Credit Education

Master your financial future with comprehensive credit knowledge. Learn the fundamentals of credit repair, score optimization, and financial wellness.

Your Credit Education Hub

Everything you need to know about credit scores, credit reports, negative items, and building financial credibility. Click any topic to expand and learn more.

Why Is Credit So Important?

Statistics

If You Asked 95% Of The People Why They Aren't Where They Want To Be In Life Or Doing What They Want To Do ? Most Will Say "It Takes Money To Make Money & That They DON'T HAVE THE MONEY"

So They THINK THE MONEY IS THE PROBLEM. I Always Tell People If You Don't Have The Money All You Need Is The Credit And You Can Get APPROVED FOR THE MONEY

Did you know it is possible to be approved for $10,000, $30,000, or even $50,000+ in funding before you are able to earn or save that amount through a traditional 9-to-5 income—while still managing everyday expenses and financial obligations?

Even individuals with challenged credit may qualify. In many cases, the time it takes to dispute negative items, rebuild credit, and establish a stronger profile is shorter than the time it would take to save $10,000 through earned income alone.

For many people, saving large sums is difficult due to ongoing living expenses, which often leads to reliance on tax refunds—only to find that those funds are quickly used to catch up on bills rather than create financial growth.

When funding is approved, the key is to allocate it toward opportunities that generate additional income or long-term returns, rather than short-term expenses.

Examples:

- Properties ( 3 Flats, 4 Flats, Fix & Flips, )

- Airbnb's

- Rental Spaces

- Tow Trucks

- Box Trucks

- 18 Wheeler

- ATM's

- Vending Machine

- Car Wash

These are just a few examples, but moral of the story the real goal is to have your PROFITS paying your Bills instead of you WORKING to pay your bills. Or 9/10 you'll be working until the day you die. Because I realized this I haven't worked a a 9-5 since 2021.

Credit repair is important because it:

✓ Lowers interest rates

✓ Increases approvals

✓ Strengthens your profile

✓ Gives you leverage

✓ Saves real money

✓ Saves you time

Think You Have Good Or Decent Credit ? Grade Yourself - How Many Categories Did You Check Off ? Example 1/27, 10/27, 27/27

If You Do Not Know The Answers To These Questions, You May Need To Access All 3 Of Your Full Credit Reports & Scores To Take This Quiz

View My Reports & Scores

https://member.identityiq.com/creditpreferred.aspx?offercode=431297LA

- Credit Age Calculator

- Credit Card Utilization Calculator

- Debt To Income Ratio Calculator

Credit Card Tier Rank

| Tier Type | Card Category | Who they're for | Example | Purpose | Average Credit Limits |

|---|---|---|---|---|---|

| Tradelines / Authorized User | Depends on the owner (Banks Will Know You Are Not The Owner) | Everyone | Doesn't Really Count Towards Your Creditability. At The End Of The Day Banks Want To Know WHAT HAVE YOU DONE? | Can help lower utilization reporting, can help increase credit scores, can help improve credit Age Reporting | Depends On Primary Owner |

| Tier 0 | These Cards Are Not Ranked | Beginners & Rebuilders | Chime, Self Lender, Kikoff, Tomo, Ava, Credit Strong | These Accounts Were Designed To Help Build Payment History But Do Not Count As Real Credit Cards. | Multiple options available. Can vary. |

| Tier 1 | Subprime / Starter Credit Cards | Poor or limited credit (typically 300–579) | Discover it® Secured • Capital One Platinum Secured • OpenSky® Secured Visa | Entry-level access / rebuilding. Secured cards, First-time builder cards | $200 – $1,000 |

| Tier 2 | Near-Prime / Fair Credit Cards | Fair credit (580–669) | Capital One QuicksilverOne • Discover it® Chrome • Credit One Bank Platinum Visa | Transition phase | $1,000 – $3,500 |

| Tier 3 | Prime Credit Cards | Good credit (670–739) | Capital One Quicksilver • Chase Freedom Unlimited® • Navy Federal cashRewards | Strong everyday use (cash back) | $3,500 – $10,000 |

| Tier 4 | Super-Prime / Premium Credit Cards | Excellent credit (740–799) | Chase Sapphire Preferred® • American Express® Gold Card • Navy Federal More Rewards | High rewards & perks | $10,000 – $25,000+ |

| Tier 5 | Ultra-Premium / Charge & Elite Cards | Top-tier profiles (800+, strong income & profile) | American Express® Platinum Card • Chase Sapphire Reserve® • American Express® Centurion | Lifestyle, leverage, and prestige | $25,000 – $100,000+ (or No Preset Limit) |

