Active Client Tab

The purpose of the Active Client Tab is to provide guidance and set clear expectations throughout your credit restoration journey. This section contains important information designed to help you understand the process and what to expect moving forward.

Please take the time to carefully review each category in full, rather than skimming or skipping sections, as many common questions are addressed here. If you have a question, we encourage you to review this page first. If you are unable to locate the information you need, you are welcome to schedule a free consultation for further assistance.

Tab Categories

Choose a category below to access specific information, guidelines, and resources

Book A Consultation

How To Contact Me

Please DO NOT message me on social media. Also Most of the time i am completely booked so I DO NOT answer random phone calls. This dropdown will explain exactly how to get in contact with me if needed.

Rules & Expectations

Payment agreements, service policies, refund terms, and important client obligations.

Things That Can Hold You Back

(THINGS YOU SHOULD BE DOING ON YOUR END)

Common issues that delay results and how to avoid them. Stay on track with your credit repair journey.

Frequently Asked Questions

Get answers to common questions about the credit repair process, timelines, and what to expect.

Educational

Learn about credit scores, reports, and profiles. Understand how credit works and how to improve it.

TO DO LIST

(THINGS YOU SHOULD BE DOING ON YOUR END)

Action items to help boost your credit score, including recommended credit building accounts.

TO DO LIST ZOOM RECORDINGS

Access recorded Zoom sessions and walkthroughs to guide you through your to-do list steps.

Resources

Links, tools, and additional resources to support your credit repair journey and financial growth.

Refer A Friend

Know someone who needs credit repair? Refer them and earn rewards when they sign up.

Tap the gift box to share your ideas

Book A Consultation

Schedule consultations and learn how to contact our team

How To Contact Me

My Schedule & Business Hours

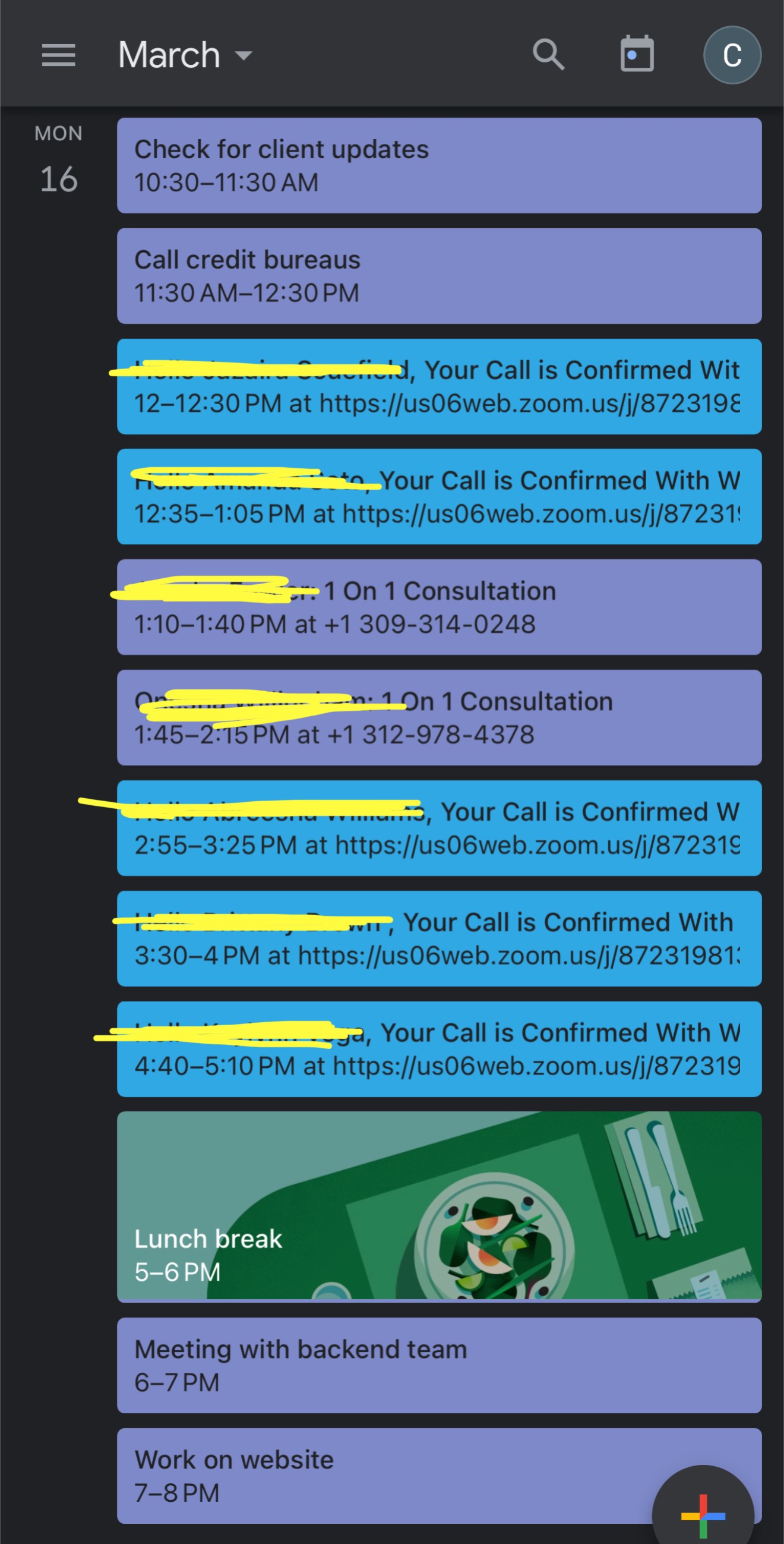

The screenshot above reflects my current calendar availability. As shown, my schedule is typically fully booked.

⏱ Business Hours: 12:00 PM – 5:00 PM CST — Monday through Thursday

Not available during ALL HOLIDAYS

These are the official business operating hours for both myself and my staff. These hours should NOT be confused with personal assumptions of what may be considered standard business hours or appropriate availability.

Please note that both my phone and this timeframe is exclusively dedicated only to clients who have taken the time to book a consultation and is not monitored for general text messaging or random calls.

During consultations, my phone is placed on “Do Not Disturb” to ensure each client receives my full, undivided attention. Responding to messages during scheduled appointments would be both unprofessional and unfair to those who have reserved that time.

My website has all the information you may need. Additionally, you may utilize the Support Chat Box, conveniently located on the bottom right-hand side of the website, for faster responses or further assistance. I also have a Suggestion Box if you feel there is any information that should be added to my website.

Boundaries & Rules

Everyone should have my Booking Link, the Support Number, and Support Email. These are the proper channels for all business communication.

- Please DO NOT call after 8:00 PM (Central Standard Time) under any circumstances. While calls outside of business hours are already discouraged, contacting me after this time is completely unacceptable.

- It is important to respect my personal time and professional boundaries, as well as my private life and relationships.

- Please DO NOT CONTACT ME through social media regarding business matters. In many cases, social media usernames do not match a client's legal name, making it difficult to properly identify who I am communicating with.

- Additionally, if I am active on social media outside of my business hours, that time is reserved for personal use. I am not available to discuss business matters during that time. Especially Friday–Sunday & ALL HOLIDAYS. For all business-related inquiries, including all QUESTIONS, COMMENTS, & CONCERNS, please use the appropriate booking link or official communication channels.

- As an active client, you are entitled to schedule consultations at no additional cost. Thank you for your understanding and cooperation.

Outside Of Operating Hours

Outside of MY business hours, both my staff, and also me myself will be unavailable and do not have access to my business phone. Especially Friday–Sunday & ALL HOLIDAYS. For this reason, it is important to book a consultation to ensure your questions and concerns are properly addressed in a timely and professional manner.

If questions arise outside of business hours, please take note of your questions and schedule an appointment for the next available time slot to ensure they are properly addressed.

I Work Late & Am Unavailable During Business Hours

If you have a late work schedule and are unavailable during standard business hours (Monday–Thursday, 12 PM–5 PM), I am willing to accommodate after-hours consultations.

However, I kindly ask that you provide at least 24 hours' notice to arrange this accommodation.

For example, if today is March 28th (Saturday) — a non-business day where neither myself nor my staff are available — please follow the steps below:

Step 1: Write down your questions to ensure nothing is missed.

Step 2: Book a consultation for the latest available time slot on the next business day (e.g., Monday, March 30th).

Step 3: Text the support number 312-584-9969 to request the specific time you prefer for that day.

All after-hours requests must be scheduled in advance • Requested times must be after 5 PM • Not available before 12 PM

Expectations

What I expect from each client is to schedule an appointment whenever they have any Questions, Comments, Concerns, Or Just Need Assistance. For example, if you've reached a specific step or reviewed a recording and need clarification, you can book a consultation and say, "I'm currently on Step 3 and need help understanding a certain part."

In those situations, I am more than willing to take the time to walk you through everything in detail and stay on the call as long as needed to ensure you fully understand — because you have done your part. At that point, it is my responsibility to do mine.

But I Just Have A Quick Question

Again, My website has all the information you may need. Additionally, you may utilize the Support Chat Box, conveniently located on the bottom right-hand side of the website, for faster responses or further assistance. I also have a Suggestion Box if you feel there is any information that should be added to my website.

The best way to reach me or get your questions answered is to book a consultation.

When you book, it guarantees that your concerns will be addressed during your scheduled time. If I have downtime before then, I may reach out sooner — but if not, you'll still have my full attention during your appointment.

Just because it's a quick question doesn't mean it's a quick answer.

For this reason, all questions, comments, and concerns must be addressed through a booked consultation to ensure no one goes unanswered.

I understand sometimes you may just have a quick question but realistically, I cannot repeatedly stop throughout the day to answer or return hundreds of unscheduled calls and text messages each day. Especially if they have already been addressed in the provided resources. Most of your questions will be answered in the FAQ, Rules & Expectations or Educational tab.

Doing so would disrupt workflow, delay progress, and ultimately take away from my ability to deliver the level of service and results that all clients deserve. It would also be unfair to those clients who are actively following the process and respecting the structure in place.

The screenshot above reflects my current calendar availability. As shown, my schedule is typically fully booked.

Booking Link

Contact Information

☎️ Support: 312-584-9969

📧 Email: [email protected]

Social Media

Yours Truly, TheCreditDaddy

Rules & Expectations

Important policies and agreements for all clients

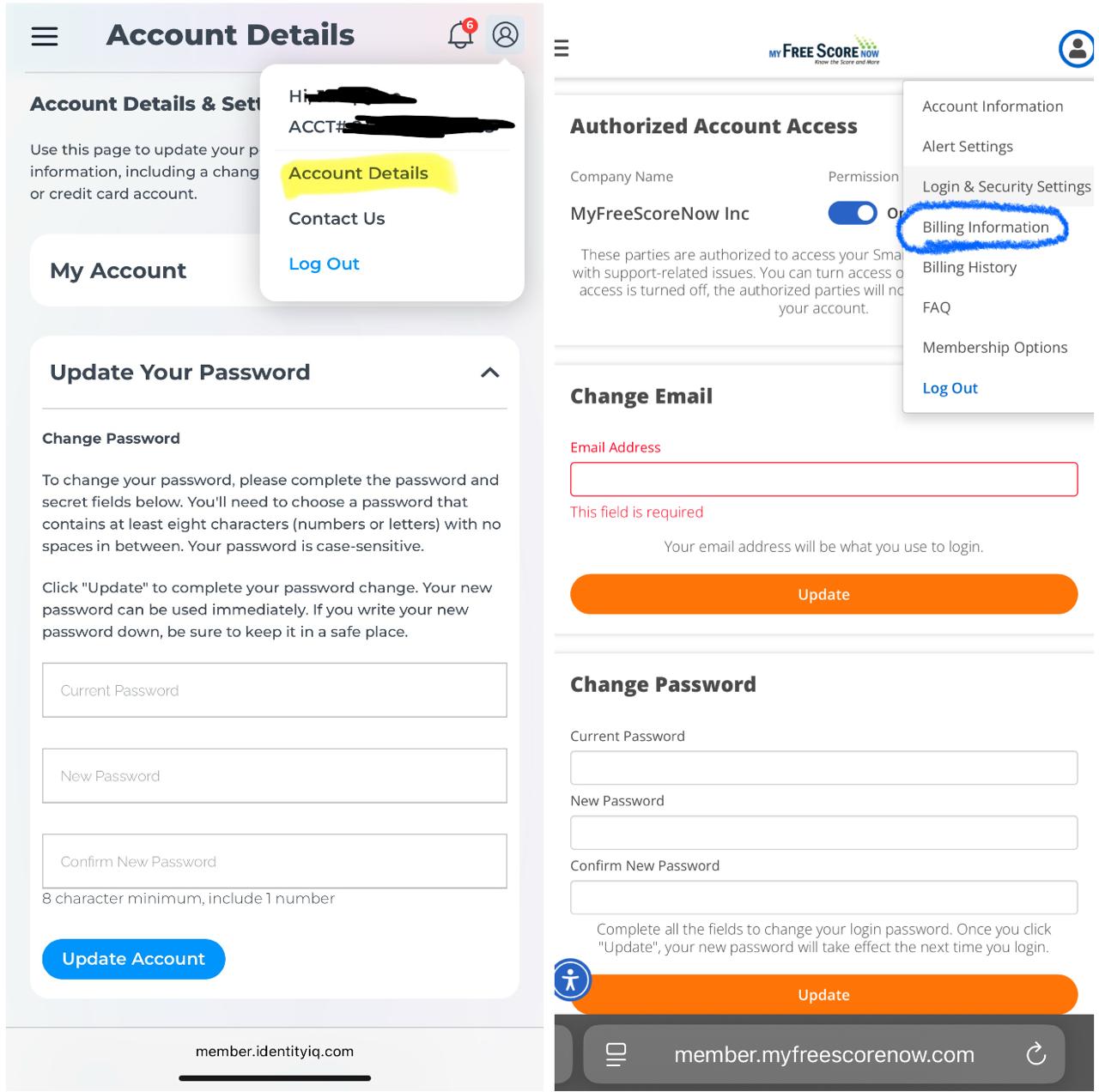

Different Websites And Logins

Just so there is no confusion about the websites and logins, understand that there are only 3 websites and logins.

1. Credit Monitoring Platform (Required)

When you first got started with our program you enrolled in one of the following credit monitoring services (which one you have depends on when you got started):

- IdentityIQ — https://member.identityiq.com/

- MyFreeScoreNow — https://member.myfreescorenow.com/login/

Important: You only need ONE of these platforms (not both).

This platform is used to:

- Monitor your credit

- View your full credit report

- Assist in generating dispute activity

Password Requirement: Please set your password to Credit@2025

2. Client Education & Resource Hub

The second platform is TheCreditDaddy.com. This website is used for:

- Frequently Asked Questions (FAQs)

- Education & Training

- Rules & Expectations

- Client To-Do List

- 24-Hour Support Chat

- Booking Consultations

- Refer A Friend

- Suggestion Box

- Available Resources

- Important Things That Can Hold You Back

All of this information can be found under the "Active Client" tab.

Access Password: Credit123!

3. Client Portal (Scorexer)

The final platform is your personal client portal (also available on an app called Credit Tracking):

https://ceoacademy.scorexer.com/Portal/login.jsp

This portal is used for two primary purposes:

1. Track Your Progress

- Monitor dispute activity

- View updates on your account

2. Upload Important Documents

Upload documents we request from you, or that you feel may help us with the process, such as:

- Proof of Address (POA)

- Driver's License / State ID / Passport

- Proof of payment for accounts in collections

- Identity theft documentation (e.g., police reports)

- Relevant screenshots, emails, mailed letters, or correspondence

Important Notice: You must sign the agreement after logging in before everything becomes available. Also, if we are unable to access your credit monitoring account, we will not be able to update your progress within your client portal.

Password Setup: You will receive a temporary password via email but may create your own password for this platform, as it serves as your personal and secure client portal.

Payment Agreement & Continuation of Services

When a payment agreement is established with a defined timeline, it is essential that the terms of that agreement are honored.

The fee charged covers the entire credit improvement process, not an individual dispute round. While payment plans are not required, one was extended as a courtesy.

If a scheduled payment is missed, all work on your account will be paused immediately, and no updates will be provided until the outstanding payment has been received.

If our team attempts to contact you regarding a missed payment and does not receive a response within 24 hours, the process will be fully suspended. In order to resume services, the remaining balance must be paid in full.

CLEAR UNDERSTANDING:

The amount you were charged represents the cost of the entire process. Any work completed up to that point is considered final and non-refundable.

This is similar to financing a vehicle. When you enter a financing agreement—for example, over a five-year term—you are expected to fulfill the agreed-upon payments for the duration of that contract.

Even if you make payments consistently for 3 years, failure to continue those payments can result in consequences such as the vehicle being disabled (in some newer models), repossession, and potential negative reporting to your credit.

The payments already made are not refunded, as they covered the time and usage of the vehicle during that period.

Now granted you're not buying a car, but I expect the same level of respect for my business. You wouldn't call the dealership and mention how you've already made payments for 3 years in a row. Because you understand you've broken the agreement so they no longer have to give you access.

Likewise, in this process, payments made reflect the services rendered up to that point. Therefore, they are not eligible for reimbursement, And I am not required to continue service at that point.

Once services have been stopped due to missing payments—the remaining balance must be PAID IN FULL, In order to resume services.

These policies are not personal. They are necessary to protect the integrity of our business operations and ensure fairness across all client accounts.

Payment Methods

When sending payment PLEASE DO NOT PUT FOR CREDIT REPAIR OR CREDIT CONSULTATION. Simply just put "THANK YOU FRIEND" for the memo.

CashApp, Apple Pay, Chime, PayPal, etc. are supposed to be for friends and family — not business. However, a lot of people don't have real bank accounts or just prefer to pay that way, so I'm just trying to work with what's easier for each client.

Inactive Client Policy & Reactivation Fee

At Wealthy Intention, we value every client and are committed to providing high-quality, consistent service. To maintain efficiency and ensure fairness to all active clients, we've implemented the following; Inactive Client Policy & Reactivation Fee

Reactivation Fee: $300

Inactive Client Policy

Clients with 60+ days of inactivity-meaning no responses/engagement, no document submissions, or no reactivation of credit monitoring-are placed on inactive status and removed from our active roster. To resume services, a $300 Reactivation Fee is required (covers admin time, file review, and system re-entry). Once you reach 60 days of inactivity you will be required to pay that $300 Reactivation fee.

Please note that multiple reminders via email and text are sent before an account becomes inactive. We understand that life happens-unexpected events, busy schedules, and personal matters can sometimes take priority. That's why we send multiple reminders before marking any account as inactive. Even if you communicate the reason you are unable to maintain your credit monitoring subscription, or upload certain documents, it does not eliminate the issues associated with becoming an inactive client.

At the end of the day Credit repair is a collaborative process. When clients go silent or no action is taken after repeated contact attempts, it not only delays their own progress but also affects our ability to manage our workload efficiently. It creates workflow and scheduling challenges for our team and backend systems. This policy ensures that active, engaged clients receive the attention and priority they deserve.

While an account is inactive, we are unable to continue work on the credit profile. However, we must still retain a client's file records of what was disputed or deleted in case a client later requests updates or verification of prior activity before becoming inactive. Which requires us to maintain your profile in our system and preserve all past correspondence, which results in monthly fees. Also storage costs for backed up emails and text for keeping old conversations for proof that reminders have been sent out. So in conclusion Even when no active work is being performed. We still have to pay for your files unless we delete all history.

For your convenience We also accept Afterpay, Klarna, and Zip as other forms of payment. Once paid, PLEASE REACH OUT FOR INSTRUCTIONS & we will promptly restore your account and continue your services.

Canceling Your Credit Repair Service

The average client goes through a minimum 4-7 rounds of credit repair before they have completed their program. Each round of results takes 45 days (1 and a half months) for a new update. These 4-7 rounds as a whole range between 6-9 months & sometimes up to 1 year for more severe cases.

By law we have to give the credit bureaus that time frame to view a client's file and validate the debt/inaccuracies! Please be patient with our team while we get each client results. If additional rounds are needed we will provide them at no extra charge.

Never judge a whole process based off 1 or 2 rounds. Just like a basketball game is 4 quarters — if something takes 3 or more rounds that's perfectly normal. It's apart of the process. You can expect certain rounds & sometimes back-to-back rounds with no change. Believe it or not it actually helps with getting deletions because it helps us catch the credit reporting agencies & debt collectors in violation even more than they already were.

💯 100% Money-Back Guarantee

If a client completes four (4) FULL ROUNDS of disputes as outlined in their service plan and receives zero (0) deletions, a 100% refund of the Service charge paid for credit repair only will be issued. (This does not include the $33/month for your credit monitoring.) This guarantee applies only when all program requirements and guidelines have been fully followed by the client.

We are committed to providing professional, compliant, and results-driven credit services. Because credit improvement is a process that requires time, consistency, and client cooperation, the following refund policy applies to all clients.

If you choose to stop services before completion, that is your right; however, no refund will be issued if you do not allow us to complete a minimum 4 rounds of the agreed-upon process due to you changing your mind. I shall only be responsible for a refund if I DID NOT DO MY JOB. Not because someone stopped me from doing my job which is get you DELETIONS.

