common Debt Categories That Matter (Illinois Example)

| Debt Type | Why It Matters | Statute Of Limitations |

|---|---|---|

| Written contracts | Credit cards, personal loans, auto loans | 10 years |

| Oral (verbal) contracts | Handshake agreements | 5 years |

| Open-ended accounts | Credit cards, lines of credit | 5 years (commonly argued) |

| Promissory notes | Student loans, auto loans, personal loans, installment loans | 10 years |

| Judgments | Court-ordered debts (completely different rules) | 7 years (renewable) |

How Statutes Of Limitations Actually Work

Each category can have a different statute — even within the same state.

What Starts The Clock? The statute of limitations clock usually starts at:

- Date of first delinquency (DOFD)

- OR date of last payment (varies by state & debt type)

⚠️ Any of the following can RESET the clock:

- Making a small payment

- Acknowledging the debt in writing

- Entering a payment agreement

If the statute of limitations has already surpassed, the only thing you really need to do is get the negative item deleted from your credit report so other lenders won't see the debt.

A lot of times consumers don't realize they're almost scot-free of paying a debt. When creditors & debt collectors convince you to get on a payment plan and you make that first small payment, THE CLOCK STARTS OVER.

This is why clients should NEVER casually agree to pay old debt without advice. If you pay them, it will be harder to get removed because now you look guilty. Why would anyone pay a debt that doesn't belong to them?

You may receive letters & emails threatening to garnish your check or sue. It's all a bluff to scare you into paying.

Ready to Get Started?

Your credit transformation journey begins with a strategic consultation. Book your personalized session to discuss your current credit situation, explore your goals, and map the precise path to achieve exceptional results.

Whether your focus is repairing your credit, removing negative items, or building a stronger financial foundation, our tailored approach delivers solutions calibrated specifically to your unique circumstances.

The consultation fee is $63 which covers:

- $30 for the consultation itself, compensating for time and expertise

- $33 for your enrollment in the credit monitoring service

Click the button below to pay your consultation fee and take the first decisive step toward financial freedom!

Book Your Consultation

$63

One-time consultation fee to begin your credit repair journey

- Personalized credit analysis

- Custom action plan

- Credit monitoring enrollment

- Direct access to The Credit Daddy

IMPORTANT:

After you make the payment it will automatically redirect you to my booking link. PLEASE READ THE DESCRIPTION IN THE BOOKING LINK AND DO THAT PART FIRST‼️

Once that part is completed you can then finish filling out the questionnaire to book your appointment.

Please choose the best time where you will have the LEAST AMOUNT OF DISTRACTIONS.

Talk to you soon! 🙌