Credit Profile Scorecard - Weak vs Strong

| Category | Weak Profile | Strong Profile | Magic Question | Score Board |

|---|---|---|---|---|

| 1. Credit Score | 300 - 679 (680-719 Is Mid) | 720 Or Higher | Is Your Credit Score A 720 Or Better? | Give Yourself One Point If Yes. |

| 2. Total Open Accounts | 1-9 Accounts and or recently | 10 Or More. | Do You Have 10 Or More Open Positive Accounts? | Give Yourself One Point If Yes. |

| 3. Closed Accounts | Paid but with late payments, some paid collections | Everything paid off 100% good standing (NO LATES) | Are All Of Your Closed Accounts Paid With 0 Late Payments? Paid Collections Don't Count | Give Yourself One Point If Yes. |

| 4. Credit History / Credit Age (15% Of Your Score) | 1 month – 4 years | 5+ years of established credit | Is Your Credit Age At Least 5 Years? | Give Yourself One Point If Yes. |

| 5. Payment History (35% of Your Score) | 20%–80% on-time payments, Any 30/60/90/120-day late payments, Missed payments on Credit Cards, installment loans | 100% on-time payments every month, No late payments at all (or none showing) | Do You Have 100% Payment History? (This Also Includes Closed Accounts You Have Paid Off) | Give Yourself One Point If Yes. |

| 6. Credit Card Type | Authorized User | Primary Owner | Do You Have At Least 3-5 Real Credit Cards? | Give Yourself One Point If Yes. |

| 7. Credit Card Tier | 0-2 Tier | 3-5 Tier | Based Off The Information Above, What Tier Do Your Credit Cards Rank? Are Any 4 & 5 Tier Cards? | Give Yourself One Point If Yes. |

| 8. Credit Card History | Opened 6-12 Months | (2-4 Years = Mid) 5+ Years = Good | Do you have at least 1 credit card with a 5 year payment history? | Give Yourself One Point If Yes. |

| 9. Individual Credit Card Limits | $200 – $4,999 | $5,000 Or Higher | Do You Have 3 Credit Cards With A Credit Limit Of $5,000 Or More? | Give Yourself One Point If Yes. |

| 10. Total Credit Limit | $14,000 Or Below | $15,000–$50,000+ total available credit | Do You Have $15,000–$50,000+ in Total Available Credit? | Give Yourself One Point If Yes |

| 11. Credit Card Utilization (30% Of Your Score) | Above 30% or maxed out | 1%–10% utilization (never above 30%) | Is Your Credit Card Utilization Under 10%? | Give Yourself One Point If Yes. |

| 12-14. Credit Mix (Can Score 1, 2, Or 3 points) | Only 1-3 accounts (usually cards only) | Credit Cards + auto + personal/installment & Open Credit | Do You Have Revolving Credit Cards, Installment Loans, And Open Credit (Utility Bills Or Rent) Reporting To Your Credit? | If You Have Revolving Accounts Add 1 Point. If You Have Installment Accounts Add 1 Point. If You Have Open Credit Add 1 Point. |

| 15-16. Installment Accounts (Can Score 1 Or 2 Points) | Only small installment loans ($500 – $3,000) | Mid =$5,000-$9,000. High-value installment loans ($10,000 – $50,000+) | Do you have any installment loans $10,000+ paid off or 100% payment history | If paid off add 1 point. If open but 100% payment history add 1 point. |

| 17. Installment Account History | Recently opened installment loans | Installment loans aged 12–36+ months | Do you have any installment loans with payment history 12-36+ months old? | Give Yourself One Point If Yes |

| 18. Hard Inquiries (10% Of Your Score) | 3-10+ per bureau | 2 or fewer per bureau | Do You Have 2 Or Less Inquiries Per Credit Bureau? | Give Yourself One Point If Yes. |

| 19. Hard Inquiry Type (Good Vs Bad Inquiries) | Not attached to open accounts (most likely got denied but still has inquiry reporting) | Attached to open accounts (Applied for something and actually got approved) | Do you have any inquiries that ARE NOT attached to open accounts? | If the answer is NO. ADD 1 POINT. |

| 20. Hard Inquiry History | 5 Months Or Less | 6 Months Old Older | Are Your Inquiries At Least 6 Months Old? | Add 1 Point If Yes. |

| 21. Debt To Income Ratio (DTI) | 44%–50%+ | 0%–35% | Is Your DTI 0-35%? | Give Yourself One Point If Yes. |

| 22-23 LLC (can score 1 or 2 points) | Less Than 2 Years Old, Not Set Up Properly, Or No LLC | 2 Or More Years Old, Set Up Properly | Do You Have A LLC & Has It Been Established For At Least 2 Years? | If You Have A LLC Add 1 Point. If you had it for 2 years add another point. |

| 24. Tax Liens | Federal or State Tax Liens present | No tax liens reported | Do you have any tax liens reporting on your credit report? | If the answer is no add one point. |

| 25. Derogatory Accounts (Derogatory = Negative) | 1+ Negative Account | Clean credit report (0 derogatory accounts) | Do You Have Any Negative Accounts On Your Credit Report? Collections, Repos, Evictions, Charge Offs, Student Loans, | If Yes, Subtract All Points. You Have Been Disqualified And Do Not Have Good Credit. If The Answer Is No Add One Point |