How To Cancel:

Whenever you wish to stop the process just simply text 312-584-9969 with your first and last name and let us know that you no longer wish to move forward with the process and that you will take it from here. We will then stop the process for you immediately and whatever work that has been done up to that point will be considered final!

New Negative Items Policy 🚩

When you begin the credit repair process, my goal is to dispute and address all negative items currently listed on your credit report.

Important Notice

If new negative items appear during the process - such as new collections, inquiries, or late payments - please understand that I am not required to work on those new items. However, I do understand that there is a difference between an old account appearing later than expected vs applying for things & adding new inquiries or late payments.

Active Client Protection:

As part of my service process, if a new collection account appears or a previously deleted collection reappears while you are actively enrolled in the credit repair program, it will automatically be included in the next dispute round at NO ADDITIONAL COST. That said, this is a professional courtesy, not an obligation. I handle it this way in good faith to help keep all clients on track and maintain the progress of their credit profile.

After Program Completion:

Once all negative items have been removed and your file has been successfully completed and closed, the service is considered finished. If a collection account later appears or reappears after the completion of the program, there will be a $300 reactivation fee to reinitiate credit repair services.

To set clear expectations:

- Any new applications must be discussed with me in advance (book an appointment). This ensures we stay aligned, protect your credit, and avoid delays in your results. My goal is to deliver strong results, and that requires us to work together strategically.

- If we've already discussed the importance of keeping your accounts positive and you still receive new inquiries or negative items, an additional charge may apply for continued credit repair services.

- If I decide to charge for additional work, I will inform you first and ask whether you wish to move forward.

If you choose not to, that is your right. However I will only continue to work on the negative items that were originally on your report when you first enrolled as a client. Repeatedly applying for new credit while your disputes are in progress adds unnecessary inquiries, lowers your scores, works against and slows up your progress, and creates additional work that makes my job significantly harder. It also makes me look like I'm not doing my job. I simply can't have that.

Refund Policy

We are committed to providing professional, compliant, and results-driven credit services. Because credit improvement is a process that requires time, consistency, and client cooperation, the following refund policy applies to all clients.

100% Money-Back Guarantee

If a client completes four (4) full rounds of disputes as outlined in their service plan and receives zero (0) deletions, a 100% refund of fees paid will be issued. This guarantee applies only when all program requirements and guidelines have been fully followed by the client.

No Refunds Once the Process Begins

Once services have started, no refunds will be issued due to a change of mind. Please ensure you have discussed this decision with your spouse or decision-maker prior to payment completion.

If you choose to stop services before completion, that is your right; however, no refund will be issued if you do not allow us to complete the agreed-upon process. I shall only be responsible for a refund if I DID NOT DO MY JOB. Not because someone stopped me from doing my job which is get you DELETIONS.

Client Responsibility & Non-Refundable Conditions

Refunds will not be issued if the client interferes with the credit repair process or fails to follow required guidelines, including but not limited to:

- Clients who have been inactive for 60 days or more will be considered inactive and temporarily removed from our active client roster.

- Continuously adding new negative items to their credit profile

- Ignoring instructions or deadlines

- Failing to provide required documentation or access

- Taking actions that delay, disrupt, or prevent the completion of services

Any work completed up to that point will be considered final and non-refundable.

Fairness & Accountability: This policy exists to ensure fairness and accountability for both parties. Our goal is to help you rebuild and protect your credit, but success requires active participation, honesty, and cooperation from the client.

⚠️ Hard Truth:

You can't pay for credit repair then:

- Ignore or skim through instructions

- Stop responding

- Ignore emails and text messages

- Keep adding new inquiries, or late payments

- Skip credit building

Then come back 3 months later saying you haven't heard anything, seen any changes, requesting a refund, & proceed to blame my company or the process.

Credit repair works only when WE work.

I'm not a miracle worker, I'm a strategist. You have to do your part as well.

Please take your credit seriously-it represents your financial credibility.

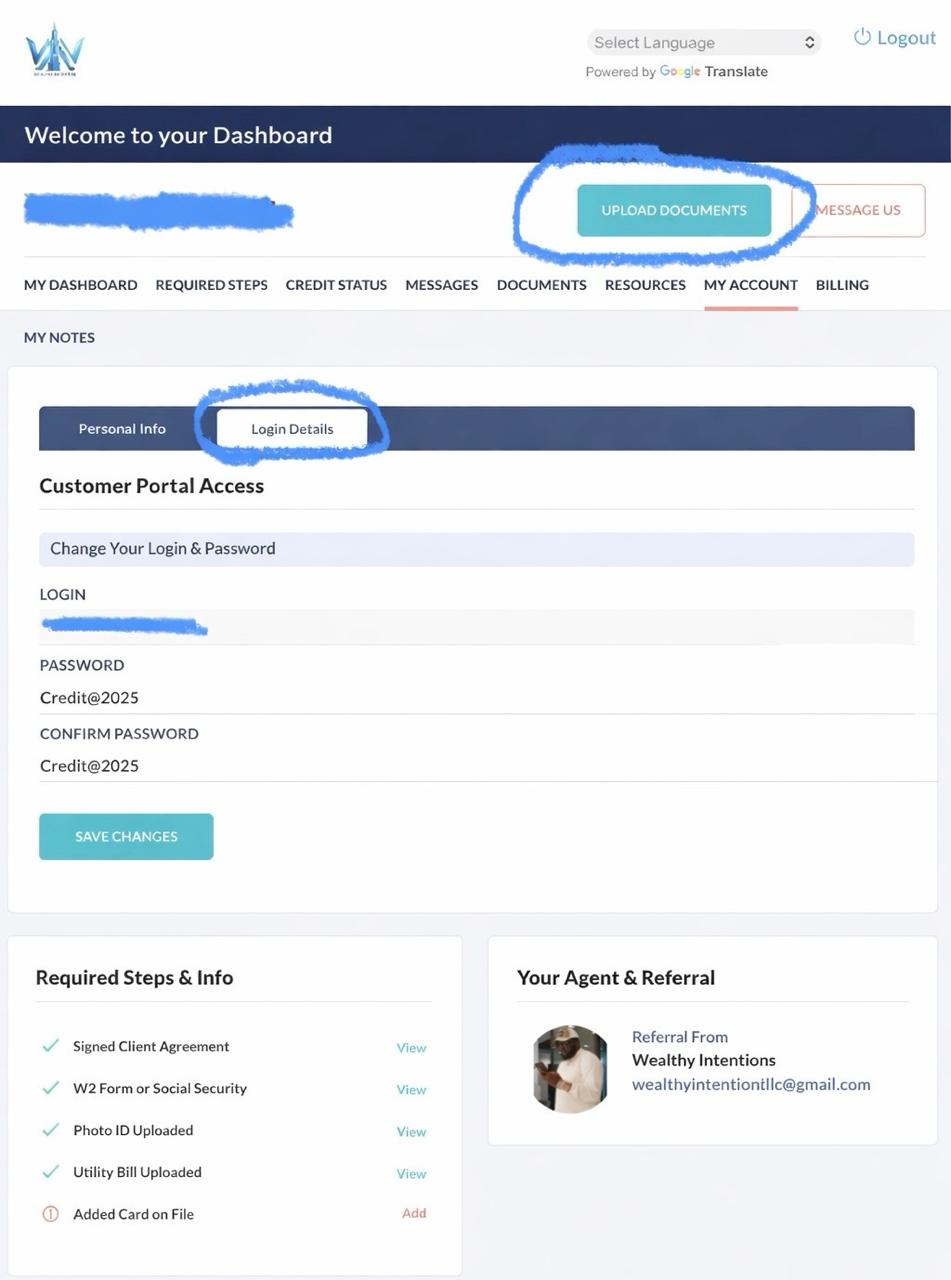

Setting Up Your Client Portal

⚠️ Important Notice: Anytime you upload any documents inside your portal you must notify us to check it at 312-584-9969 or [email protected]. We only check the client portal when notified!!

Within 4 Business Days After Getting Started my support team should have sent you a email for you to access your portal. The sole purpose of your client portal is to track your own progress and upload documents when necessary. Search for TRACK YOUR RESULTS or CLIENT PORTAL LOGIN in your email and spam. If you do not see the email with the username and password for your online client portal please text my team to make sure it gets resent out. (312) 584-9969

Important Notice: Anytime you upload any documents inside your portal you must notify us to check it at 312-584-9969 or [email protected]

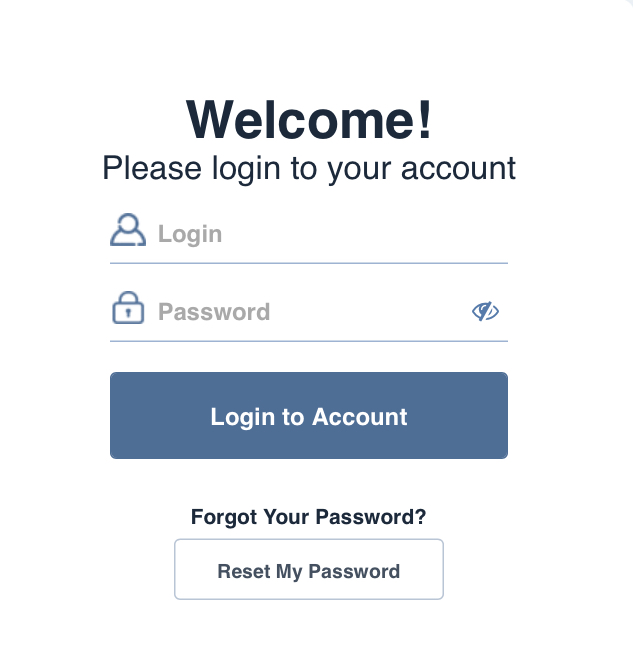

Log into your portal directly on the website: https://secure.scorexer.com/Portal/login.jsp

Things That Can Hold You Back

Common issues that delay results and how to avoid them

(THINGS YOU SHOULD BE DOING ON YOUR END)

Primary Issues That Can Hold You Back

- Expired Driver's License Or State ID

- Outdated credit monitoring reports

- Inaccessible or incorrect credit monitoring login credentials

- Missing or invalid Proof of Address (POA) documentation

- Full or inaccessible email inbox (clean up space or buy more storage if needed)

- Phone settings that block or silence unknown numbers. Please save 312-584-9969 in your contacts to ensure uninterrupted communication.

- NOT NOTIFYING US BY TEXTING THE SUPPORT NUMBER AFTER AN ISSUE HAS BEEN HANDLED.

IMPORTANT MENTAL NOTE:

Due to the high volume of clients we serve — over 500 individuals — it is not feasible for our team to repeatedly follow up with hundreds of clients each day regarding the same issue. It is also unfair to active clients and takes away from the attention they deserve. Our priority is to continue assisting clients who are actively completing the required steps in the program.

Please understand that once we have notified you of the issue, we have fulfilled our responsibility on our end. For this reason, WE WILL NOT revisit the client's file unless we are notified that the issue has been resolved. We will just assume the matter is still pending.

These are the primary issues that delay results for most clients. By proactively managing the items listed above, you set yourself up for a smooth and successful experience.

Whenever an issue arises — such as a POA matter or a login-issue concern etc. — our first step is to promptly notify the client so they are aware of the matter and can take the necessary steps to resolve it. By doing so you are tagged within our system. Once tagged, automated messages with CLEAR INSTRUCTIONS are sent to you via email & text every 10 days. You will no longer receive these notifications after a maximum of three reminders are issued, or until we are notified that the issue is resolved — whichever occurs first.

These reminders are simply a courtesy to ensure you don't forget & nothing is overlooked, as we understand that schedules can be busy. After providing this notification, our team proceeds with assisting other clients.

If you receive an email or text message regarding any of the items above, it is not sent without cause and is not a system error.

In most cases, either:

- Our team was not notified that the issue has been handled. (Most of the time this is the case)

- The issue has resurfaced and requires immediate attention.

- The login information provided were invalid.

- The submitted documentation is invalid.

That Said — These notifications should NEVER be ignored.

Before responding with "I've already completed this," please take a moment to verify first, and provide a screenshot as proof if you believe the issue has already been resolved.

- Log directly into your credit monitoring account to confirm the report is current

- Confirm all documents are clear, dates are accurate & all submitted documents are up to date

Verification ensures accuracy, prevents delays, and keeps your account active and progressing as intended. Notify 312-584-9969 whenever you have taken care of an issue.

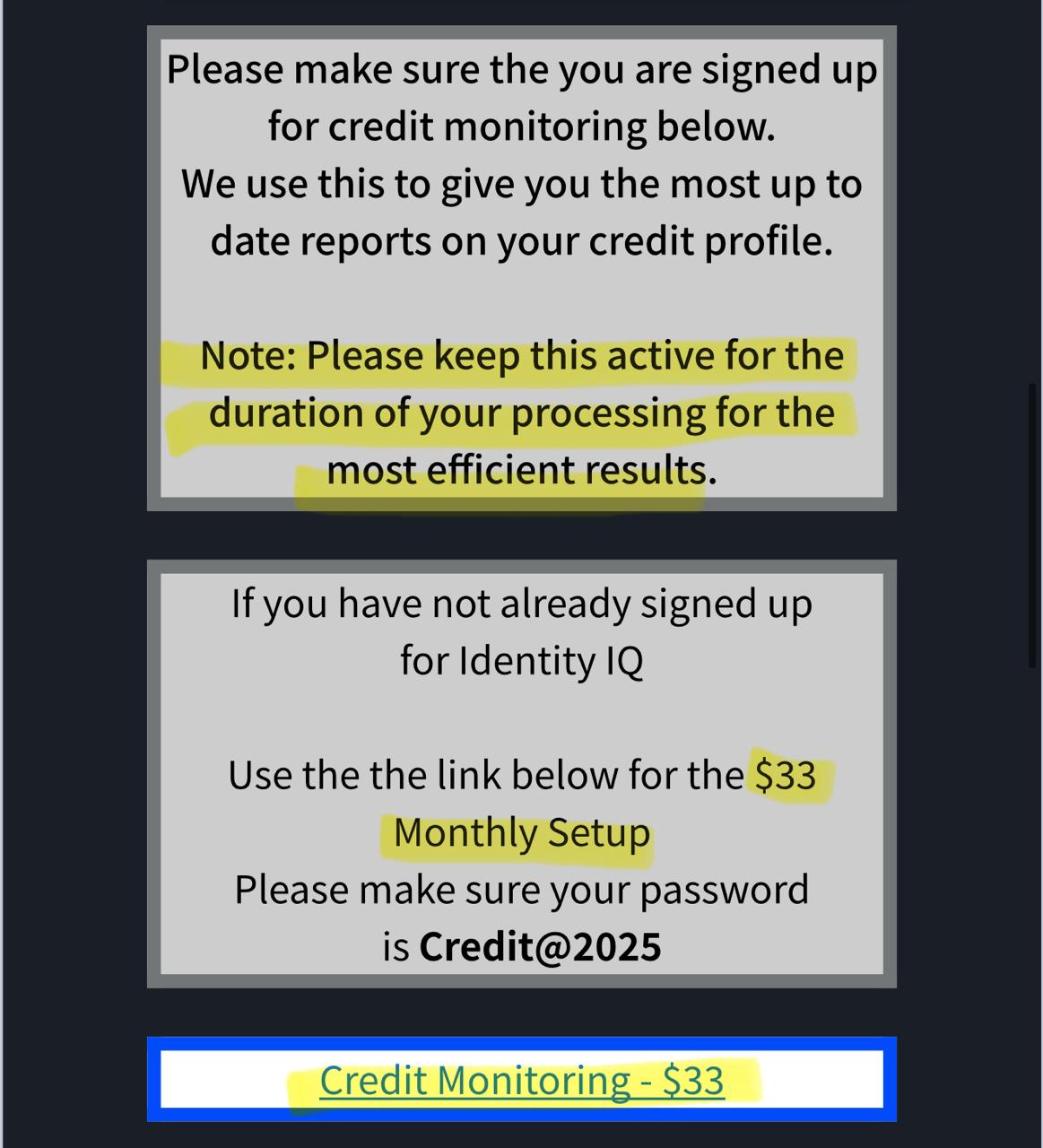

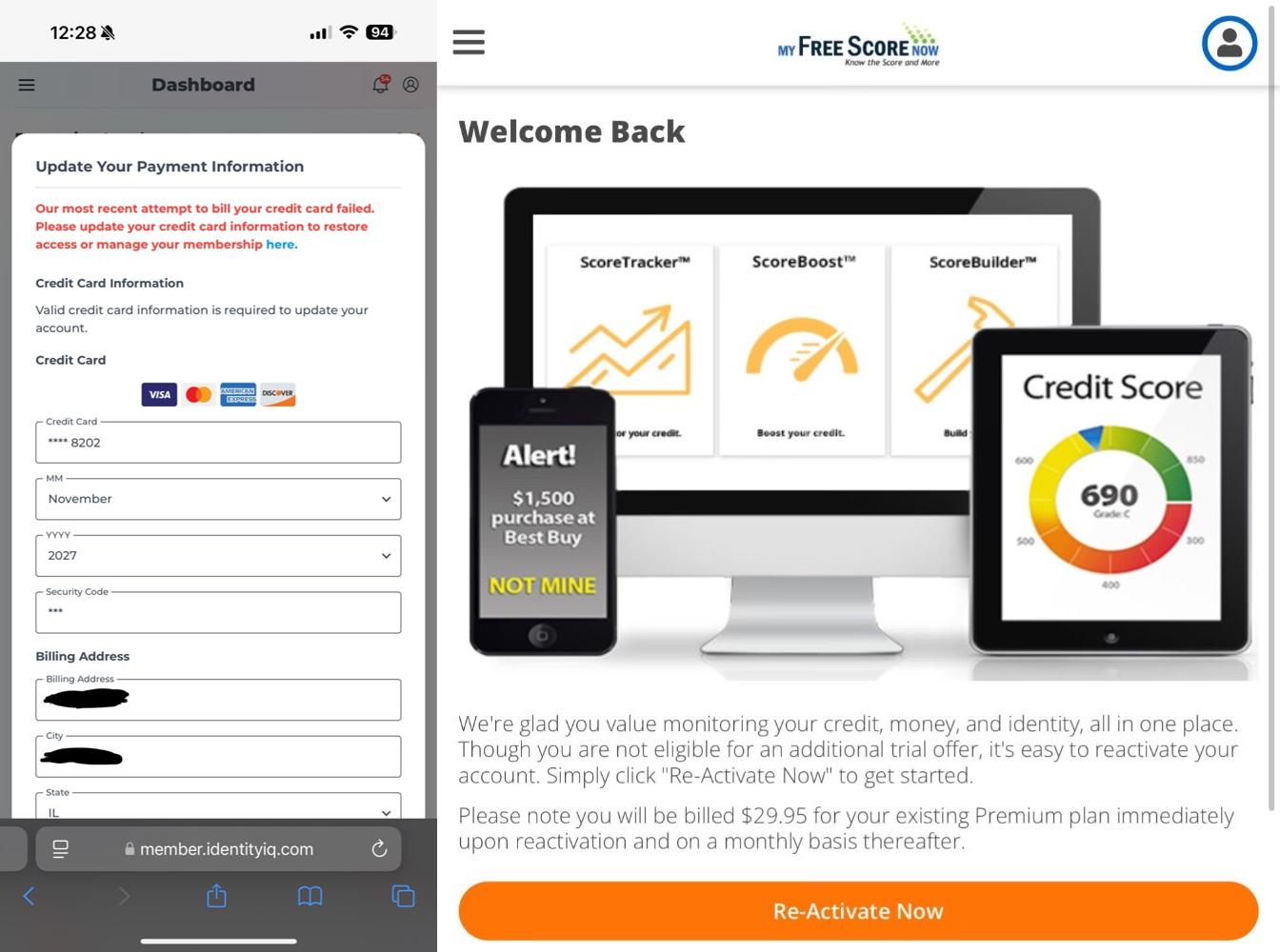

Credit Monitoring Payment Issue

Just to have a clear understanding, yes the fee you paid me directly covers the work I perform on your credit profile. However, in order to proceed effectively, we must have access to all three credit reports and scores. This requires a separate credit monitoring service, which comes with a monthly fee — and that fee was disclosed to you during the sign-up process before you got started.

Unless you text 312-584-9969 with your first and last name, giving us consent to update your report when needed, we cannot update it for anyone because we’re not responsible for any unauthorized charges.

Please understand that your Card Number and CVV will be required for us to complete this for you. If you do not wish to give us consent to update it for you, that is fine. It will be your responsibility to keep track, as you will only be reminded 3 times about this.

So, set monthly reminders in your calendar now.

This platform is used to:

- Monitor your credit

- View your full credit report

- Assist in generating dispute activity

- Compare and contrast previous reports

- Contact creditors on your behalf

- Identify inaccuracies on your credit report

That said, please understand that there is absolutely NO WAY for me, you, or anyone else to work on your credit without having access to your credit reports.

Which means if we are trying to send you an update on your current status or perform the next round of disputes on your behalf, this issue would prevent us from doing both.

Please understand that if you fall behind on this, that DOES NOT MEAN you don't have any results. I just can't tell you what's going on with your status or continue services if I cannot access your credit report.

So if we try to log into your credit report and can't access it due to missing payments, it will prolong the process for you. And that would be 100% your fault.

Here's What To Do To Prevent This:

Step 1. Every 40 days I want you to go to the website for your credit monitoring account — NOT THE APP.

Log into your report and the same message should appear. If it does, please pay your subscription at your earliest convenience.

Step 2. Notify us with your first & last name at 312-584-9969 that your account is back active. If it has been more than 45 days since your last PDF update, you shall receive one within 4 business days from notifying us.

If you receive an email or text message regarding any of the information above, it is not sent without cause and is not a system error.

In most cases, either:

- Our team was not updated that the issue has been handled

- The issue has resurfaced and requires immediate attention

These notifications should never be ignored.

Before responding with "I have already completed this," please take a moment to verify first — log directly into your credit monitoring account to confirm the report is active. If you feel it was a mistake, please provide a screenshot of proof that the situation has been handled.

Inactivity Policy

If your dispute process is paused for inactivity after 60 days, you will be placed on our Inactive Client Roster and YOU WILL HAVE TO PAY A $300 Re-Activation Fee TO GET BACK STARTED.

Please note that multiple reminders are sent via email and text before a profile becomes inactive. When no action is taken after repeated contact attempts, it creates workflow and scheduling challenges for our team and backend systems.

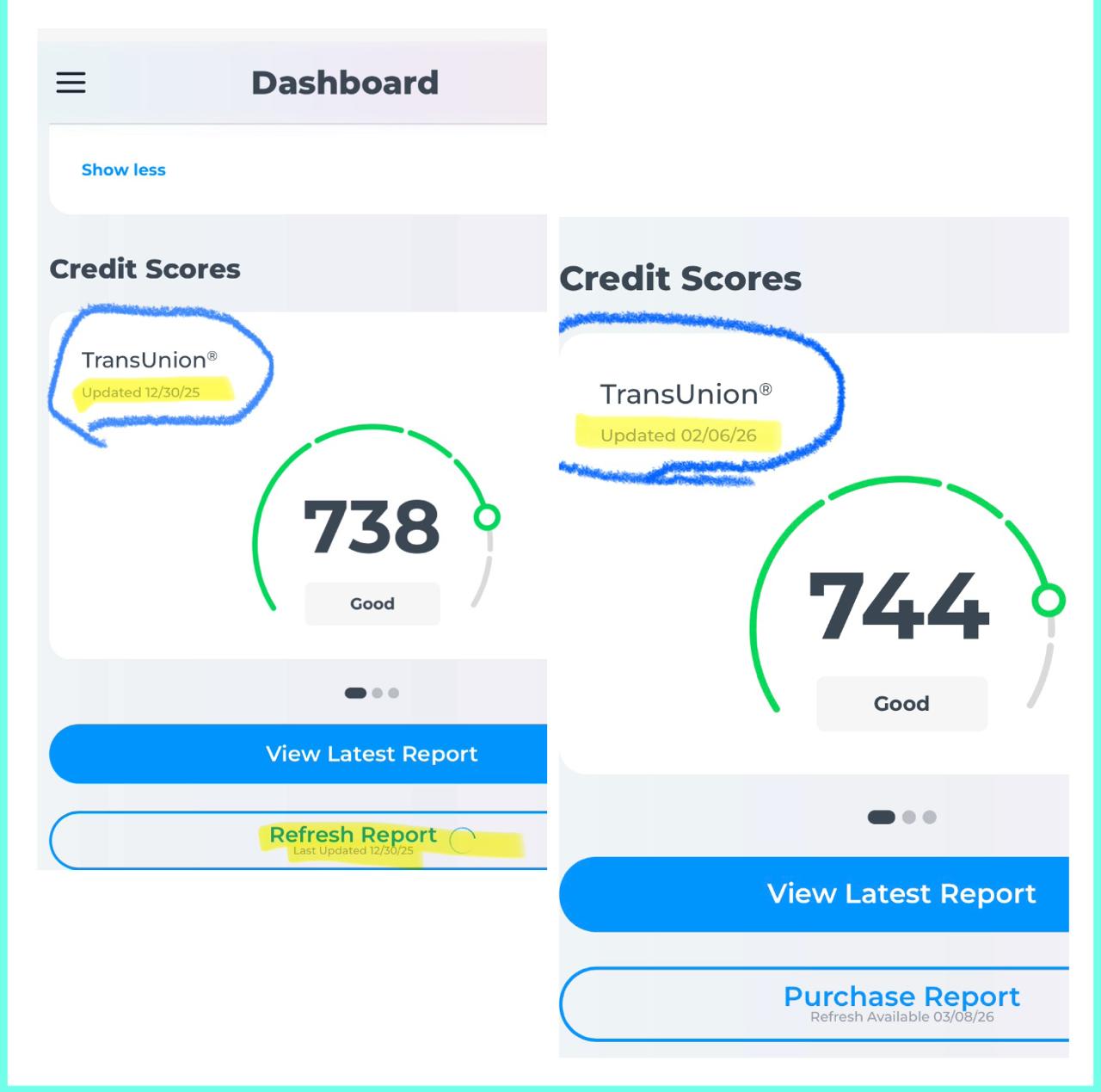

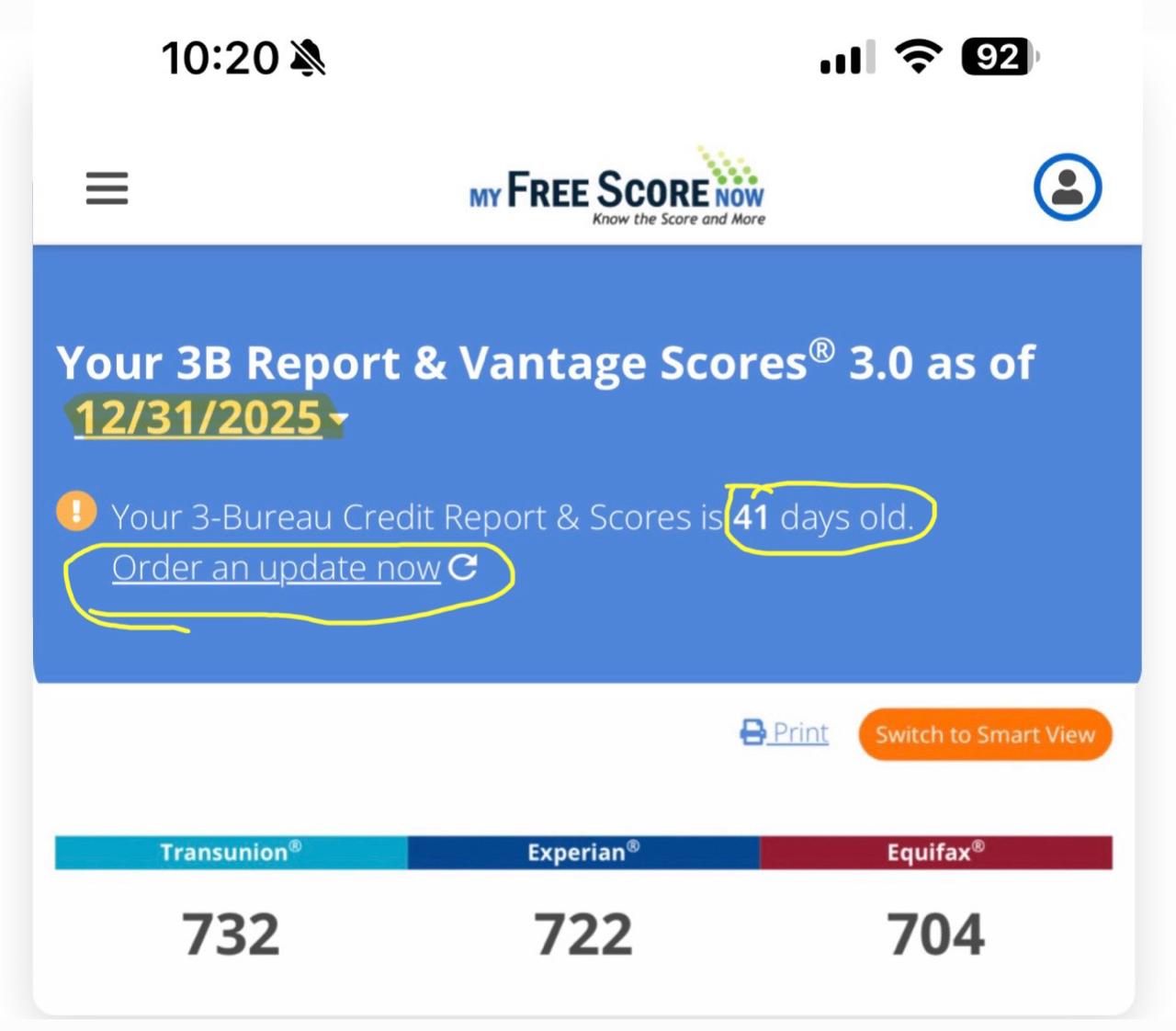

Credit Monitoring Outdated

It Is Extremely Important That You Understand The Difference Between UPDATED and ACTIVE:

● ACTIVE means you have successfully paid the $33 fee for your credit monitoring ( just because your card was charged doesn't mean your report will automatically update )

● UPDATED means you actually ordered a new report. ( Every month you get a new one but they do not update automatically, sometimes you have to manually refresh the report )

BOTH OF THESE MUST BE DONE IN ORDER FOR US TO GIVE YOU AN UPDATE. Regardless of if you have IDIQ OR MFSN, Your Credit Report Should NEVER Be More Than 40 Days Old. If it is then that means you haven't logged into your credit report to update it.

Unless you text 312-584-9969 with your first and last name, giving us consent to update your report when needed. We cannot update it for anyone because we are not responsible for any unauthorized charges. If you do not wish to give us consent to update it for you that is fine. It will be your responsibility to keep track as you Will Only Be Reminded 3 Times About This... So I Am Telling You Now To Set Monthly Reminders In Your Calendar.

Understand if you fall behind on this I won't be able to send you your round results. But that DOES NOT MEAN That you don't have any results. I just can't tell you what's going on in June if I'm looking at a report from March.

Step 1. IDIQ USERS ONLY - Every 40 Days I want you to go to the website NOT THE APP. https://member.identityiq.com/

- ● If your report isn't already showing the current month, click on REFRESH REPORT.

Step 1. MFSN USERS ONLY - Every 40 Days I want you to go to the website NOT THE APP: https://member.myfreescorenow.com/login/ — Member Login | MyFreeScoreNow

- ● If your report isn't already showing the current month, click on ORDER NEW UPDATE

Step 2: Notify Us At With Your First & Last Name 312-584-9969 That Your Report Has Been Updated. If It Has Been More Than 45 Days Since Your Last PDF Update You shall receive one Within 4 Business Days From Notifying Us.

If you receive an email or text message regarding any of the information above, it is not sent without cause and is not a system error. In most cases, either: Our team was not updated that the issue has been handled, or The issue has resurfaced and requires immediate attention. These notifications should never be ignored.

Before responding with I have already completed this, please take a moment to verify first: Log directly into your credit monitoring account to confirm the report is active. Make sure your reports are actually updated. Make sure your logins are Correct. Verification ensures accuracy, prevents delays, and keeps your account active and progressing as intended.

Inactivity Policy

If Your Dispute Process Is Paused For Inactivity After 60 Days You Will Be Placed On Our Inactive Client Roster And YOU WILL HAVE TO PAY A $300 Re-Activation Fee TO GET BACK STARTED.

Please note that multiple reminders are sent via email and text before a profile becomes inactive. When no action is taken after repeated contact attempts, it creates workflow and scheduling challenges for our team and backend systems.

POA (Proof Of Address)

Proof of Address Requirements:

There Are only 3 acceptable documentations for this: Utility Bill, Bank Statement, Or Lease Agreement. NOTHING ELSE. & We Only Need 1 Out Of The 3. If you are paperless, share the link of the PDF to our support email instead of sending a screenshot.

All Bank Statements Are Accepted (Chime, Cashapp, Varo, Bank Of America, Or Whatever Institution You Bank With. Credit Card Bank Statements Are Also Acceptable)

To be valid, the document must:

• Display your FULL FIRST AND LAST NAME (not a business name or nicknames)

• Show your COMPLETE CURRENT RESIDENTIAL ADDRESS

• Pictures MUST BE FULL PAGE Meaning TAKE IT OUT OF THE MAIL AND UNFOLD IT

• Screenshots Must Also Be FULL PAGE meaning MAKE SURE ALL 4 CORNERS ARE IN THE PIC

• Must Not Be Too Light Or Too Dark

• Must NOT be blurry

• No shadows blocking words on the documents

• Must Be Dated within the LAST 60 DAYS

If the document is older than 60 days, it is considered outdated and cannot be used. For example, if it is currently December and the document on file is from September or October, it is no longer valid. For this reason, we strongly recommend SUBMITTING A NEW POA EVERY MONTH as soon as it becomes available. Utility bills and bank statements are often delayed, and by the time the next update cycle arrives, a previously submitted document may already be expired. This can cause unnecessary delays for both you and our team.

If you have a RENTAL OR LEASE AGREEMENT, that is ideal, as it typically remains valid for an extended period and eliminates the need for monthly submissions.

Important: Please note that the address on your utility bill or bank statement DOES NOT NEED TO MATCH the address listed on your State ID Or Drivers License — that is not what we are verifying. What matters is that the address on your Utility Bill Or Bank Statement accurately matches your CURRENT PLACE OF RESIDENCE, as this serves as your OFFICIAL PROOF OF ADDRESS (THIS IS WHAT WE ARE VERIFYING EVERY MONTH).

If the address on your utility bill or bank statement DOES NOT MATCH the CURRENT address where you are actively living, you have Three (3) options:

SUGGESTION #1 (Highly Recommended):

• Update the address directly online using your mobile app before downloading the new PDF document. Resend it to [email protected]

• If the New PDF doesnt display your edits immediately you may have no choice but to wait until they new one is ready. Which should be at the beginning of the new month. (I believe chime bank statements update immediately after editing)

SUGGESTION 2 (Faster results):

• Download a pdf editor app and change the address to your new address

SUGGESTION #3 (Completely Optional):

• If you cannot edit your Utility Bill or Bank Statement yourself you can Submit a editing fee, which covers the cost for my partner to update the document on your behalf.

Understand This POA Is Mandatory. If You Cannot Provide This Monthly, We Wont Be Able To Dispute On Your Behalf.

Inactivity Policy:

If Your Dispute Process Is Paused For Inactivity After 60 Days You Will Be Placed On Our Inactive Client Roster And YOU WILL HAVE TO PAY A $300 Re-Activation Fee TO GET BACK STARTED. Please note that multiple reminders are sent via email and text before a profile becomes inactive. When no action is taken after repeated contact attempts, it creates workflow and scheduling challenges for our team and backend systems.

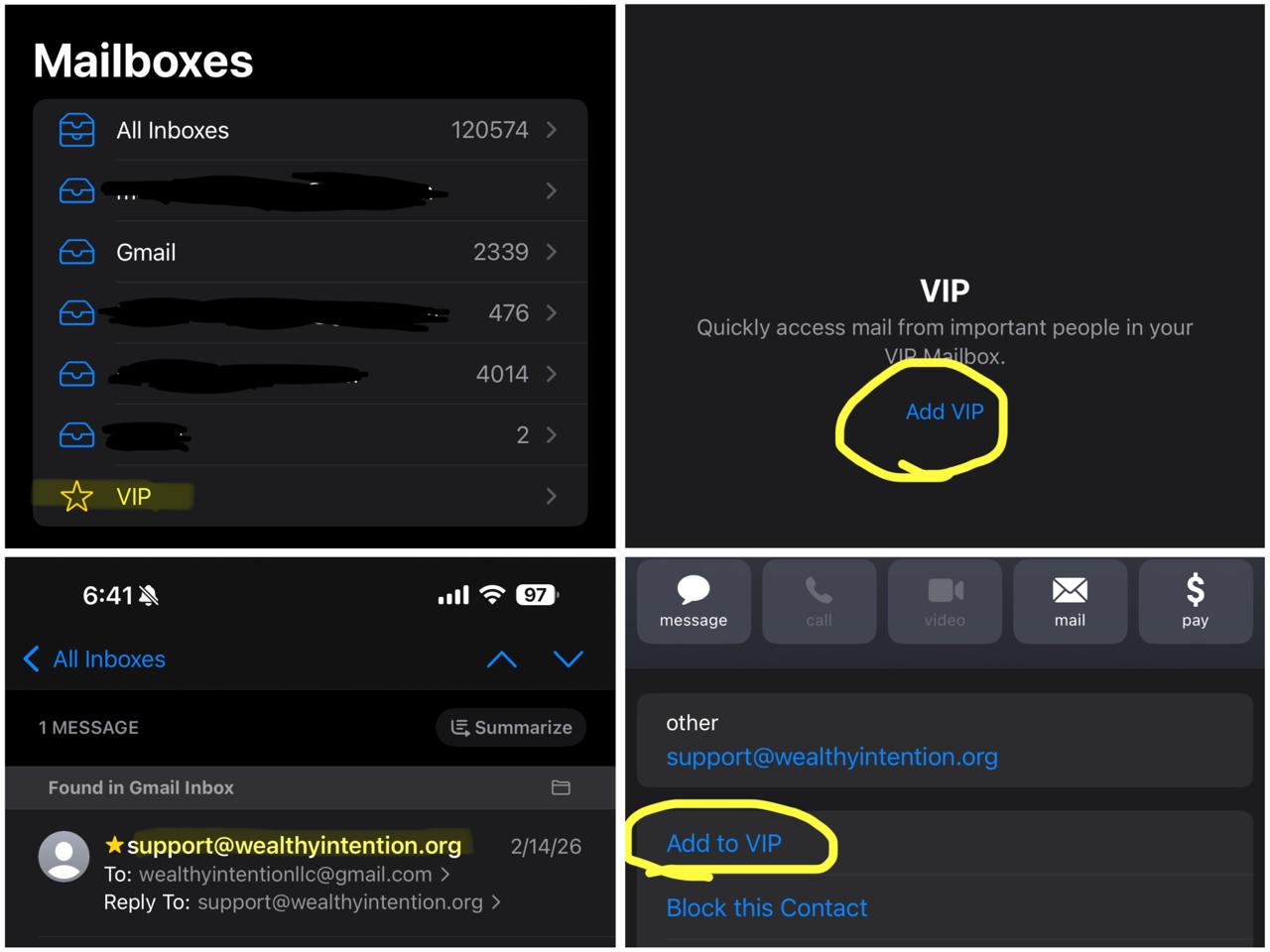

Trouble Finding Emails?

It is impossible to call/text 400+ people everyday so most of our communication will be through via email. To ensure you receive all important updates regarding your account, please add our emails [email protected] & [email protected] to your contacts and mark it as a priority or VIP sender in your email settings.

📱 How To Add As VIP (iPhone/Apple Mail):

- Open your Mail app → go to your Mailboxes screen

- Tap VIP in the list

- Tap Add VIP

- Search for and select [email protected]

- Repeat for [email protected]

This will help prevent our messages from being sent to your spam or promotions folder and ensure you receive all updates, dispute results, and important notifications in a timely manner.

Just to be on the safe side — be sure to check your emails & spam weekly if not daily.

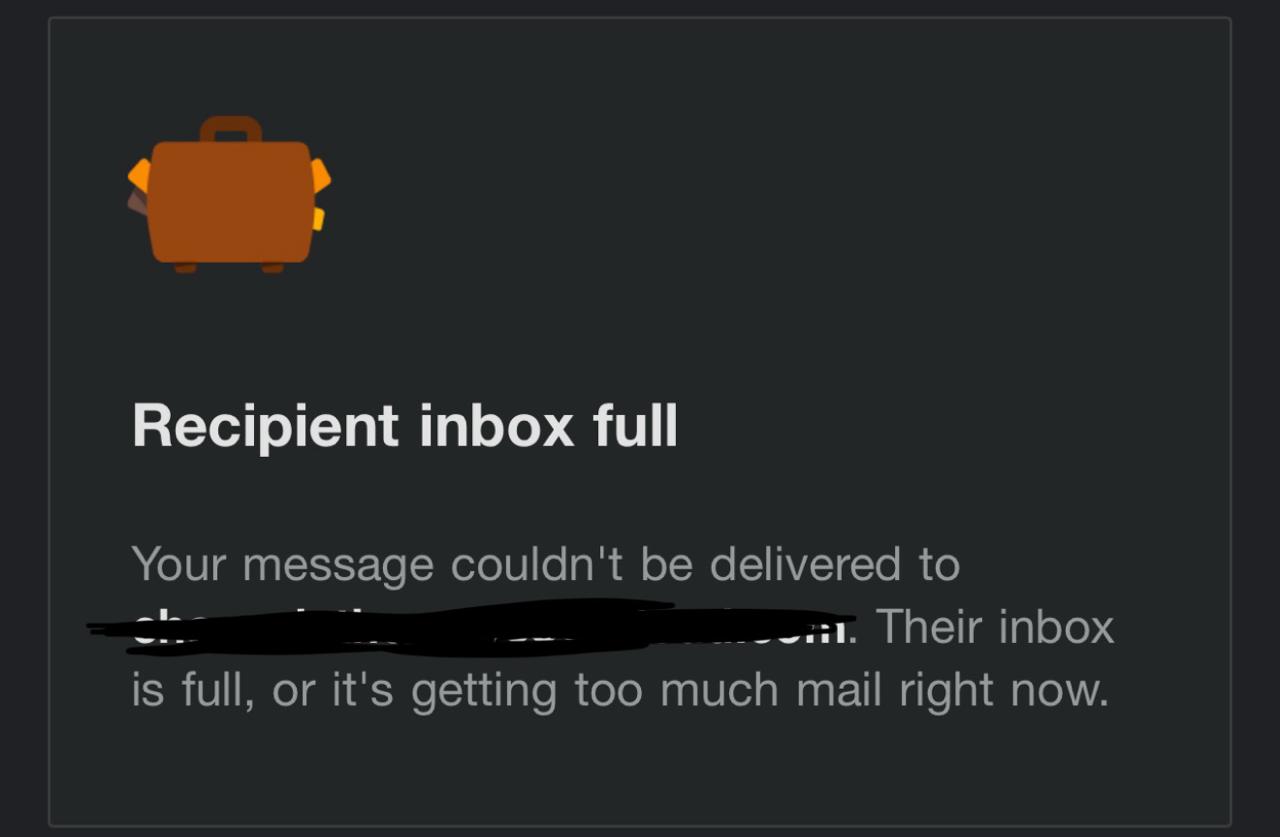

It is just as important to make sure that your email storage isn't full. This will prevent us from being able to email you and it will also prevent you from being able to email us. I don't want a situation where both parties are doing their part but the emails aren't going through.