| 26. Bankruptcies | Open Bankruptcy, Dismissed, Or Discharged (Chapter 7, 11, or 13) | No bankruptcy on file | Do you have a bankruptcy reporting on file? | If The Answer Is No Add One Point. If Yes Subtract All Points. A Bankruptcy Is The Worst Thing You Can Have On Your Credit Report |

| 27. Funding Outcome | Denials or terrible loan terms | Lower interest & higher approval limits | If you apply for a personal or business loan and can't get a minimum 50K. You do not have good credit. You may have decent credit but not good credit. | If you have been approved for over 50k within the last 6 months add 1 point. |

| Approval Results | Requires cosigner, proof of income, collateral, or high interest rates etc | No cosigner, proof of income, or collateral needed. Also low interest rates. | Based off of your recent experience when applying for things using credit you should be able to tell if your report is Bad, Decent, Good, Or Great. | No need to add points here |

Hard Truth: What's Your Total Out Of 27? I Scored 23/27

- Because I didn't care about my credit until a few years ago even im still building payment history. No one can run from this. Tradelines won't save you.

- Because I am financing so many things at once my DTI is now higher than 35%. As I slow down and keep paying my bills on time it'll go back down.

- Although I have 3 installments over 10K, (10K, 45K & 50K) Neither has been fully paid off but all 3 does have 100% payment history so I only got 1 point for that.

- I was approved for 50K within the last 6 months so I gained a point for that but that also means I also have a hard inquiry that is recent so I lost a point for that.

For those who believe their credit situation isn't that bad, I hope this provides helpful clarity and insight. There's no reason for embarrassment—awareness is the first step toward improvement. Now that you know what areas need attention, you can take the right steps forward. If you need assistance with any of these subjects, don't hesitate to book a consultation. I'm here to help you restore and strengthen your credit profile.

Why Is Credit Repair So Important?

1️⃣ Credit Affects Things People Don't Expect

Credit isn't just loans:

- Renting an apartment

- Cell phone deposits

- Utilities (gas, electric, internet)

- Insurance rates

- Some jobs & promotions

Bad credit = more deposits, more scrutiny, fewer options.

2️⃣ Credit Repair Removes What's Holding You Back

Credit repair does NOT erase debt — it removes:

- Inaccurate

- Outdated

- Unverifiable

- Improperly reported items

That's important because lenders don't care why something happened — only what's showing right now.

3️⃣ A High Score ≠ Strong Credit

You can have a 720+ score and still get denied.

Lenders look at:

- Payment history

- Utilization

- Credit age

- Account mix

- Profile strength

Credit repair cleans the report so building actually works

4️⃣ Credit Repair Saves Time

Without cleaning the report first:

- New credit gets denied

- Utilization fixes don't move scores

- Hard inquiries hurt more

- Growth stalls

Repair first → then build → then apply.

That Said Every Single Person Wants Good Credit & eventually finds out the hard way that they actually NEED GOOD CREDIT. It kills me that people don't realize a few negative items are the main things holding them back from living the lifestyles they deserve. Whenever your credit is holding you back from something you have 5 Options.

1️⃣ Pay Off Of All Of Your Debt.

If you have thousands of dollars available to pay everything off then be my guest. But understand that Paying collections does not Remove the negative item from your credit report. It will just update the payment status to PAID COLLECTION. And that still does not help your credibility. And most importantly it doesn't wipe away the late payments either.

2️⃣ Stay In Debt For 7-10 Years & Wait For Everything To Fall Off ( Holding Yourself Back )

This option is Not as Simple as it sounds, and honestly isn't smart either. Mainly because of how late payments report. YOU'LL BE WAITING FOREVER LIKE YOU BEEN HAVE.

| Account Type | How Long It Stays On Your Credit Report |

|---|---|

| Late Payments | That's 7 Years ( PER LATE PAYMENT ) So if you got a late payment on your car note in 2023. It won't fall off until 2030. But what if you got another late payment in 2026? Now you have to wait until 2033. So when you have multiple accounts with multiple late payments you'll be waiting forever and hopefully you don't add any new late payments. |

| Inquiries | 2 Years |

| Collection | 7 Years |

| Charge-Offs | 7 Years |

| Repossession | 7 Years |

| Bankruptcy | 7-10 Years |

| Evictions | 7 Years |

| Medical Bills | 7 Years |

| Student Loans | Open Accounts can last a lifetime. Closed accounts can last 7 years. Most of the time Lenders never close student loans because there is no statue of limitation on the debt so if you don't get them removed, they can still hold you back 10–25+ years down the line. |

3️⃣ Do It Yourself ( Free But Understand This Takes Time. )

- You Might Research The Right Things. You Might Research The Wrong Things.

- If You Do Research The Right Things You Might Understand It Or You Might Not.

- If You Do Understand It You Might Do It Right Or You Might Do It Wrong.

Bottom Line You Keep Going Until You Get It Right And That Will Take However Long It Needs To Take. Question Is Do You Have That Time To Wait ? Probably Not but That's Your Decision.

4️⃣ Pay Someone To Fix It

Best option if you can find someone like me who's efficient, very informative, trustworthy, has real results, real testimonials, and a proven track record of consistency.

5️⃣ Find someone who will accept you with your situation ( THIS IS THE TRAP ) this is also why bankruptcy wouldn't be a smart option.

I Guarantee if a company ever told you, WE ACCEPT BAD CREDIT. They are legally about to Rob you blind. And I will prove it. Take a look at Interest Rates where I explain to you how much life is costing you with Having Good Credit Vs Bad Credit.

Why Bad Credit Cost More Than Credit Repair ?

Did You Know That Having Bad Credit Is Costing You WAY MORE Than Credit Repair Ever Will?

- If You're Worried About The Cost Of Getting Started...

- You Should See The Cost Of Staying Exactly Where You Are…

- Credit repair is important because your credit controls the COST OF YOUR LIFE — not just approvals.

Credit Repair Is an Investment, Not a Bill. People hesitate or complain over paying $600–$2,000, then:

- Donate their money regularly to every single business everyday

- Overpay $8k–$30k on a car

- Pay $100k–$300K+ more on a mortgage

- Get stuck in high-interest cycles

Choosing To Stay With Bad Credit Is Costing You THOUSANDS OF DOLLARS MORE & I Will Prove It.

Incase it hasn't dawned on you by now I want to be very REALISTIC. I can charge you $5,000 to fix your credit and you will still come out of more money trying to reach your goals without just paying me the $5K first. Don't worry my prices are nowhere near $5K, but for this example let's say that was how much I charged for my services.

Most people would hear that price and think to themselves "he's crazy I'm not paying that" and they will keep searching until they find a company who "ACCEPTS BAD CREDIT". Or they will consider filing for Bankruptcy.

The Bankruptcy Trap Most People Don't See Coming

Most people have a major misconception about bankruptcy. They believe that once they file, it's a complete "fresh start." But in reality, it often creates a much more expensive problem long-term — one that most people don't realize until years later.

Let's start with a common scenario.

Many people file bankruptcy over what feels like a large amount of debt — often something like a repossessed vehicle or an auto loan balance of $8,000 to $10,000. At the moment, filing can seem like the easiest solution: the debt is discharged, the account is no longer collectible, you no longer have a car note, and it feels like the problem is gone.

But what most people fail to consider is THE COST OF BANKRUPTCY OVER TIME. They're going to spend 10 times whatever the price was of the original debt they were avoiding.

Once bankruptcy is on your credit report, it remains there for 7–10 years. During that time, LENDERS VIEW YOU AS HIGH RISK. That means 10/10 whatever you apply for within that timeframe will automatically cause… higher interest rates, fewer approvals, and stricter terms across the board.

For example, after bankruptcy, many people still need transportation — so they go finance another vehicle. Even if the car costs only $20,000, they may be approved at a 25–30% interest rate, often with a longer loan term (60–72 months) just to keep the monthly payment affordable.

If you get charged that much, especially if you're getting about a six-year term — which most people do because the car note's already high, so in order to get the cheaper car note they get a longer term, not realizing a longer time means more interest — so with a 25% interest rate on a $20,000 car, you're already paying an extra $5,000 a year. That's already $30,000 in interest after the 6-year term is done.