⚠️ Recipient Inbox Full Error:

If you or we receive a "Recipient inbox full — your message couldn't be delivered" error, it means your email storage is maxed out. Please immediately clean up your inbox or purchase more storage to ensure communication isn't disrupted.

If you ever get a new email or prefer us to send notifications to a different email please notify us at 312-584-9969 with your First & Last Name and new email. This also applies for new phone numbers.

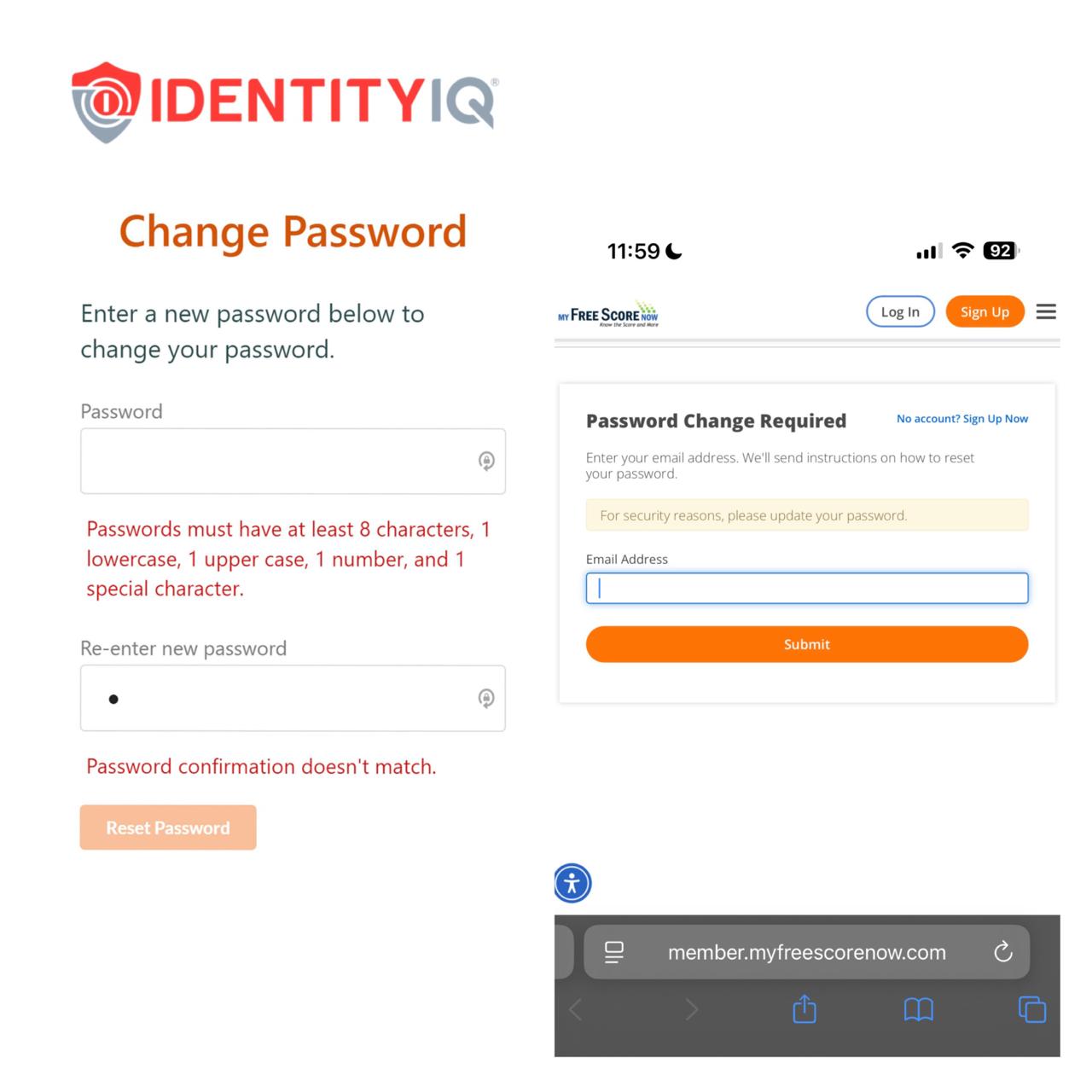

Login Credentials

MAKE SURE YOUR PASSWORD IS Credit@2025 with a Capital "C"

- ● If you can't use Credit@2025, add a period at the end so Credit@2025.

- ● If That Doesn't Work Please Use Credit@2025!

Please Do Not Make Your Own Password. It Makes Our Jobs A lot easier when we can have all clients have the same password. If none of these passwords work out please text our support number to see what password we recommend.

Having Trouble Changing Your Password?

IdentityIQ Customer Service: (877) 875-4347

MyFreeScoreNow Customer Service: (888) 548-2008

Please be sure to text 312-584-9969 with your first and last name after you change it

Password Change Required

This happens every so often for security purposes. These notifications should never be ignored. If you receive an email or text message regarding any of the items above, it is not sent without cause and is not a system error.

In most cases, either:

- ● Our team was not notified by you that the issue has been handled, or

- ● The issue has resurfaced and requires immediate attention.

Before responding with "I've already completed this," please take a moment to verify first:

Log directly into your credit monitoring account to confirm the report is current

What To Do:

Please Do Not Make Your Own Password. It Makes Our Jobs A lot easier when we can have all clients have the same password. If none of these passwords work out please text our support number to see what password we recommend.

Step 1: Actually log into your account to confirm if the same issue pops up for you. If not, send a screenshot to our support team of you being logged into the credit report to 312-584-9969.

Step 2: If the issue also shows for you, just enter your email to receive the reset password link. Once received, enter the same exact password Credit@2025 with a Capital "C". If you can't use the same password add a period at the end so Credit@2025. If That Doesn't Work Please Use Credit@2025!

Step 3: After Updating The Password Be sure to log into your account to make sure the password works.

Step 4: Once completed Please text (312) 584-9969 or with your first and last name to notify us that your account is back active with the new password, as we will no longer check on this for you until notified.

Having Trouble Changing Your Password?

IdentityIQ Customer Service: (877) 875-4347

MyFreeScoreNow Customer Service: (888) 548-2008

Please Be sure to text 312-584-9969 with your first and last name after you have changed it.

Phone Settings - DND

Please add our support number — 312-584-9969 — to your phone contact favorites for both calls and text messages. This helps ensure that our communications reach you successfully and are not mistakenly blocked or filtered by your phone. It is common for mobile devices to have settings enabled that silence or block unknown numbers. Please note that 312-584-9969 is the official number used by our customer service team. We kindly ask that you save this number to ensure you receive all necessary communications.

Do NOT Reply "STOP"

Please do not reply with "STOP." Doing so will automatically block all future text messages and emails from our system, which may prevent you from receiving important updates. This could delay your progress and result in your account becoming inactive.

If you have already replied "STOP" to this number, please text a message back to 312-584-9969 to start back receiving updates & notifications via email & text.

If you ever get a new number or prefer us to send messages to a different number, please notify us at [email protected] with your First & Last Name and new number so we can update your contact information in our system to avoid any interruptions in service. This also applies for a new email.

Canceling Your Credit Monitoring Service

If you choose not to continue your monthly credit monitoring subscription, that is entirely your right. However, please understand that active credit monitoring is required for us to access your credit reports and continue working on your profile.

Once monitoring is canceled, your file is automatically paused. Due to the cancellation we will no longer be able to provide round results or perform any additional work on your account. This does not mean that no results exist — it simply means we no longer have access to your credit reports to review or communicate updates.

After 60 days of inactivity, you will be removed from our active client roster & the credit repair process is terminated. Any work completed up to that point will be considered final. No refunds will be issued, as services were rendered and further progress was prevented by the client. This policy is clearly disclosed in our refund policy, and every client was acknowledged about the $33 monthly fee when they completed the onboarding form.

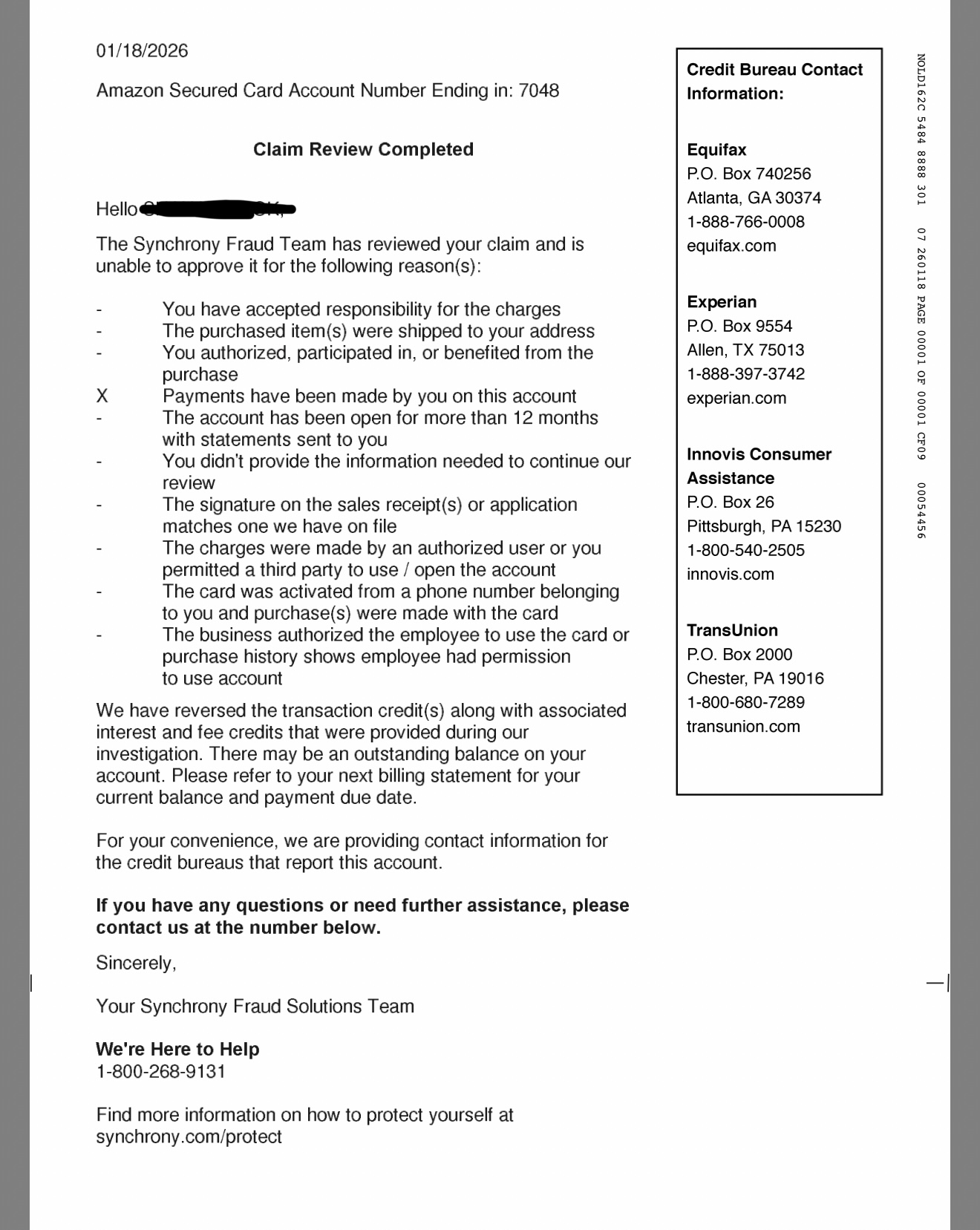

Important — Do NOT Dispute the Charge

Please do not dispute the charge with your bank, request a chargeback against the credit monitoring company, or have your bank block the credit monitoring company from being able to charge your card.

When this happens it creates financial penalties for the provider. That company already deposited that money into THEIR BANK ACCOUNT. When u DISPUTE it, now that money is being taken away from that company for fees you LEGALLY AGREED TO. BY LAW now that company can come after you. Chargebacks may also expose you to potential collection activity.

If you wish to cancel properly, please follow these steps instead:

- Log into your mobile app or contact the credit monitoring company's customer service directly to cancel your subscription.

- Text 312-584-9969 and let us know you no longer want to move forward.

Thank you for your cooperation and understanding.

Canceling Your Credit Repair Service

The average client goes through a minimum 4-7 rounds of credit repair before they have completed their program. Each round of results takes 45 days (1 and a half months) for a new update. These 4-7 rounds as a whole range between 6-9 months & sometimes up to 1 year for more severe cases.

By law we have to give the credit bureaus that time frame to view a client's file and validate the debt/inaccuracies! Please be patient with our team while we get each client results. If additional rounds are needed we will provide them at no extra charge.

Never judge a whole process based off 1 or 2 rounds. Just like a basketball game is 4 quarters — if something takes 3 or more rounds that's perfectly normal. It's apart of the process. You can expect certain rounds & sometimes back-to-back rounds with no change. Believe it or not it actually helps with getting deletions because it helps us catch the credit reporting agencies & debt collectors in violation even more than they already were.

💯 100% Money-Back Guarantee

If a client completes four (4) FULL ROUNDS of disputes as outlined in their service plan and receives zero (0) deletions, a 100% refund of the Service charge paid for credit repair only will be issued. (This does not include the $33/month for your credit monitoring.) This guarantee applies only when all program requirements and guidelines have been fully followed by the client.

We are committed to providing professional, compliant, and results-driven credit services. Because credit improvement is a process that requires time, consistency, and client cooperation, the following refund policy applies to all clients.

If you choose to stop services before completion, that is your right; however, no refund will be issued if you do not allow us to complete a minimum 4 rounds of the agreed-upon process due to you changing your mind. I shall only be responsible for a refund if I DID NOT DO MY JOB. Not because someone stopped me from doing my job which is get you DELETIONS.

How To Cancel:

Whenever you wish to stop the process just simply text 312-584-9969 with your first and last name and let us know that you no longer wish to move forward with the process and that you will take it from here. We will then stop the process for you immediately and whatever work that has been done up to that point will be considered final!

Credit Monitoring Reactivation Notice

From time to time, your credit monitoring account may require reactivation for security purposes. Please understand that this does not necessarily indicate a missed or incomplete monthly payment. In most cases, it simply means that you need to verify the payment method on file, which may include re-entering your card's CVV code.

When this occurs, it temporarily delays our ability to access your credit report, which can impact the progress of your file.

Your Privacy Is Protected

Please note that for security and privacy reasons, we do not have access to your card information and will never request it from you. Therefore, we are unable to complete this verification on your behalf.

How To Resolve It

- Log into your credit monitoring account

- Confirm your payment method on file

- Complete any required verification steps (e.g. re-enter your CVV code)

- Notify us once it has been resolved so we can resume work on your profile

Please be advised that we will not continue to follow up on this issue without confirmation from you that it has been resolved.

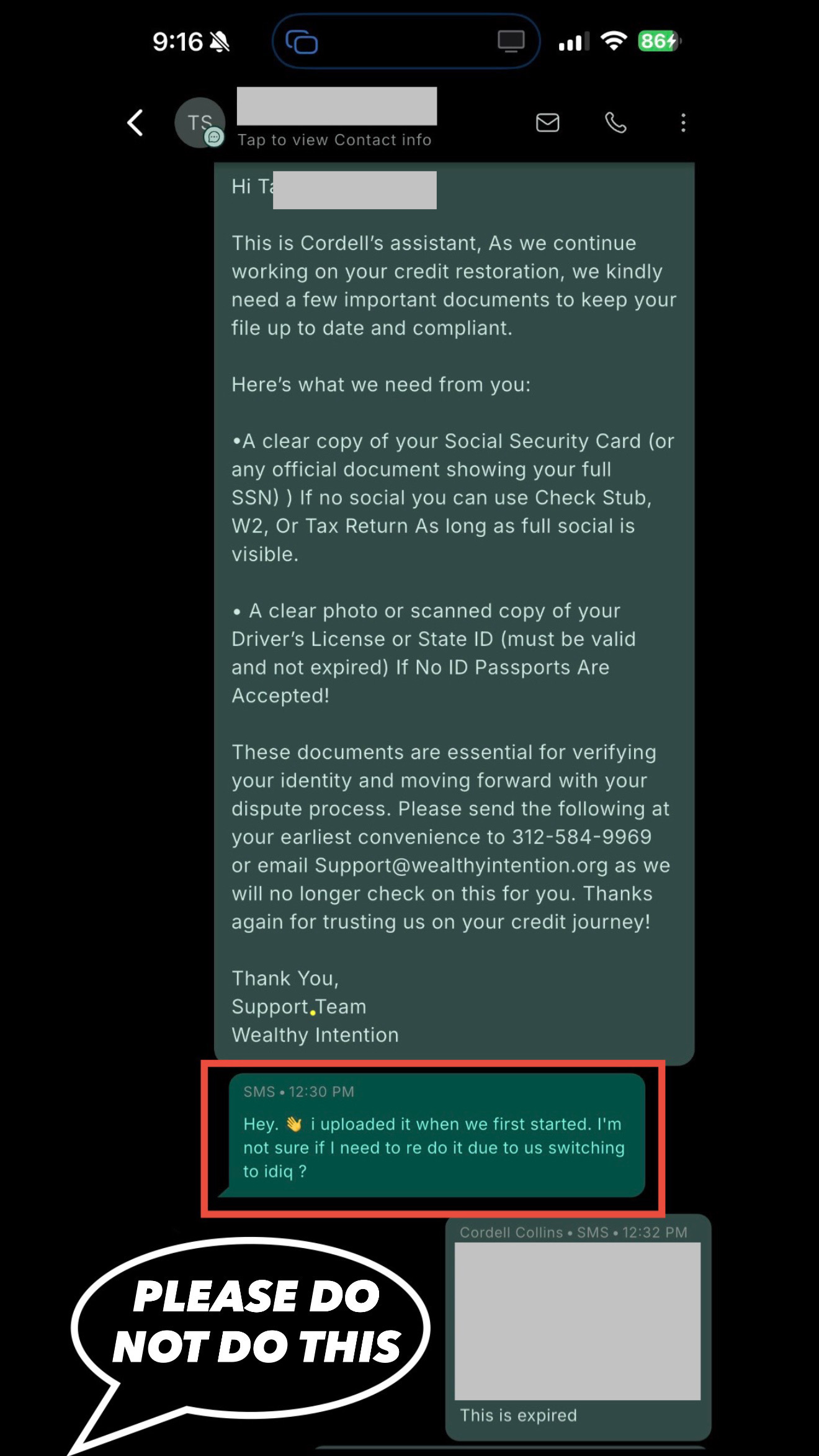

Expired Driver's License Or State ID

This Is Pretty Self Explanatory

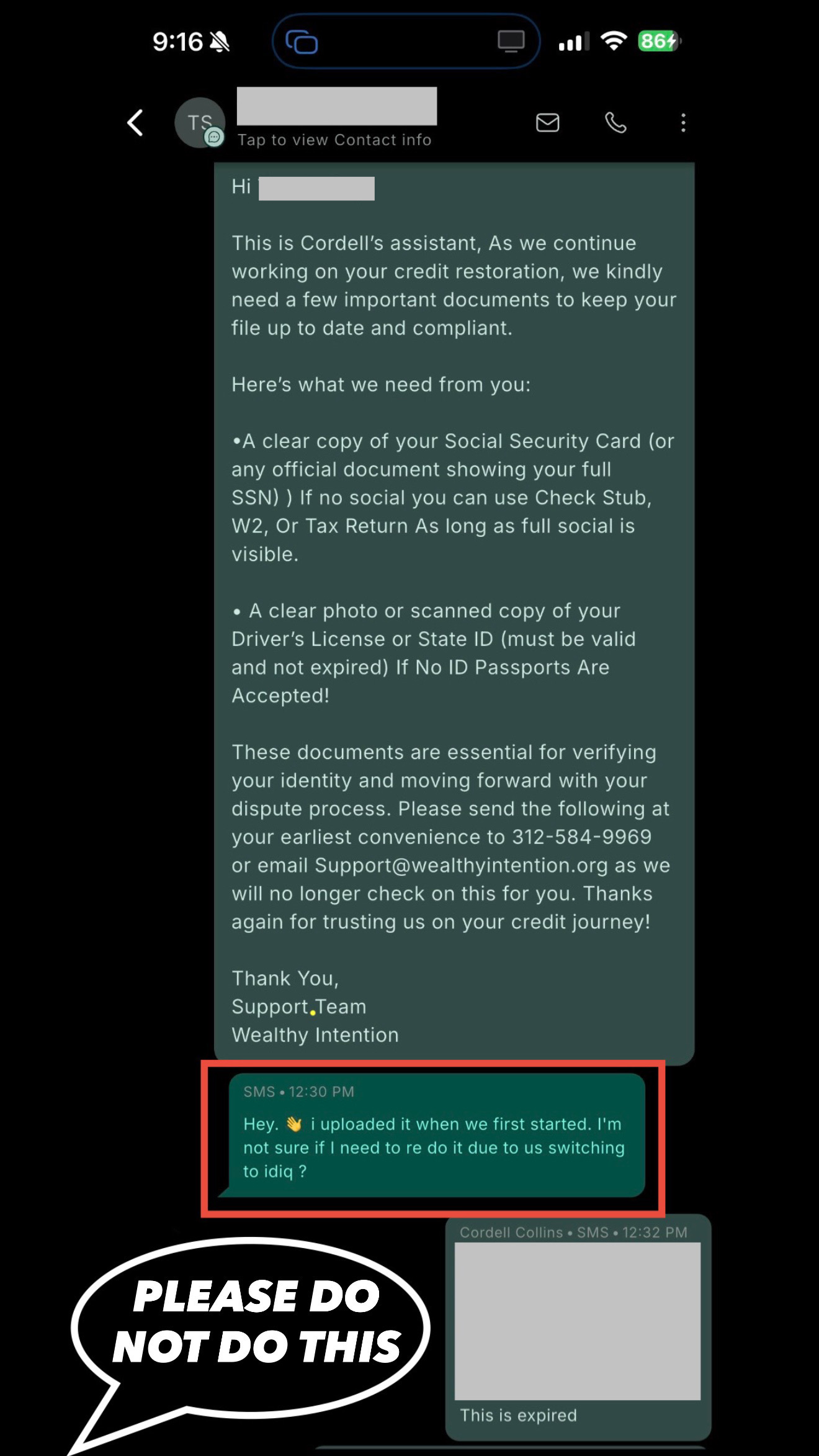

Please understand that every time dispute letters are sent, we must verify your identity. Which means that your Driver's License Or State ID along with your MOST RECENT Proof of Address is required for every round. If your ID or License were to ever expire, my support team will request an updated version and if it is not provided, I cannot proceed with the next round of disputes.