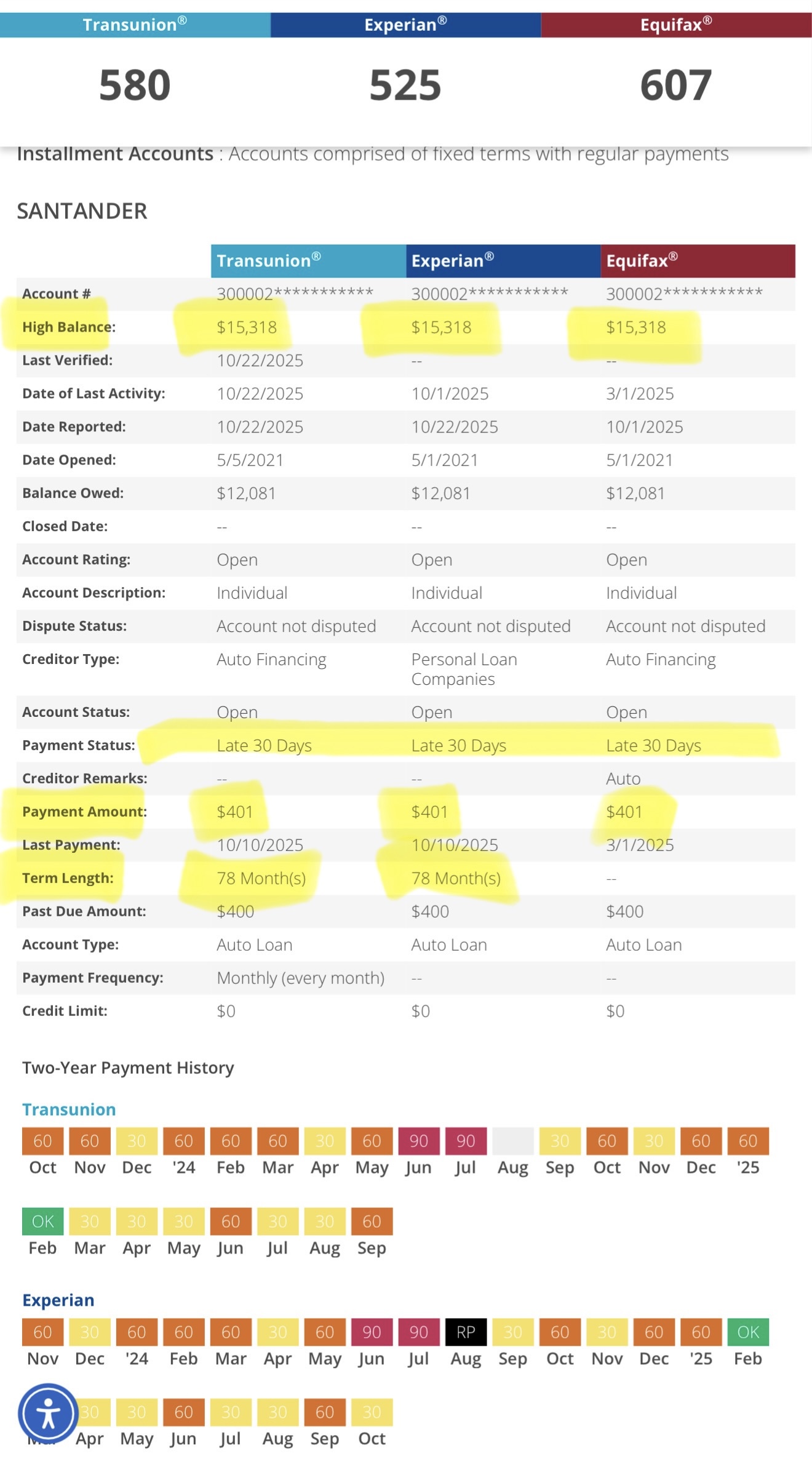

Take This Person For Example:

- The total price of this car was only $15,318

- 78-month term (6 years and 5 months)

- Car note is $401/Month

- $401 X 78 = $31,278.00 Total

- $31,278 - $15,318 = $15,960.00 EXTRA

- They are paying more in interest than for the car itself

- That's 104.20% Interest (Not including down payment, which was likely 10K+ due to bankruptcy)

Hopefully this car doesn't give you any issues because in most cases if the car is in bad shape, it will most likely be in and out the shop costing you thousands. And what do most people do? They figure why pay a car note if I don't have the car? When in reality the car problems has nothing to do with the bank that loaned you the money for the car. YOU STILL OWE THEM. And now your credit is even worse and you're back to square one.

Or let's say the car is in good shape. It's still not worth it because by the time you're ready to trade it in, it won't be worth the amount you owe. So if you still owe $12,000 by the time you trade it in, that $12,000 debt is considered NEGATIVE EQUITY — which means it will get added to the new loan.

So let's say you trade it in for another $25,000 car. You'll be paying $37,000 for a $25,000 car — and that's not even including the extra 25% interest you're about to get charged because you still have a bankruptcy on your report. Once again digging your grave even bigger.

Now a car is just one thing. And if that's how much extra you'll pay for a $20,000 car — how much extra do you think you'll pay to get a house, a building, or a business loan? All of those things cost way more than a car. Which means you're going to be spending so much money in interest every year that you could have already paid the $10,000 or whatever it was for the original debt. But life doesn't stop for you. So for the next 10 years, every approval costs more. Every loan carries heavier interest. Every financial move becomes more expensive.

Take this house as an example:

- Total cost: $112,818

- $1,117/Month, 360-month term (30 Years)

- $1,117 X 360 = $402,120.00

- $402,120 - $112,818 = $289,302.00 EXTRA IN INTEREST

- That's 256% IN INTEREST

- Could have bought 3 Houses For The Same Exact Price & Still Had Over $63,666 Left

- My point is — one way or another, you will pay the money.

SO YOU MEAN TO TELL ME YOU REALLY PREFER TO DONATE ALL THAT MONEY RATHER THAN INVEST IN YOURSELF?

This is one of the main reasons people can't afford to or are scared to invest in themselves because they don't know what they're doing — they're JUST GIVING IT OUT. By choosing to stay with bad credit you are choosing to DONATE YOUR HARD EARNED MONEY.

When you add it all up, many people who filed bankruptcy to avoid paying $8,000–$10,000 end up spending well over six figures in extra interest over the next decade — simply because their credit profile was damaged. That's the part no one explains.

Bankruptcy doesn't erase debt — it reshapes your financial future, and usually not in your favor. In many cases, paying or strategically resolving a smaller debt upfront is far cheaper than carrying the long-term cost of bankruptcy. That's why bankruptcy should always be a last resort, not a quick fix.

Why Good Credit Allows You To Save Over $10,000+

Here Are A Few More Reasons Why Bad Credit Cost More Than Credit Repair Even If You Didn't File For Bankruptcy.

Watch The Video Passcode: 0wPk$mMg

Understand The Difference Between Your Credit SCORE Vs Credit REPORT Vs Credit PROFILE

Fun Facts:

- Your Credit Score, Credit Report, & Credit Profile Are 3 Completely Different Things.

- Your #CREDIT Is NOT Your Credit SCORE. Your Credit Is Your Credibility Aka Your Reputation With Banks & Lenders

- When You Have Negative Items & Late Payments On Your Report YOU HAVE NO CREDIBILITY

- Your Credit Score DOES NOT Get You Approved For Anything

- Just Because You Have A Good Credit Score DOES NOT MEAN You Have GOOD CREDIT

- Someone With A 650 Credit Score Can Get Approved Over Someone With A 750 Credit Score due to the report and profile

- Your Credit Report & Credit Profile Is Far More Important Than Your Credit Score.

- You Can Have A 750 Credit Score And STILL NEED A CO-SIGNER

- Credit Is Just Like A Job… You Need The Experience To Get The Job, But You Need The Job To Get The Experience. In This Case You Need The History To Get The Credit & You Need The Credit To Get The History.

- Having No Credit History Is Almost The Same As Having Bad Credit. Either Way You Have NO CREDIBILITY

What Credit Repair Actually Does

Credit Repair DOES NOT DELETE THE DEBT ‼️

No You DO NOT Owe The DEBT COLLECTOR. But You DO OWE The Original Creditor.

The Purpose Of Credit Repair Is To Hide The Negative Items From Your Report So That They Don't Hold You Back For 7–10 Years Waiting On Things To Fall Off Of Your Report. And Also, You Don't Have To Pay High Interest For 7–10 Years, All Because You Got A Collection 3 Years Ago. So Now You Can Get Approved For Things. However, It DOES NOT MEAN THE DEBT IS DELETED.

So Why Not Just Pay It?

- 9/10 If You Have A Collection Your Information Has Been Passed On To A 3rd Party Debt Collector That You NEVER Did Business With So Therefore You DO NOT OWE THEM ‼️

- Every State Has A Statue Limitation On When A Creditor Can Collect On A Debt 💸 A lot Of Times Consumers Don't Realize That They Almost Are Scott Free Of Paying A Debt But When They Pay A Small Payment THE CLOCK STARTS OVER

- If You Pay Them It Will Be Harder To Get Removed Because Why Would Anyone Pay A Debt That Doesn't Belong To Them. So You Look Guilty

- Paying Them DOES NOT REMOVE IT FROM YOUR CREDIT REPORT

- If You Pay Them In Full It Will Show Up As A PAID COLLECTION

- If You Fall For That Letter Saying Pay 30-40% Off It Will Say SETTLED FOR LESS THAN FULL BALANCE

So When It Comes To Your Credit REPORT. Regardless Of If You Pay Some Or All Of Your Collections. It DOES NOT HELP YOU AT ALL.

The Smart Approach:

- If You're Ever Behind On an OPEN ACCOUNT Yes it is safe to get on a payment plan etc to pay it down

- But if that account has ALREADY BEEN CLOSED & SENT TO COLLECTIONS It's better to get it removed FIRST & Then Settle The Debt

- Because If You Settle First, It Will Still Be On Your Credit Report And That Doesn't Help You

Credit Repair Is Still Important. Look at it as if you just got your RECORD EXPUNGED. Just because you get your record expunged doesn't mean you didn't do the crime and do the time. But when you apply for jobs THEY DON'T SEE THE FELONIES ETC…

So in this case, just because you get something REMOVED FROM YOUR REPORT doesn't mean you don't have late payments or collections, but when you're applying for things THEY DON'T SEE THEM… But yes, you still owe the debt WITH THE ORIGINAL CREDITOR.

Example: Let's say I received an auto loan from CHASE BANK. And I fall behind on payments and the car gets repossessed. If I were to try to finance another car, almost everyone will deny me once they see that or any other collections on my report.

But once I get it REMOVED FROM MY REPORT, it's a million companies that'll give me an auto loan. But if I want to get another auto loan from CHASE BANK, 9/10 I may have to settle that debt with them because THEY HAVEN'T FORGOT ABOUT ME. But everyone else won't be able to see that I owe Chase, so they'll be willing to do business with me.

Credit SCORE

Your Credit Score = Your RESUME

( What Makes You Qualify To Apply )

A Good Resume Does Not Mean You Automatically Got The Job. The Resume Is Only Enough For The Employer To CONSIDER YOU.

For Example: A Trucking Company Is Hiring On The Flyer It Says " MUST HAVE VALID CDL " I Can't Even APPLY Without Having A CDL. But Just Because I Have A CDL That Doesn't Mean I Will Get The Job. I'll Still Have To Complete A Interview & Background Check.