Here's what we need from you:

- A clear photo or scanned copy of your Driver's License or State ID (must be valid and not expired). If No ID, Passports Are Accepted!

- A clear copy of your Social Security Card (or any official document showing your full SSN). If no Social Security card, you can use a Check Stub, W2, Or Tax Return as long as the full Social is visible.

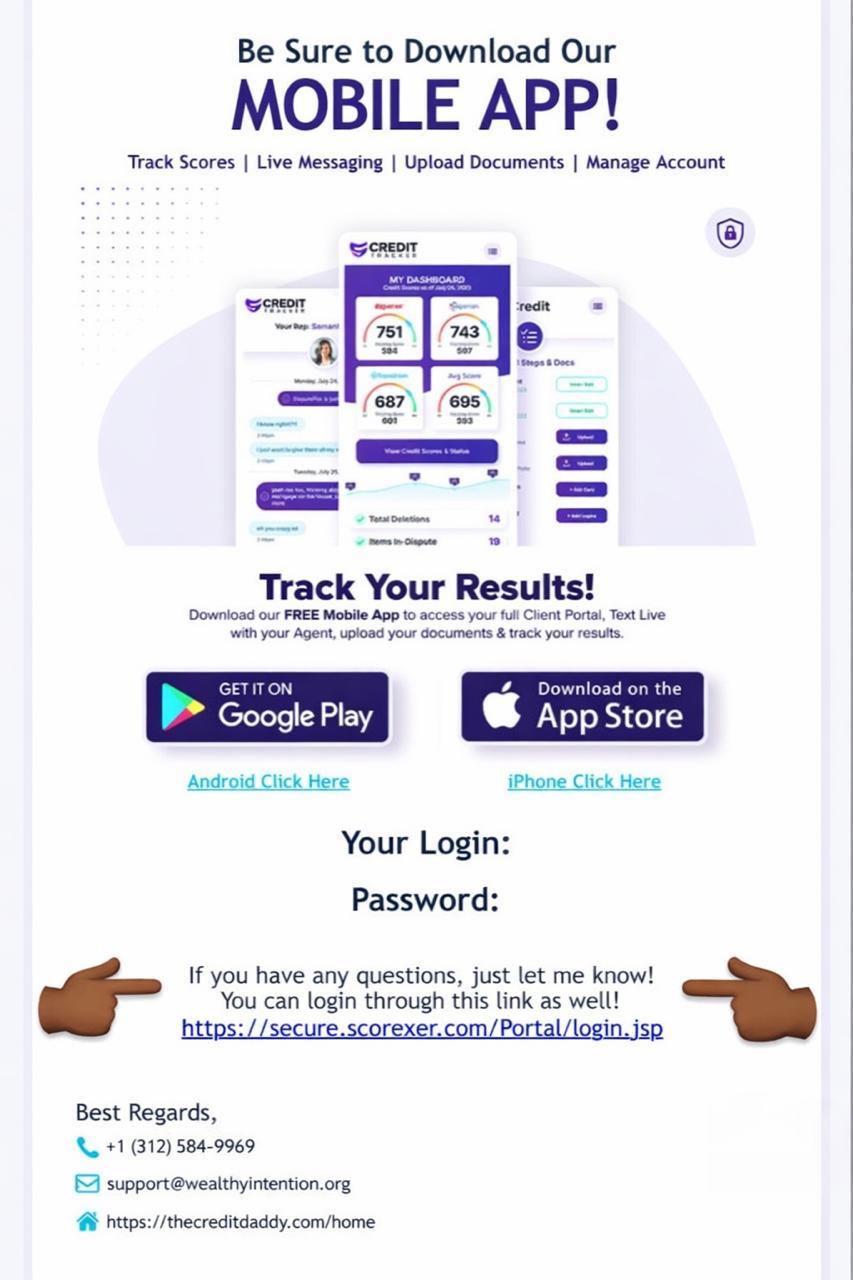

Please upload in your client portal or send the following at your earliest convenience to 312-584-9969 or email [email protected] as we will no longer check on this for you until notified. Thanks again for trusting us on your credit journey!

If you receive an email or text message regarding an issue, it is not sent without cause and is not a system error.

In most cases, either:

- Our team was not notified that the issue has been handled, or

- The issue has resurfaced and requires immediate attention

- The login information provided is invalid

- The submitted documentation is outdated or invalid

That said — these notifications should NEVER be ignored.

Before responding with "I've already completed this," please take a moment to verify first, and provide a screenshot as proof if you believe the issue has already been resolved.

Confirm all documents are clear, dates are accurate, and all submitted documents are up to date.

Thank You,

Support Team — Wealthy Intention

Frequently Asked Questions

Common questions about the credit repair process and what to expect

Different Websites And Logins

Just so there is no confusion about the websites and logins, understand that there are only 3 websites and logins.

1. Credit Monitoring Platform (Required)

When you first got started with our program you enrolled in one of the following credit monitoring services (which one you have depends on when you got started):

- IdentityIQ — https://member.identityiq.com/

- MyFreeScoreNow — https://member.myfreescorenow.com/login/

Important: You only need ONE of these platforms (not both).

This platform is used to:

- Monitor your credit

- View your full credit report

- Assist in generating dispute activity

Password Requirement: Please set your password to Credit@2025

2. Client Education & Resource Hub

The second platform is TheCreditDaddy.com. This website is used for:

- Frequently Asked Questions (FAQs)

- Education & Training

- Rules & Expectations

- Client To-Do List

- 24-Hour Support Chat

- Booking Consultations

- Refer A Friend

- Suggestion Box

- Available Resources

- Important Things That Can Hold You Back

All of this information can be found under the "Active Client" tab.

Access Password: Credit123!

3. Client Portal (Scorexer)

The final platform is your personal client portal (also available on an app called Credit Tracking):

https://ceoacademy.scorexer.com/Portal/login.jsp

This portal is used for two primary purposes:

1. Track Your Progress

- Monitor dispute activity

- View updates on your account

2. Upload Important Documents

Upload documents we request from you, or that you feel may help us with the process, such as:

- Proof of Address (POA)

- Driver's License / State ID / Passport

- Proof of payment for accounts in collections

- Identity theft documentation (e.g., police reports)

- Relevant screenshots, emails, mailed letters, or correspondence

Important Notice: You must sign the agreement after logging in before everything becomes available. Also, if we are unable to access your credit monitoring account, we will not be able to update your progress within your client portal.

Password Setup: You will receive a temporary password via email but may create your own password for this platform, as it serves as your personal and secure client portal.

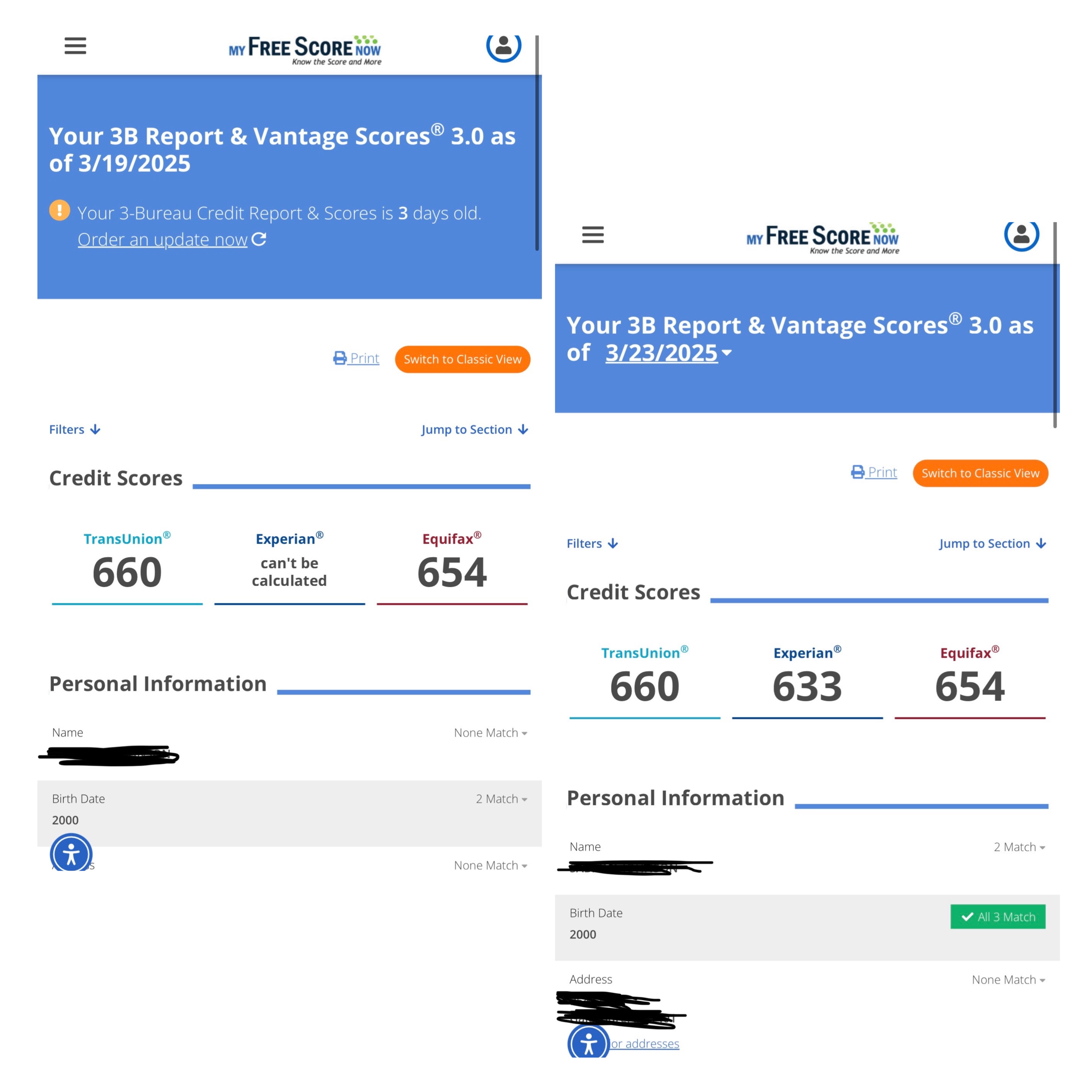

Why Isn't My Credit Score Showing For All 3 Bureaus?

Usually this happens when an old address gets deleted. Your old accounts were attached to that address so now since no old or current accounts are attached to your current address there is nothing to show on your credit report. But no worries this is an easy fix.

Step 1: MFSN USERS ONLY

(888) 548-2008 (Press Option 2)

Call Customer Service to let them know about the issue. They may mention an old address that they had on file. You can let them know that address is incorrect and provide them with your current address. Once you verify your CURRENT ADDRESS they should be able to resolve it. If not, please view step 2.

Step 1: IDIQ USERS ONLY

(877) 875-4347 (Press Option 2)

Call Customer Service to let them know about the issue. They may mention an old address that they had on file. You can let them know that address is incorrect and provide them with your current address. Once you verify your CURRENT ADDRESS they should be able to resolve it. If not, please view step 2.

STEP 2: Call The Bureaus Directly

This step is FOR BOTH IDIQ & MFSN users BUT ONLY if step one didn't work.

You only need to call for whichever bureau is missing. So if your reports and scores aren't showing for both Equifax & Transunion, then you will call both and give them both the same exact rundown.

- Transunion: 800-916-8800

- Equifax: 800-685-1111

- Experian: 888-397-3742

Give them a call (Press 0 To Get To A Live Person):

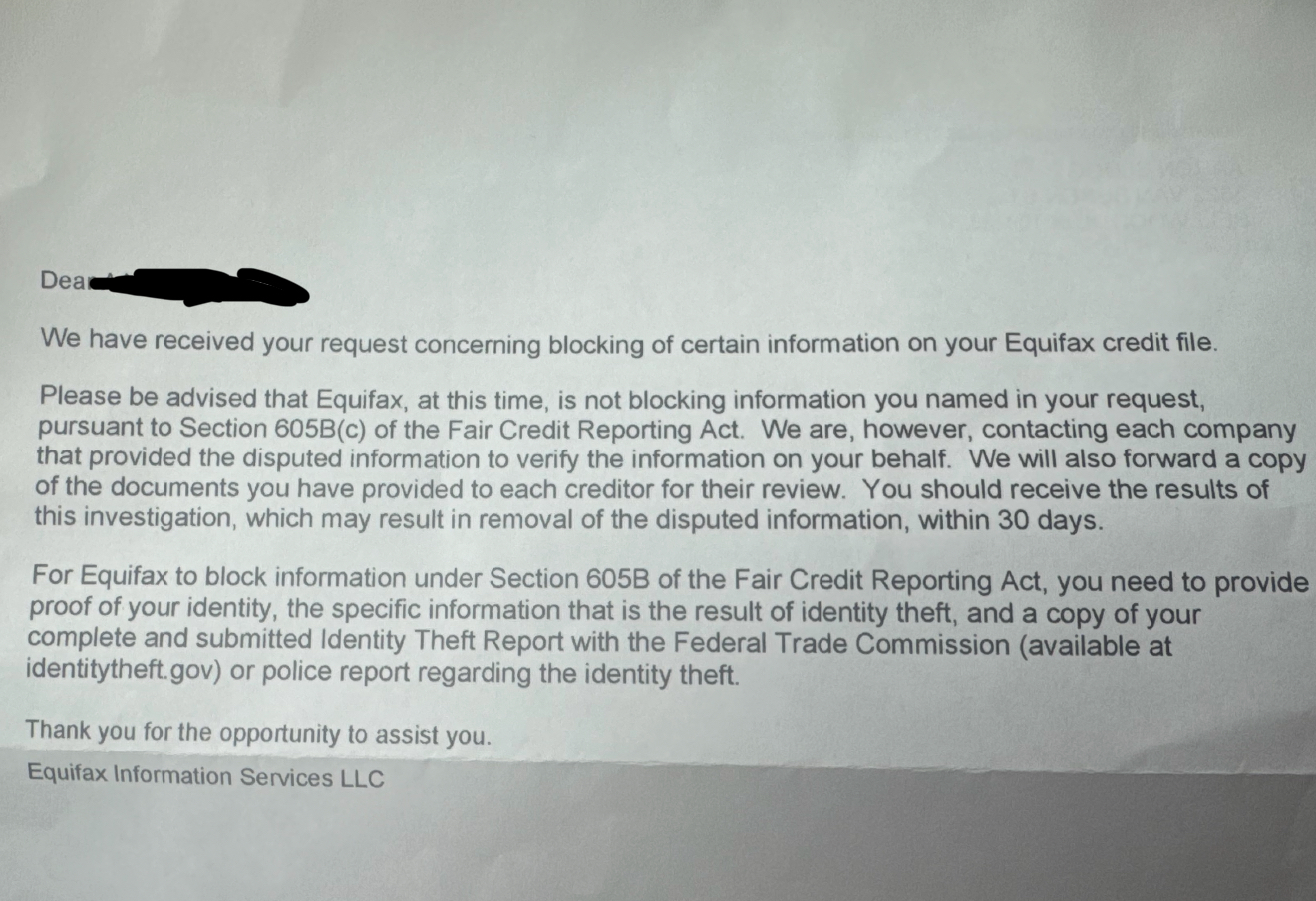

"I sent some disputes for my credit and I received something that said I couldn't be verified."

Wait for a response and make sure to update all your information.

"I would like to remove any information that I did not mention due to it being inaccurate. My Only Name Is... My Only Address Is... My Only DOB Is..."

"Can we please get this fixed so that they can furnish my credit report because it's holding me back from getting approved from housing which is a violation of my consumer right."

Ask how long it will take before your credit report will show up. They may ask you to send them a "cover letter". Please make sure your State ID or Driver's License is updated with your current address BEFORE sending out this cover letter.

STEP 3: Cover Letter (only if asked to provide)

You only need to send a cover letter for whichever bureau is missing. If missing for two, send two separate letters.

Addresses:

- Equifax: P.O. Box 740256, Atlanta, GA 30374

- Experian: P.O. Box 4500, Allen, TX 75013

- TransUnion: P.O. Box 2000, Chester, PA 19016

Date: __________

To Whom It May Concern,

I am writing to verify my identity so that my [Bureau Name] credit report and score can be released and made available.

My information is as follows:

Full Name: __________________________

Date of Birth: ______________________

Last 4 of SSN: ______________________

Current Address: ___________________

City, State, Zip: ___________________

Phone Number: _____________________

I have enclosed copies of my government-issued photo ID and proof of address for verification. Please process my identity verification as soon as possible so my credit file can be properly displayed.

Sincerely,

________________________ (Signature)

________________________ (Printed Name)

Documents to Include (VERY IMPORTANT):

- ✅ Copy of Driver's license or state ID (cannot be expired)

- ✅ Proof of address (utility bill, bank statement, or lease — dated within 60 days)

After you make the phone calls to customer service or send the cover letters, your credit reports and scores should reappear by your next credit report at the latest. Sometimes it will appear the next day.

How To Read Your Credit Report

A credit report is a detailed record of your credit history and financial behavior. It shows lenders, banks, and creditors how you have managed borrowed money over time.

In the United States, credit reports are maintained by the three major credit bureaus: Equifax, Experian, Transunion

These companies collect information from lenders, credit card companies, and collection agencies to build your report.

What Information Is On a Credit Report

This section identifies you. It may include:

- Full name and any previous names used

- Current and previous addresses

- Social Security number (partially masked)

- Date of birth

- Employers (past and present)

What you want to see

Ideally your report should display: one name, one current address, one date of birth, one current employer.

Multiple variations can create inconsistencies that allow negative accounts to remain linked. Contact bureaus directly to correct:

- Equifax — 800-685-1111

- Experian — 888-397-3742

- TransUnion — 800-916-8800

Keep your ID updated with your current address — bureaus may keep old addresses accurate if your ID still shows them.

It's your credit grade — a number that tells lenders how risky or reliable you are.

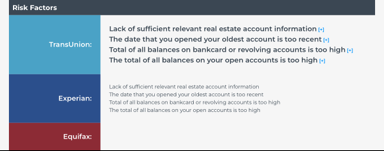

Risk Factors are the key reasons why your credit score is not higher.

👉 In simple terms: They tell you what's hurting your credit the most right now. They show exactly what to fix and give insight into how lenders view your profile.