Just Like A Resume Your Credit Score Makes You QUALIFIED TO APPLY. ( Example: You Must Have A 650 Credit Score To Apply For This Apartment )

- What If 12 Other People Also Have A 650? Why Should They Choose You ?

- Just Because You Might Have A 650 Credit Score Doesn't Mean You Will Be Approved.

- You Just QUALIFY TO APPLY.

Credit Card Application

Credit Card Application = The INTERVIEW

When applying for credit, several factors influence approval, including your income, existing debt, employment history, and overall financial profile. However, what many people don't realize is that even with a 700+ credit score and no collections, your application can still be negatively impacted by inaccurate or inconsistent personal information.

Credit bureaus rely heavily on personal identifiers to verify identity. If your name or details appear differently across reports—for example, Cordell D. Collins on one bureau, Cordell Collins on another, and Cordell Collins Jr. on a third—those discrepancies can cause verification issues. On paper, these variations can appear as separate individuals. The last thing you want to do is be held responsible for someone's else mistakes.

Ultimately what you want to see on your credit report is ONE NAME, ONE DOB, & ONE EMPLOYER. All 3 of them should MATCH TO THE T.

Many consumers have multiple name variations and outdated addresses listed on their credit reports. This can trigger red flags during the application process, leading lenders to question identity verification, suspect potential fraud, or confuse you with another individual who shares the same name. While this is not a common reason for denial, it does happen—and I've seen it occur.

To avoid surprises: The best way to prevent and correct this issue while undergoing credit repair is to ensure that the address on your government-issued ID matches your current residence.

Consistency and accuracy play a critical role in protecting your credit profile and improving approval outcomes.

Credit REPORT

Credit Report = The BACKGROUND CHECK

( This Is What Gets You Approved Or Denied )

Derogatory Marks Are Like Felonies. You Can Have The Best Resume In The World Along With All The Work Experience. The Chances Of You Becoming Manager At Any Establishment With Armed Robbery On Your Record Is Slim. A lot of times people often downplay their credit reports.

Don't ever think just because you only have a "few negative items" or only owe small debts that your credit report is " NOT THAT BAD " In Most Cases 1 Collection can and will get you denied regardless of the amount owed.

Smaller collections are actually worse. A $10,000 collection makes sense but when you have small collections you just make yourself look very irresponsible. If You couldn't handle a $300 credit card, Why should anyone trust you with a $30,000 auto loan?

You Can Have A 750 Credit Score 1 Collection Can Get You Denied. Having A Bankruptcy On Your Report Is Like Committing Murder. It's The Absolute Worst Thing You Can Have On Your Credit Report.

Good Credit Report Vs Bad Credit Report

Good Credit Report - This Is What You Want To See

- This Person Has 0 Late Payments

- 0 Collections

- 0 Public Records ( Which would also be considered a Derogatory account )

- Less Than 2 Inquiries Per Credit Bureau

- If Your Report Doesn't Look Like This YOU NEED CREDIT REPAIR.

Bad Credit Report - This Is What You Don't Want To See

- This Person Has 2 Delinquent Accounts ( meaning accounts with late payments)

- They Also Have A Total Of 12 Derogatory Accounts ( Meaning Accounts In Negative Standing Such As Repos, Charge-offs, Evictions Etc ) 2 Collections

- They Also Have 3 Public Records ( usually bankruptcies )

That's A Total Of 19 Negative Accounts. That's Not Including The 22 Inquiries.

SideNote: Your Report Is Always Worse On Paper Than Real Life. You Might Have 1 Collection With T-Mobile But If That Collection Is Reporting On Transunion, Experian, & Equifax, On Paper That's 3 Collections. In Conclusion This Report Is HORRIBLE. Would You Loan Someone Money If You Knew For A Fact They Owed 19 People?

Credit Profile

When Applying For Things Like Auto Loans, Personal Loans, Business Loans, & Mortgage Loans. Without A Strong Profile You May Be Asked To…

- Provide a co-signer

- Show proof of income (pay stubs, tax returns, bank statements)

- Put up collateral (vehicle, cash, assets, or liens)

- Accept a higher interest rate or unfavorable terms

- Make a larger down payment

- Accept a lower approval amount than requested

- Pay origination, funding, or risk-based fees

- Open additional accounts with the lender (checking/savings)

- Agree to shorter loan terms (higher monthly payments)

- Provide business financials (P&L, balance sheet, EIN history)

- Face manual underwriting instead of instant approval

- Receive a conditional approval that can be revoked

Take This Story As A Great Example. She Thought Her Credit Score Was Her Credit. 10/10 She Had A Weak Profile & That's Why She Still Needed A Co-signer.

Hard Truth:

Having "good credit" means more than a high score. If you are not in a position to confidently request six-figure funding from a financial institution, your credit profile may not be as strong as you believe.

For the statement "I have good credit" to be accurate, four key elements must be in place:

- Good Credit Score

- Clean & Accurate Credit Report

- Strong Credit Profile

- LLC SET UP PROPERLY

Why Do You Need All Four? Because All 4 Combined Is WHAT MAKES YOU CREDIBLE. And Remember YOUR CREDIT IS YOUR CREDIBILITY.