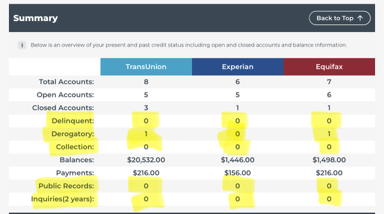

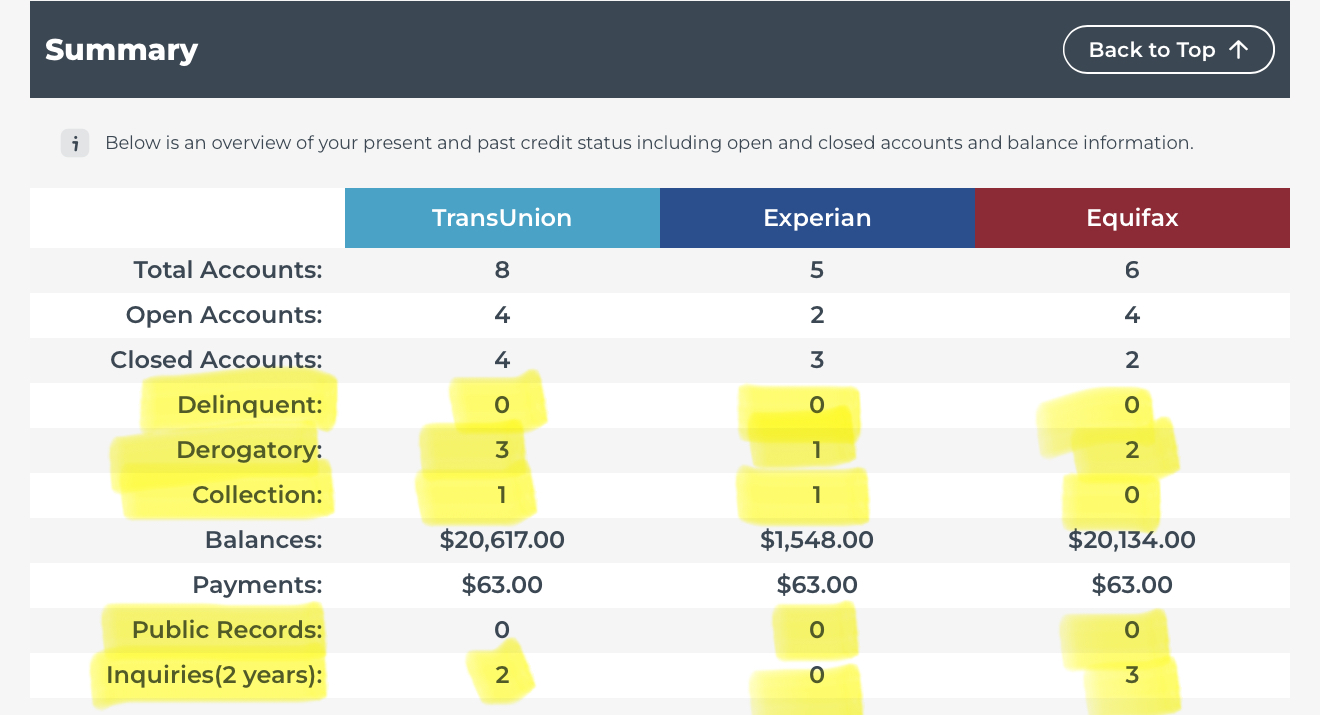

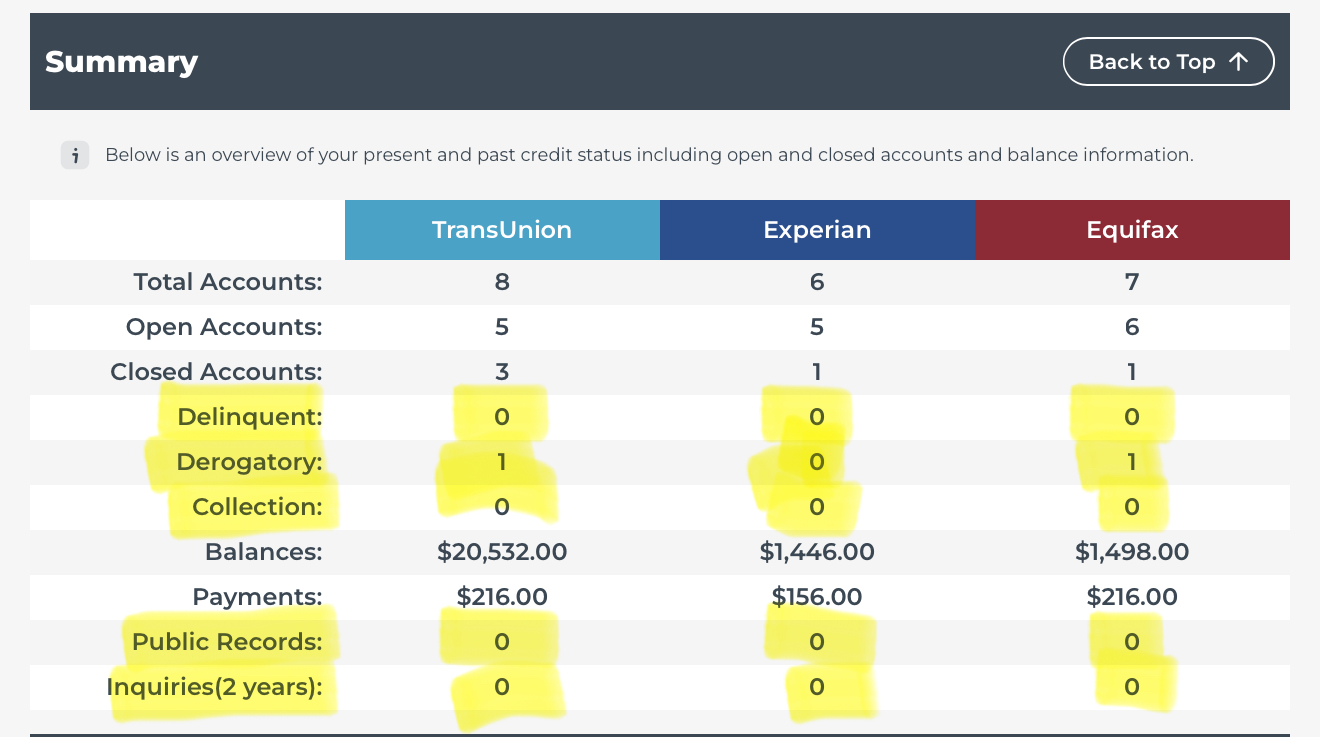

The Summary is a quick overview of your entire credit profile.

👉 In simple terms: It's a snapshot that breaks down everything on your credit report at a glance. ( Soft Pulls & Pre-Approvals )

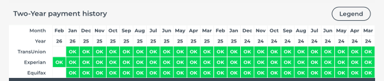

Account History is a detailed record of how an account has been managed over time — especially your payment behavior month by month.

👉 In simple terms: It shows your track record for all accounts both open and closed.

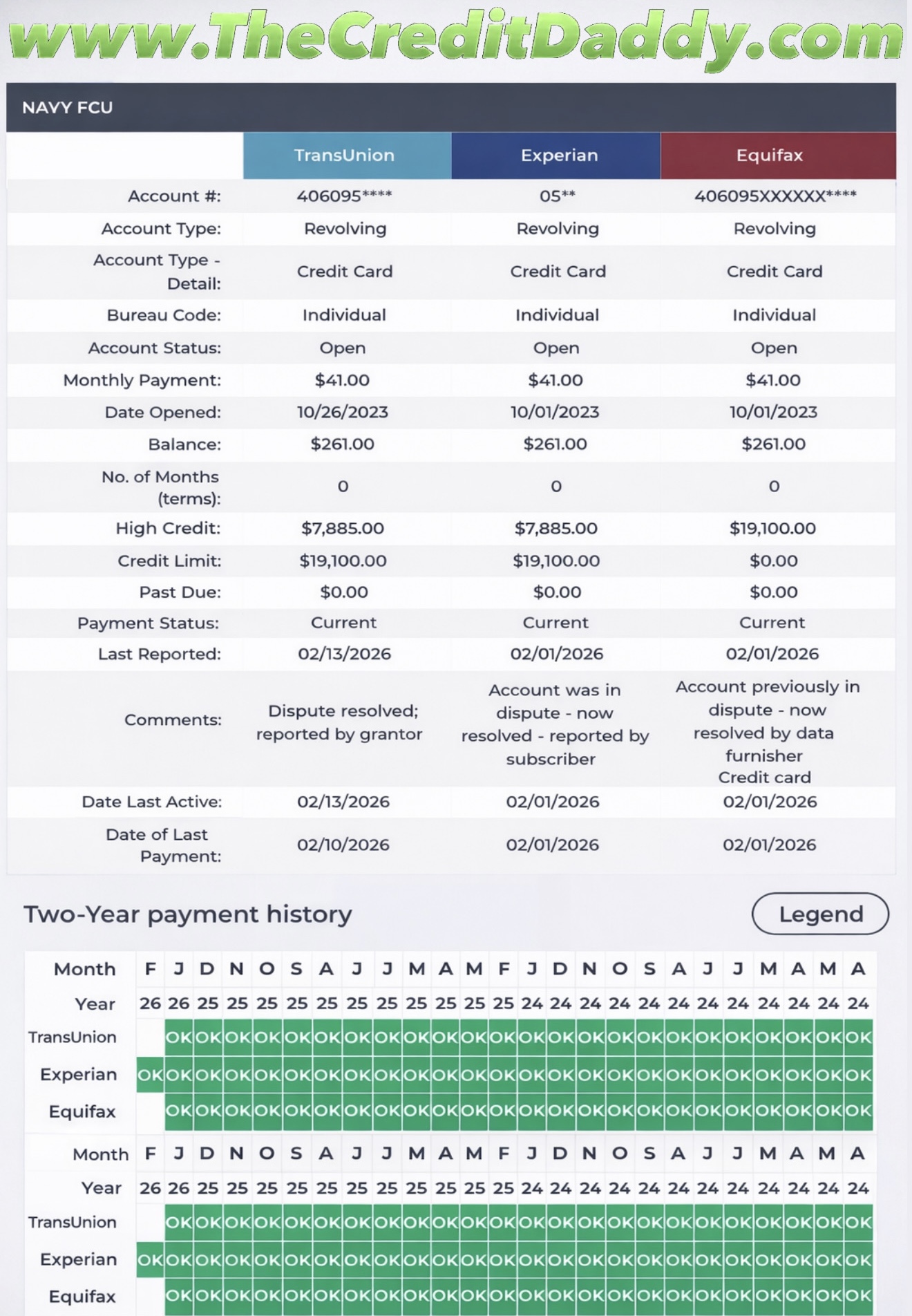

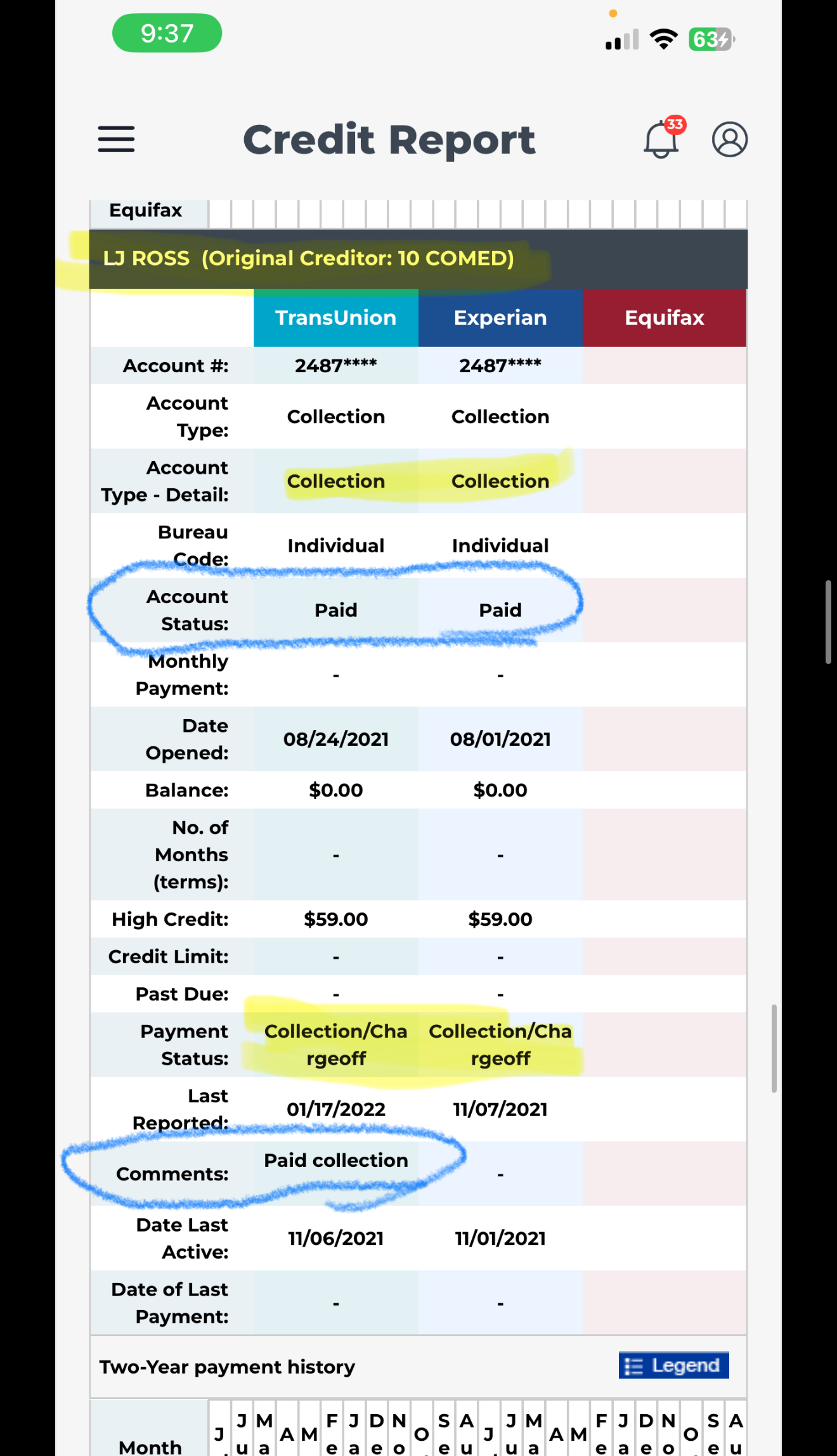

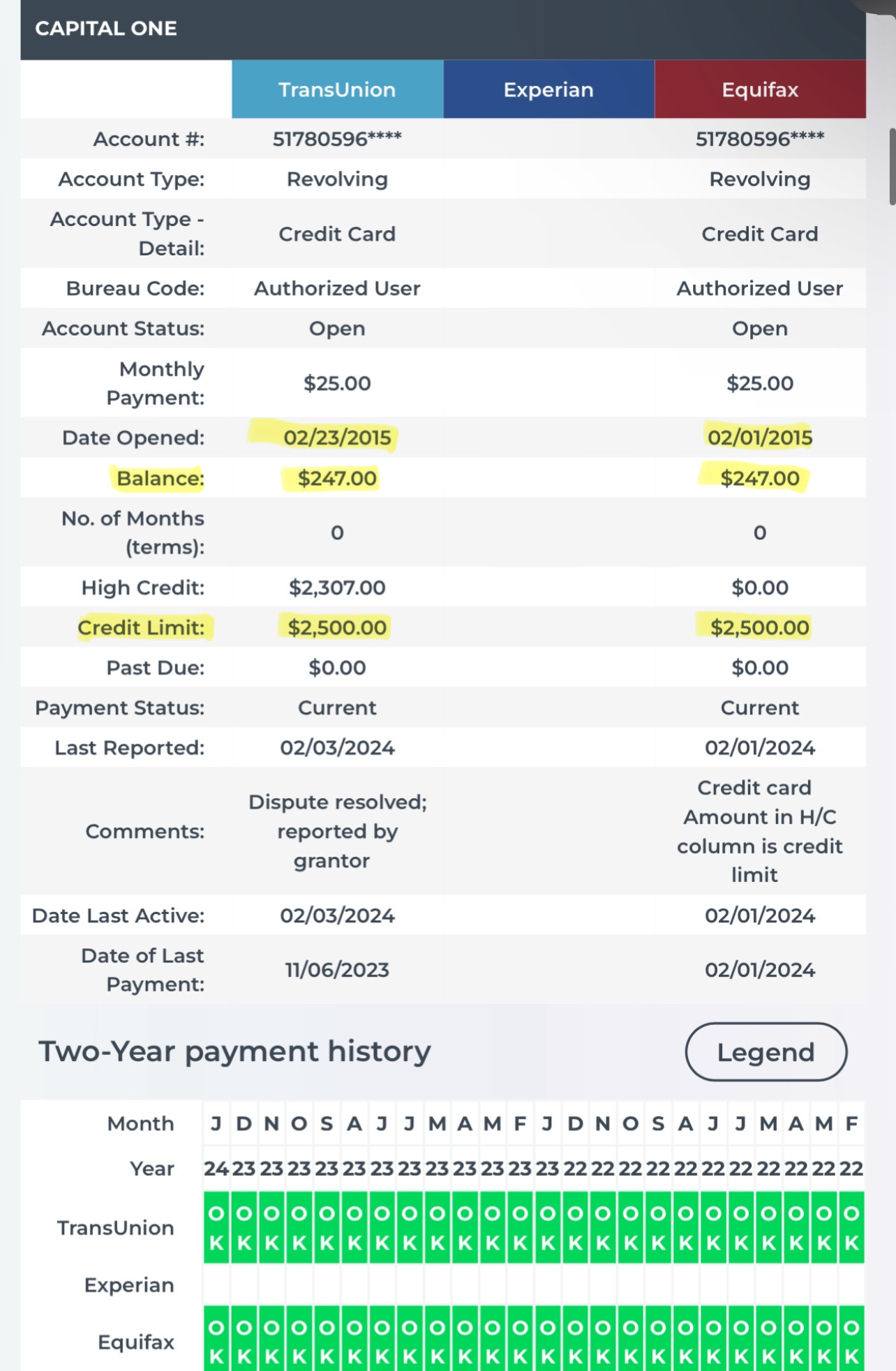

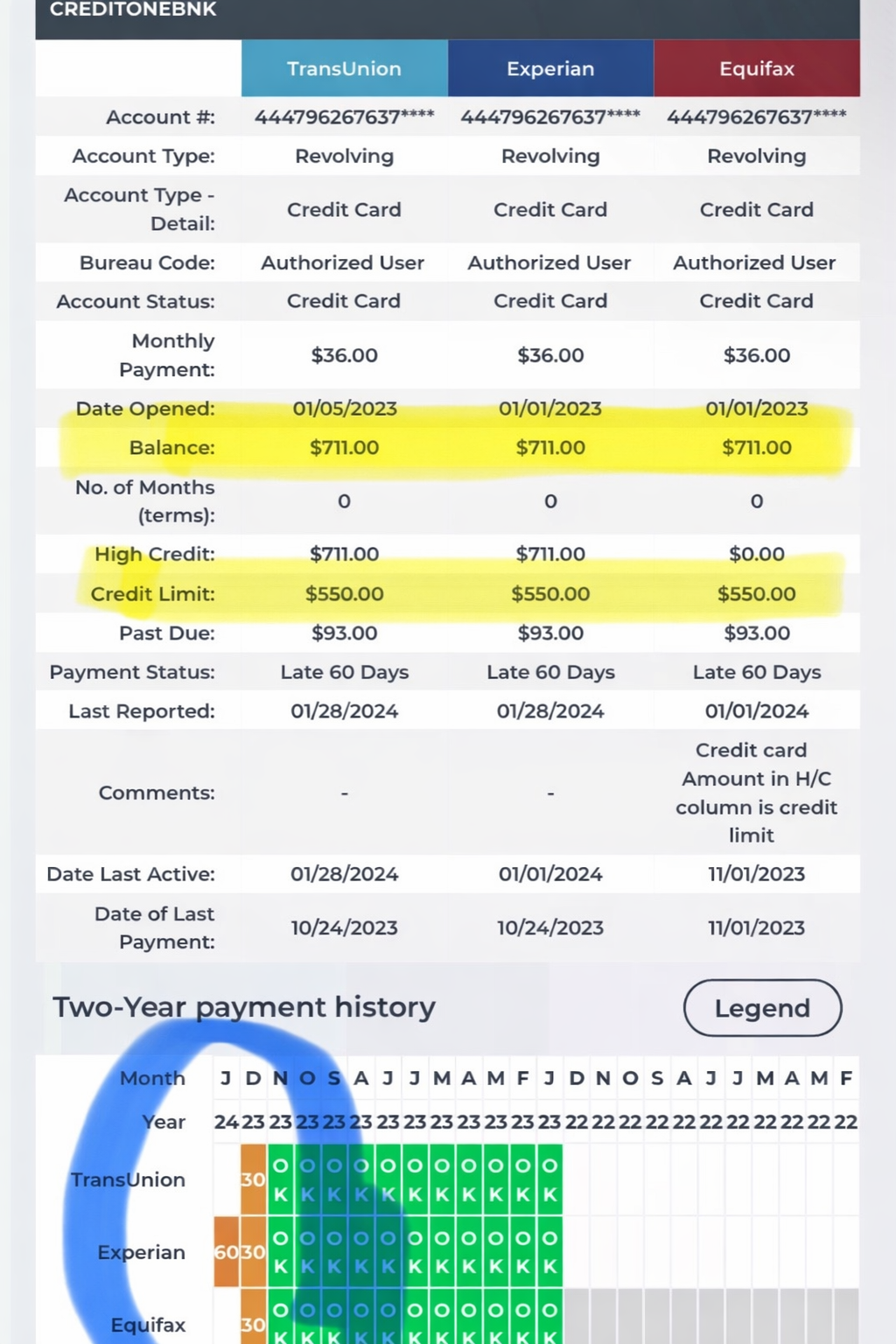

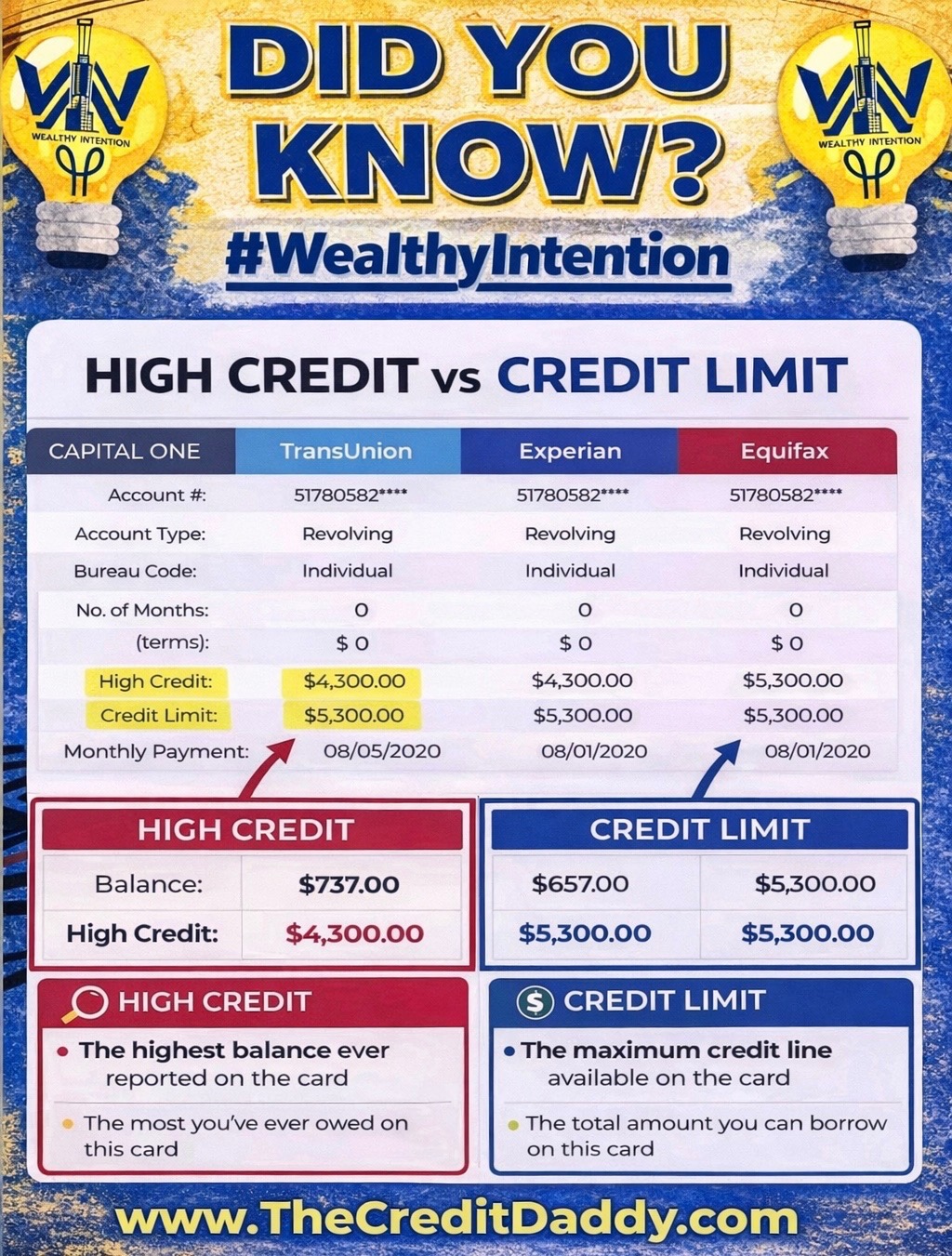

What Each Field Means:

| Field | Definition | Example | ACTUAL |

|---|---|---|---|

| Account #: | Unique identifier assigned by the creditor. May show partially masked. | Full: 1234567890 • Report: XXXXXX7890 | 31** |

| Account Type: | General category of the account. | Revolving, Installment, Open Credit | Revolving |

| Account Type - Detail: | More specific account description. | 💳 Credit Cards: Bank, Retail, Secured 🚗 Loans: Auto, Personal, Student, Mortgage | Credit Card |

| Bureau Code: | Your role on this account. | Individual, Authorized User, Joint, Co-Signer | Individual |

| Account Status: | Open or closed, positive or negative. | Open, Closed | Open |

| Monthly Payment: | Min amount required monthly to stay in good standing. | Balance: $2,000 • Min: $60 📘 Pay $60 to avoid late | $20.00 |

| Date Opened: | Exact date account was created. | Opened Feb 1, 2024 📘 Active 2+ years | 02/01/2024 |

| Balance: | Total amount currently owed. | $756.00 | $756.00 |

| No. of Months (terms): | Total repayment period agreed. 0 for revolving accounts. | 0 | 0 |

| High Credit: | Most ever spent on card, or original loan value. | Limit: $5,000 • Most used: $3,200 📘 High Credit = $3,200 | $4,787.00 |

| Credit Limit: | Max amount lender allows you to borrow. | Limit: $5,000 • Balance: $1,500 📘 $3,500 still available | $11,100.00 |

| Past Due: | Amount owed that should already be paid. $0.00 is good. | Payment: $150 • Missed 2 months 📘 Past Due = $300 | $0.00 |

| Payment Status: | Current condition of account and payment behavior. | Current, Collection/Charge-Off | Current |

| Last Reported: | Most recent date creditor updated the bureaus. | Last Reported: 02/15/2026 | 02/06/2026 |

| Comments: | Notes added by creditor or bureau with extra details. | "In collections" ❗ "Settled for less" ⚠ | - |

| Date Last Active: | Last time account was used or had movement. | Used Jan 10, 2026 📘 Last Active = 01/10/2026 | 02/01/2026 |

| Date of Last Payment | Last time you actually made a payment. | Payment Feb 5, 2026 📘 Last Payment = 02/05/2026 | 02/01/2026 |

This is one of the most important parts of the report. It shows:

- On-time payments

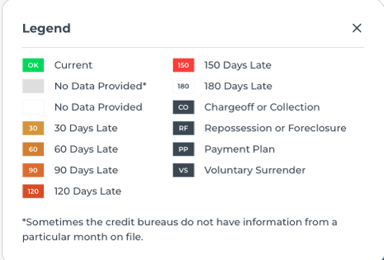

- Late payments (30, 60, 90, 120 days late)

- Collections, Charge-offs or repossessions

Your payment history heavily influences your credit score.

Legend:

Account Inquiries are records of who has accessed your credit report and when.

👉 In simple terms: They show who checked your credit and why.

- Hard inquiries – when you apply for credit (can affect score)

- Soft inquiries – background checks or checking your own credit (no impact)

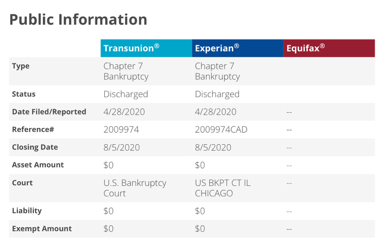

Some serious financial events may appear here, such as:

- Bankruptcies

- Tax liens

- Civil judgments (less common now)

Creditor's Contact Information provides the details of the company that owns or reports the account.

👉 In simple terms: It tells you who to contact about that account.

How Does The Process Work / What's Included?

- We send out customized letters to the credit bureaus to challenge for removal of negative items off your file and clean up your report. Things like charge-offs, collections, late payments, inquiries, derogatory, evictions and even repossessions.

- You will Be required to pay $33/month To monitor your Credit until we're done with your profile. It's like a credit karma but it's more accurate and shows everything we need to see.

- Each round takes 45 days for updates and results! (approximately one and a half months) You will have access to your own personal portal to track the progress as we go! 24/7 access!

Step 1: Credit Repair

My primary responsibility is to dispute inaccurate, unverifiable, and negative items on your credit report. That is the service you are paying for.

Step 2: Credit Growth

In addition, I provide all clients with guidance on how to properly build and maintain their credit scores by giving them a TO DO LIST.

Step 3: Profile Building

I also coach clients on how to develop a strong credit profile and assist with applying for credit cards when the timing is appropriate. THIS IS ALSO INCORPORATED WITHIN THE TO DO LIST.

Step 4 : Execution

This is when I assist clients who are ready to pursue business funding or apply for major financing such as a home or vehicle. While this level of involvement is not required of me, I choose to provide it because I genuinely care about my clients' long-term success.

It's important to understand that a 750 credit score alone does not automatically mean you have GOOD CREDIT. True credit strength consists of:

- A good score (typically 720+),

- A clean credit report, and

- A strong overall credit profile.

Step 5: LLC Setup/ Business Funding ( BONUS )

Regarding business credit, I educate clients on how to properly set up an LLC, establish relationships with banks, and position themselves to qualify for business funding. My goal is to teach clients how to apply independently. However, if you choose to have me assist directly with applications, I charge a 10% success fee for based on the approved amount.

I also work with relationship managers at major institutions, including Chase, U.S. Bank, PNC Bank, Truist, Citizens Bank, the SBA, and American Express. These relationship managers are the individuals who actually review and approve applications, and I refer my clients directly to them. Additionally, I offer tradelines & shelf corporations, which function similarly to tradelines but for an LLC.

All Of this is included but understand what you are paying for is CREDIT REPAIR—the process of cleaning and correcting your CREDIT REPORT. When it comes to creditworthiness, your credit report is what gets you approved—not your credit score.

When Will I Start Seeing Deletions & How Long Does Credit Repair Take?

I can't give a specific timeframe for a few reasons:

- Often times clients hold themselves back with the process by not keeping their credit monitoring up to date.

- They don't check their emails for instructions and they don't send in their most recent proof of address every month — and we need that in order to dispute on your behalf.