- A Good Credit Score Doesn't Mean You're Approved But Without A Good Credit Score You Most Likely Won't Qualify To Apply For Most Things.

- You Can Have A Good Credit Score & Still Fail The Application For Putting Wrong Information On A Application, Or Not Having An Accurate Credit Report

- You Can Have A Good Credit Score, Clean Credit & Accurate Credit Report. But Still Have A WEAK PROFILE.

Even with a good credit score, clean credit report, and strong profile. Business funding can still be denied if the LLC is not set up correctly. Entity structure, compliance, and financial alignment play a critical role in lender approval. Your business is what gives you access 150K or more. Not to mention all of the tax benefits as a business owner.

However, if your personal credit is not strong, it is recommended that you address and improve it first—unless you can provide verifiable business bank statements and tax returns demonstrating consistent monthly profits of at least $10,000.

This is a separate—but equally important—conversation. If you would like to determine whether your LLC is properly established or need assistance with setup and compliance, you are encouraged to schedule a consultation.

What Makes Up Your Credit Score?

Please Understand That Credit Repair DOES NOT Boost Your Score. The Only Person That Can Increase Your Credit Score Is YOU.

I Cannot Make Your Scores Go Up Or Down. So If You Want A Higher Credit Score You First Need To Know What Makes Up Your Credit Score? These Are Called #The5Factors

| Factor | Explanation |

|---|---|

| Payment History 35% | Nobody pays your bills BUT YOU so if you get a late payment the only person should be to blame IS YOU. I Do Not Pay Any Of My Clients Bills |

| Credit Card Utilization 30% | Nobody should be using any of your credit cards BUT YOU so if your credit card balances are over 30% or maxed out and your score drops. Once again that is not my fault. I have 0 access to any of my clients credit cards |

| Credit Age/History 15% | This is the one that gets everyone including myself. The banks like to see at least 5 years worth of good credit history. But unfortunately people don't care about their credit until it stops them from getting approved for things. So if you waited last minute to prioritize your credit and you have no credit history or short history…. THAT IS NOT MY FAULT. |

| Inquiries 10% | Every time you apply for something that is a HARD PULL. You WILL RECEIVE A INQUIRY. And every time you receive an inquiry whether you are Approved Or Denied YOUR SCORE WILL DROP. I don't apply for anything in anyone's name So if you have too many inquiries or receive new inquiries once again… NOT MY FAULT |

| Credit Mix 10% | So incase you didn't know there are different types of credit. I break down these different types of credit in my zoom recordings that should be in your email. But long story short. If you have no positive accounts on your profile then you have no credit mix. And since I have not and will not apply for anything in anyone's name if my client's names. Once again… NOT MY FAULT. |

| Reality | Credit score changes are based on account activity and lender reporting. I do not make payments, use your credit cards, or apply for credit on your behalf. |

Hard Truth:

There's absolutely NO WAY to have good credit without having positive reporting accounts. You can get everything deleted off of your credit report and STILL have bad credit due to failure of REBUILDING your credit profile. Rebuilding means you have positive reporting accounts that report to the credit bureaus monthly.

- 2 or more Active Credit Cards

- 1 or more Active short term loan (Self lender, credit builder loan, personal loan etc)

- 1 or more Active long term loan (Car, mortgage, Bank loan etc)

If you cannot go through your report and find any of the following then you NEED to visit my ACTIVE CLIENT TAB & CLICK ON THE "TO DO LIST"

Credit repair works only when WE work.

I'm not a miracle worker, I'm a strategist. You have to do your part as well. Please take your credit seriously—it represents your financial credibility.

Different Types Of Credit (Credit Mix + Credit History = Credit Portfolio)

Revolving Credit - Credit Cards 💳

Revolving Accounts that would generally have a different amount due each month depending on the current balance. The full balance is not required to be paid in order to keep the account in good standing. Interest is accumulated each month that a balance is carried over into the following month.

Installment Credit

- Auto Loan

- Mortgage Loan

- Student Loans

- Personal Loans

- Secured Loans

Open Credit

- Utilities

- Phone Bill

- Rent

Primary Account vs Authorized User

| Primary Account | Authorized User |

|---|---|

| You are the owner of the account. You have full responsibility of everything that comes with the account. | A primary account holder has the option to add an authorized user to their account. They can use the card but the responsibility and owner of the account is the primary account owner. |

Different Types Of Revolving Accounts

Credit Cards Issued By Banks Or Credit Unions

• Always backed by familiar logos such as Visa, Mastercard, American Express, or Discover.

• Generally A 680+ Would Get You Approved

• Multiple options available for customers who have no credit to established credit.

Credit Cards Issued By Retail Stores

• Store credit cards are great for saving money on purchases at your favorite stores.

• Generally, a minimum of 640+ credit score will get you approved for a retail store credit card.

Examples: Amazon