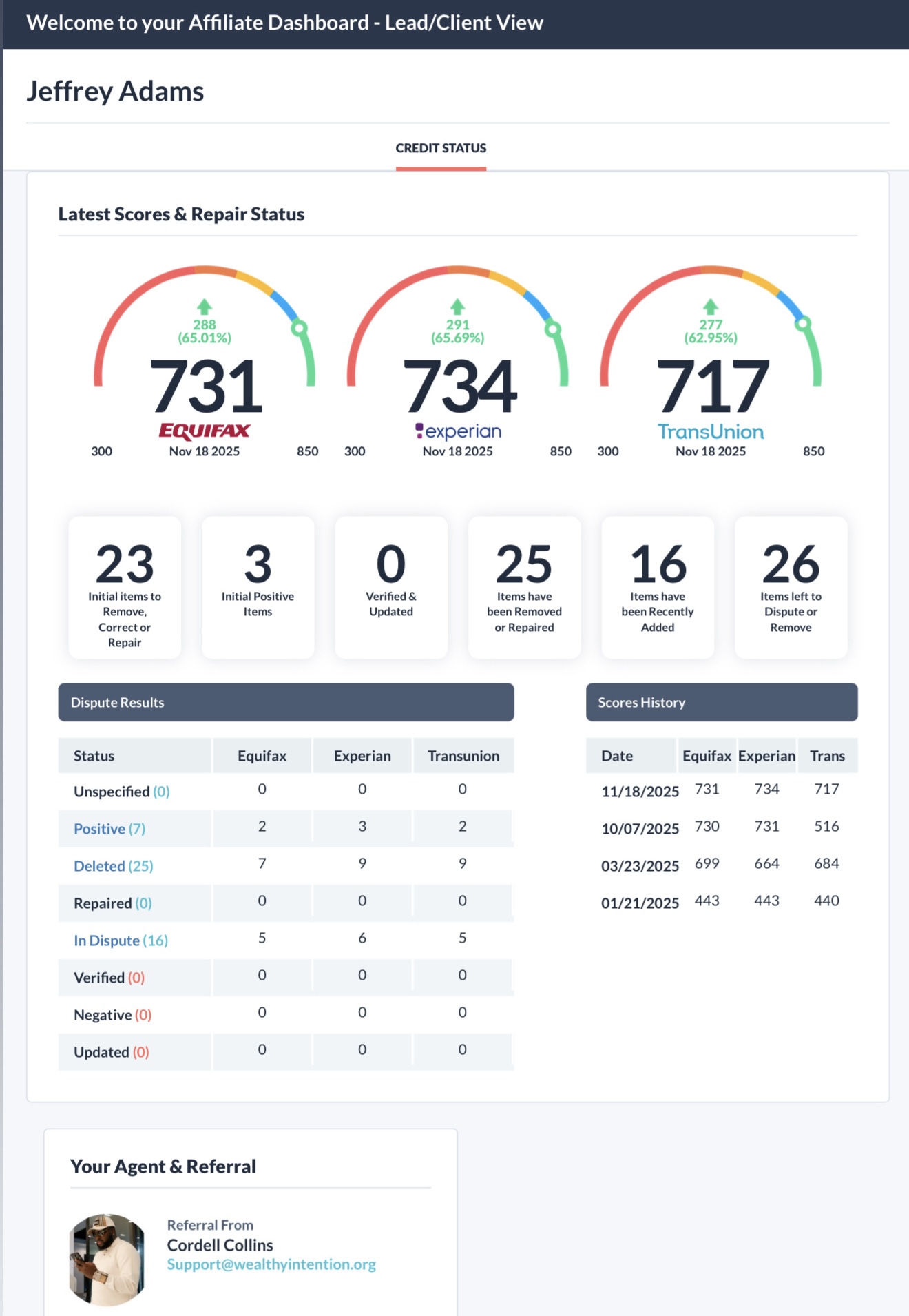

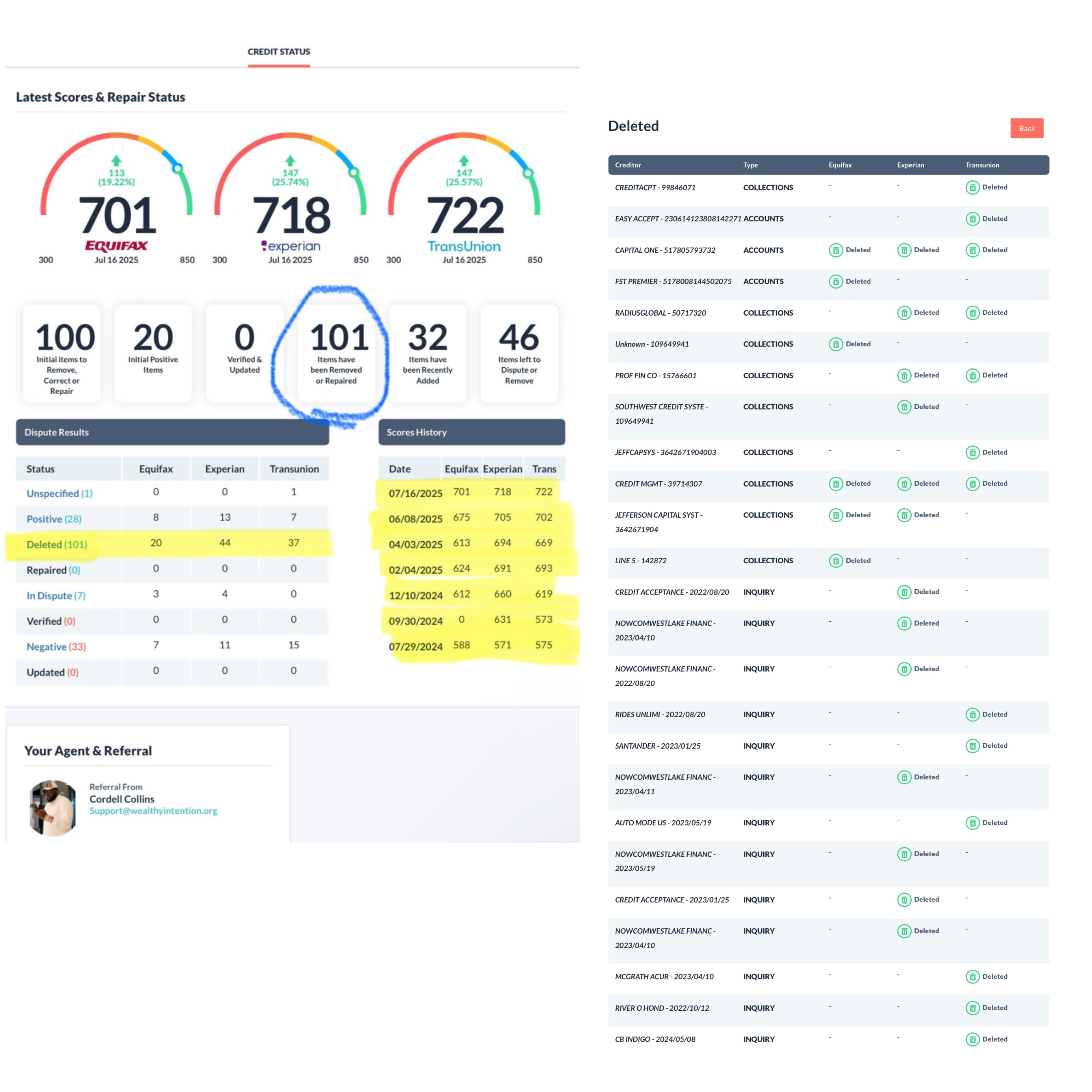

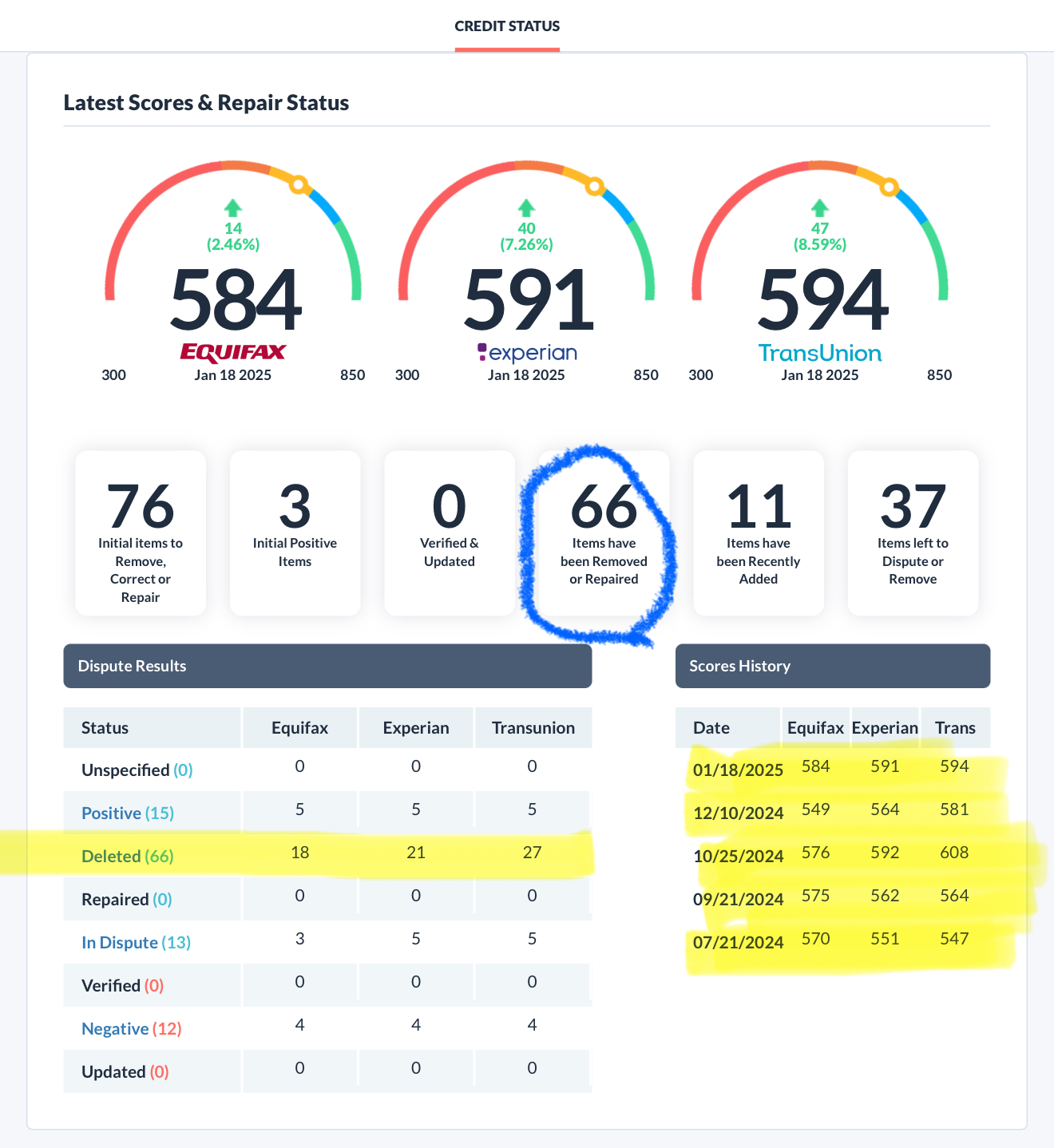

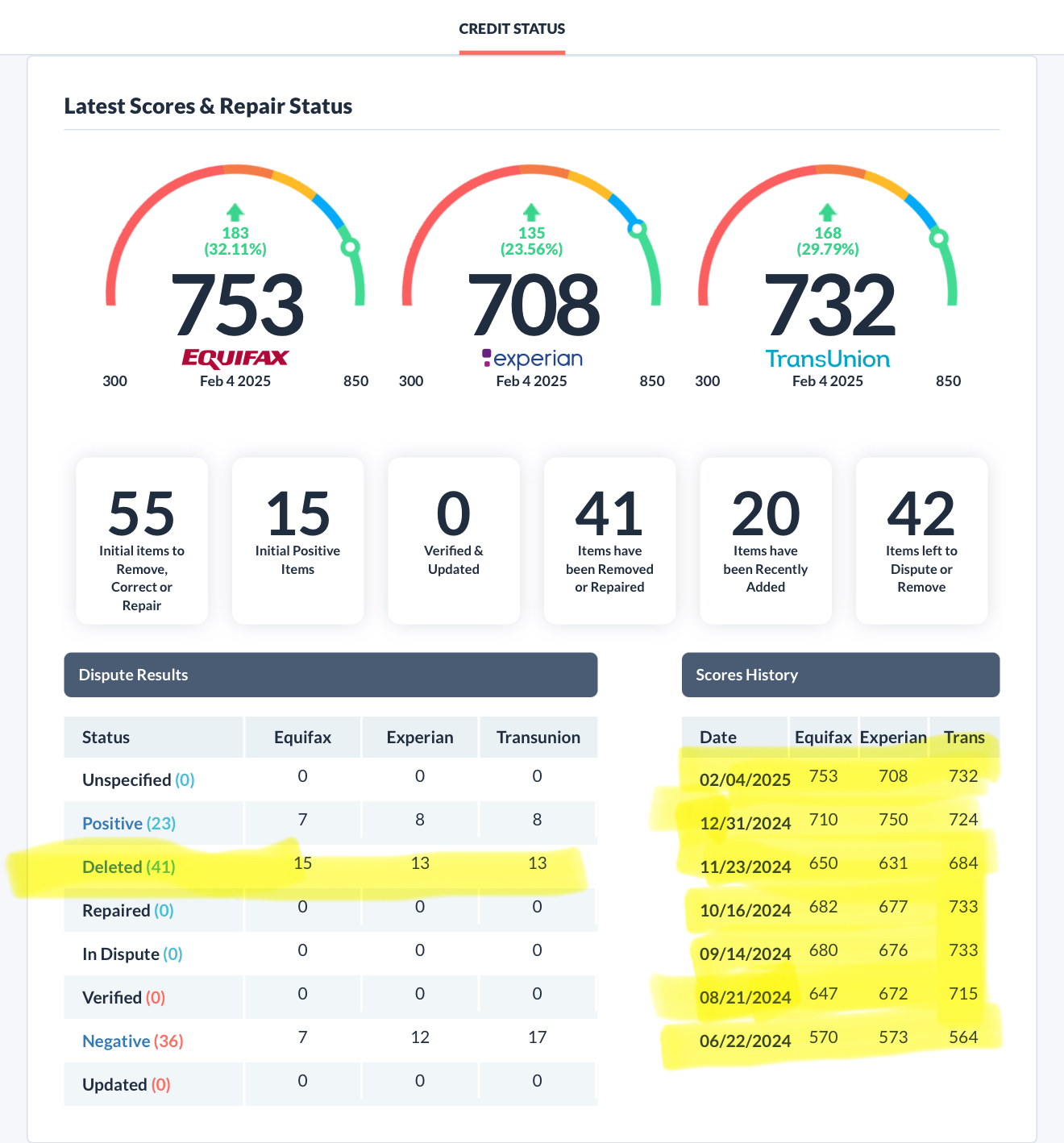

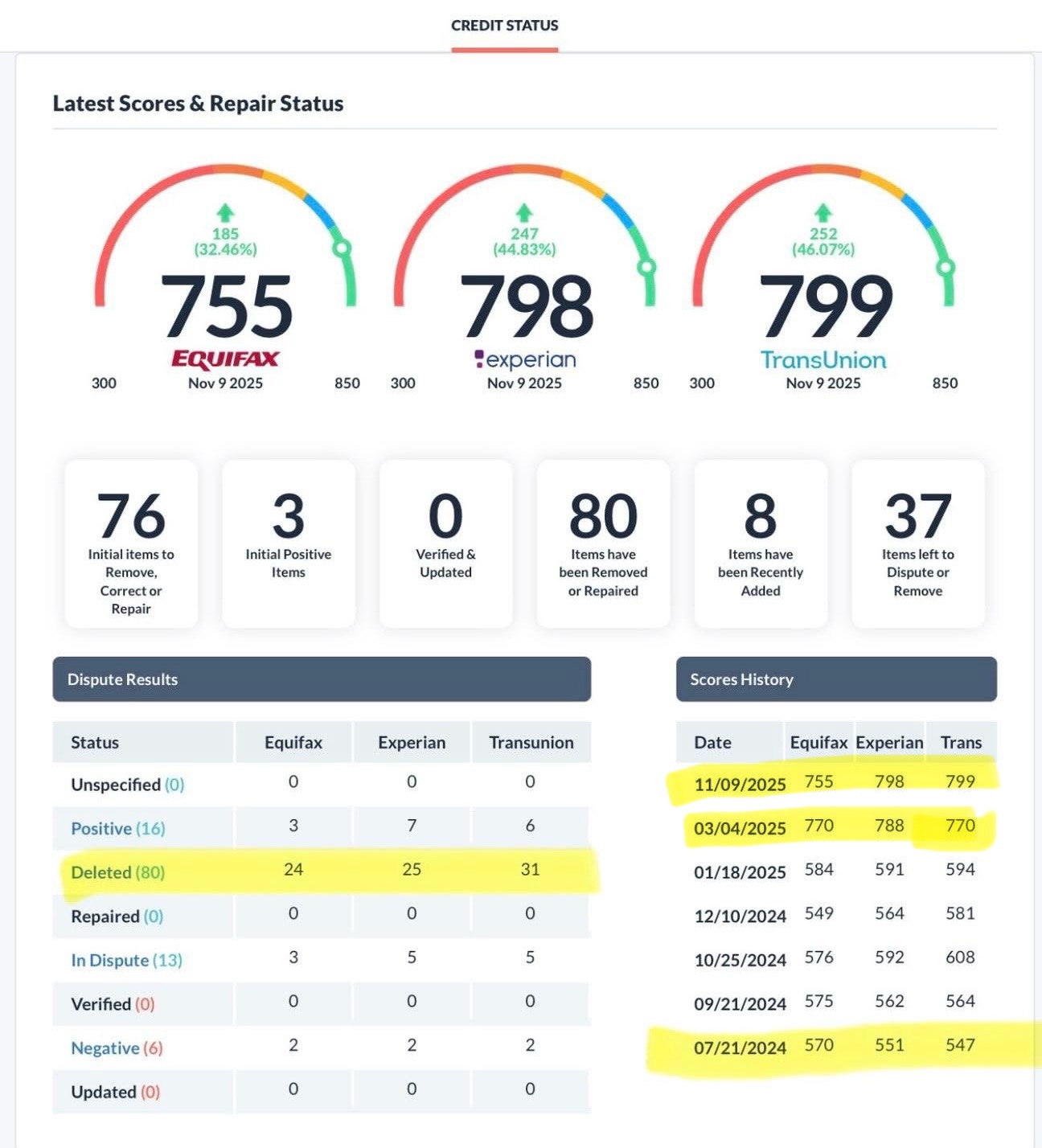

If you look at the screenshot above, you'll see that this client started with 23 negative items and we actually got 25 negative items deleted. Which means 2 additional negative items appeared after he started, and we got those removed as well — resulting in a completely clean credit report.

If you pay attention to the dates on the right-hand side, you'll see this client started Round 1 on 1-21-25 and Round 2 on 3-23-25. However, the next round did not begin until 10-7-25. From the outside looking in, it may appear that no work was done for 8 months, but that is not the case.

In most situations, delays like this happen because the client either did not maintain their credit monitoring subscription (which prevents me from accessing your credit report), or the client failed to submit an updated Proof of Address (POA) every single month.

Please understand, every time dispute letters are sent, we must verify your identity. Your Proof of Address is required for every round, and if it is not provided, I cannot proceed with the next round of disputes.

These two things alone can prolong a client's results for months or even up to a year — which would not be my fault as long as I send out emails and texts notifying them. So his total timeframe took a total of 10 months. 10 months, although it could have potentially been significantly shorter without delays.

On top of that, the credit repair timeline varies from person to person, depending on the number and type of negative items on the credit report.

Success Stories:

• Fastest deletion: Eviction removed in just 14 days

• Quickest full clean-up: 88 total negative items cleared within 45 days

That said, results like these are possible but not typical and cannot be guaranteed for every client — no one in this industry can honestly make such a promise. If they do, they're telling you what you want to hear so you feel comfortable enough to give them your money because they know you're in a rush & most likely desperate.

Realistic Expectations:

On average, credit repair takes 6 to 9 months, and in more severe cases, it can take up to a year.

I believe in full transparency: credit repair should take as long as it needs to take. Anyone guaranteeing complete results in 30–60 days is not being realistic. The average client goes through 4–7 rounds of disputes. If it were that simple, multiple rounds of disputes wouldn't even exist.

Unfortunately, many companies lie for sales, which gives credit specialists a bad reputation. My approach is different — I prefer honesty over hype. MY NAME IS MORE IMPORTANT THAN YOUR MONEY! I will let anyone walk before I tell them what they want to hear. It's not about what you want — it's about how the process actually works. Results take time, but they do come. Will it take the full 6–9 months, or even a year? Not necessarily, but you should be prepared for that timeframe.

Each dispute round lasts approximately 45 days, and after every round, you will receive a detailed PDF update outlining any deletions or changes that occurred.

See Real Results:

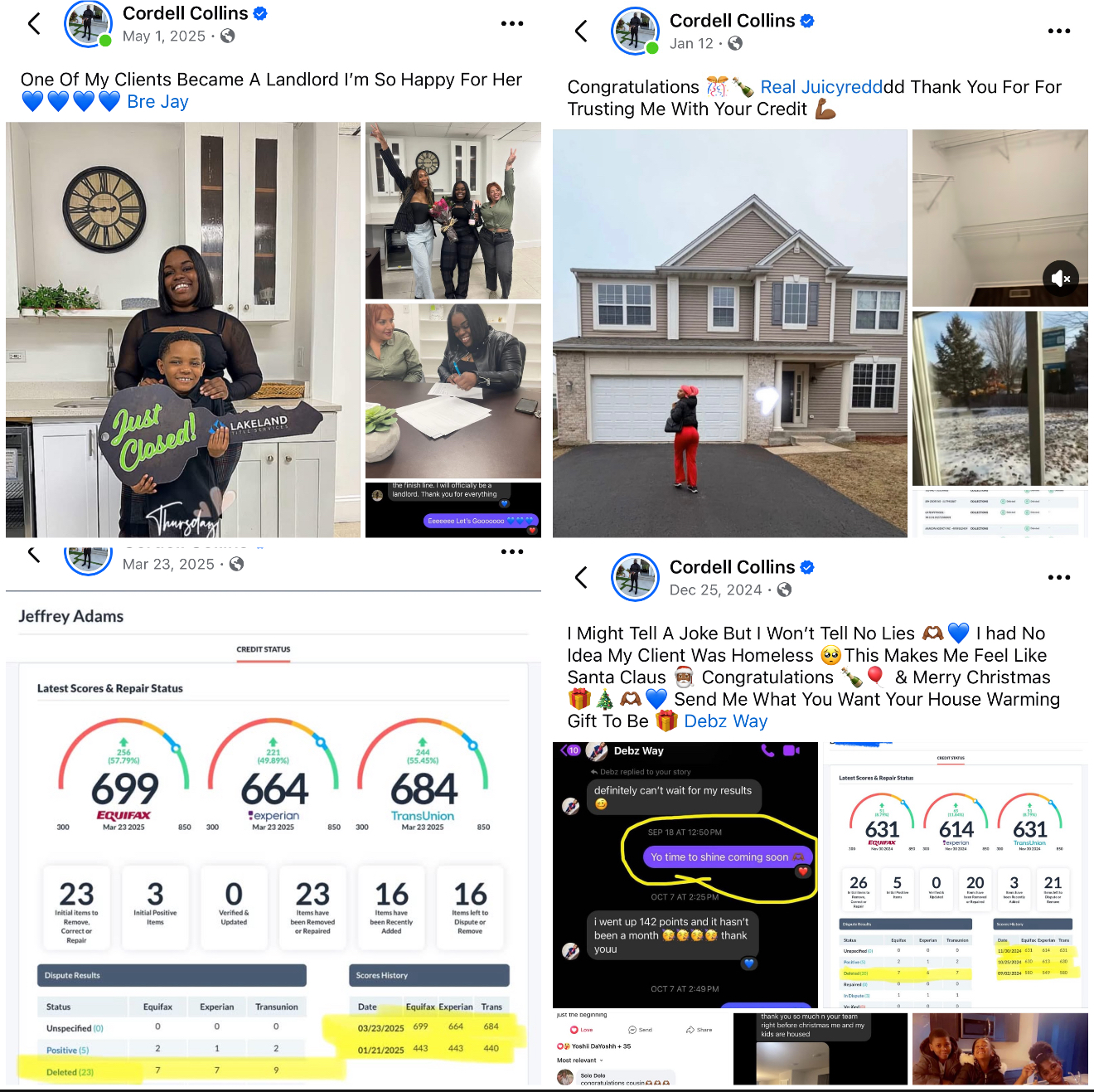

If you click this link you can look at the credit scores and deletions for some of my clients and kind of do the math on how long it took — do with that what you will. Also, a lot of the shares are from some of my real clients.

www.TheCreditDaddy.com/results

Why Haven't I Received Any Updates?

I would like to take a moment to clarify how updates are provided throughout the credit improvement process.

First, it is important to understand that not receiving a formal update from us does not necessarily mean there has been no progress. Many clients receive updates directly through creditor notifications, emails, mailed correspondence, or alerts from their credit monitoring service indicating deletions or changes. In addition, you also have access to your client portal, where updates may be reflected. All of these notifications are considered valid updates.

That said, we intentionally provide formal PDF updates because they are more professional, easier to review, and help clients feel confident and informed about their progress.

Misconceptions

Please understand that an update is strictly just an update. It does not guarantee a score increase every round or that something will be deleted every round. You can expect certain rounds—and sometimes back-to-back rounds—with no change, and that is completely normal and part of the process.

Believe it or not, this actually helps increase your chances of deletions, as it Helps Us Catch The Credit Reporting Agencies & Debt Collectors Up In Violation Even More Than They Already Were.

Update Timeline

Each dispute round operates on a 45-day cycle (approximately one and a half months). Updates are scheduled according to this timeline and are dependent on all required documentation and access being current and accurate.

Phase One: Proof Of Identity

The first step before any update can be issued is confirming that we have two forms of Identification on file for you. One being documentation that displays your FULL SSN, and the other being either a valid State ID or Driver's License.

Here's what we need from you:

- A clear photo or scanned copy of your Driver's License or State ID (must be valid and not expired). If no ID, passports are accepted.

- A clear copy of your Social Security Card (or any official document showing your FULL SSN). If no Social Security card, you may use a check stub, W-2, or tax return, as long as the full SSN is visible.

Please understand that every time dispute letters are sent, your identity must be verified. This means your Driver's License or State ID is required for every round. If your ID or License expires, my support team will request an updated version, and if it is not provided, we cannot proceed with the next round of disputes.

Phase Two: Proof of Address (POA)

The 2nd step before any update can be issued is confirming that we have a current Proof of Address (POA) on file. Whenever we request your most recent Proof of Address (POA), we are not asking whether you have moved from your current residence. We understand that your address may remain the same.

What we are specifically requesting is updated documentation that verifies you are currently residing at that address.

There are ONLY Three (3) Acceptable Documents, and we only need ONE out of the three (please DO NOT send anything other than one of these).

- A rental or lease agreement

- A utility bill

- A bank statement

If you don't have your own apartment, obviously you won't have a utility bill or rental agreement. THAT IS COMPLETELY FINE. In your case, you will use your bank statement for the proof of address.

Regarding bank statements, all financial institutions are accepted. This includes, but is not limited to, Chime, Cash App, Apple Pay, Varo, credit card statements, and any major traditional bank.

To be valid, the document must:

- Display your full first and last name (not a business name or nickname)

- Show your complete residential address

- Be dated within the last 60 days

Whenever sending or uploading documents into your portal PLEASE MAKE SURE ALL DOCUMENTS ARE CLEAR:

- Not Too Light Or Too Dark

- No Blurry Photos Or Screenshots

- No shadows blocking words in the documents

- Pictures MUST BE FULL PAGE (Meaning take it out of the mail and unfold it)

- Screenshots Must Also Be FULL PAGE (meaning MAKE SURE ALL 4 CORNERS ARE IN THE PIC)

These things can cause your docs to come back as NON VERIFIABLE—which can prolong you getting fast and efficient results.

If the document is older than 60 days, it is considered outdated and cannot be used. For example, if it is currently December and the document on file is from September or October, it is no longer valid. For this reason, we strongly recommend submitting a new POA every month as soon as it becomes available. Utility bills and bank statements are often delayed, and by the time the next update cycle arrives, a previously submitted document may already be expired. This can cause unnecessary delays for both you and our team.

If you have a rental or lease agreement, that is ideal, as it typically remains valid for an extended period and eliminates the need for monthly submissions.

If your POA is missing or outdated at the time an update is scheduled, we will contact you via email and text message and send up to three reminders. If the issue is not resolved, the process CANNOT move forward.

Phase Three: Credit Monitoring Access

Once the POA is confirmed, the next requirement is accurate and up-to-date credit monitoring access.

Common issues at this stage include:

- Incorrect login credentials

- An outdated credit report

- Required password changes initiated by the monitoring service for security reasons

If we are unable to access your credit report, we cannot provide an update.

It is important to understand the difference between active and updated credit monitoring:

- Paying the monthly fee keeps the account active

- Logging in and refreshing the report ensures it is updated

When you log into your credit monitoring account, the report will display a "last updated" date. That date must reflect the current month. For Example: Let's say the current month is December. If the report is showing a prior month (for example, September, October, Or November), it will be considered outdated & cannot be used to provide a current update. I can't tell you what's going on in June if I'm looking at a report from March.

While we can request an update on your behalf if your monitoring is active, we cannot initiate updates that would result in unauthorized charges. If your monitoring payment has lapsed, updating the report would trigger a charge, and we will not proceed without your authorization.

Once a client is scheduled to receive a PDF update, my team will then begin Phases 1 & 2. If my team has any issues such as mentioned before, step 1 would be to contact you via email or text. From there we will wait for your confirmation and we will no longer check on that issue for you — it will be 100% YOUR DUTY to notify us once the issue has been handled so that we can resume the process.

Best Practices to Avoid Delays:

To ensure consistent progress, we recommend the following:

- Submit your most recent Proof of Address every month

- Log into your credit monitoring account monthly to confirm:

- The report is updated

- Your login credentials work

- No password reset is required

If these 3 are consistently maintained, everything else falls on us. Don't let it be your fault we couldn't successfully do our job.

⚠️ Hard Truth:

You can't pay for credit repair then:

- Ignore or skim through instructions

- Stop responding

- Ignore emails and text messages

- Keep adding new inquiries, or late payments

- Skip credit building

Then come back 3 months later saying you haven't heard anything, seen any changes, requesting a refund, & proceed to blame my company or the process.

Credit repair works only when WE work.

I'm not a miracle worker, I'm a strategist. You have to do your part as well. Please take your credit seriously—it represents your financial credibility.

☎ Customer Service Number: 312-584-9969

📧 Customer Service Email: [email protected]

Receiving The Same Email & Text From My Support Team

Primary Issues That Delay Results

- • Outdated credit monitoring reports

- • Inaccessible or incorrect credit monitoring login credentials

- • Missing or invalid Proof of Address (POA) documentation

- • Full or inaccessible email inbox (clean up space or buy more storage if needed)

- • Phone settings that block or silence unknown numbers. Please save 312-584-9969 in your contacts to ensure uninterrupted communication.

These are the primary issues that delay results for most clients. By proactively managing the items listed above, you set yourself up for a smooth and successful experience.

Whenever an issue arises—such as a (POA) matter or a login-issue concern—you are tagged within our system. Once tagged, automated messages with clear instructions are sent to you via email & text every 10 business days. You will no longer receive these notifications after a maximum of three reminders are issued, or until the issue is resolved—whichever occurs first.

These reminders are simply a courtesy to ensure you don't forget or nothing is overlooked, as we understand that schedules can be busy.

If you receive an email or text message regarding any of the items above, it is not sent without cause and is not a system error.

In most cases, either: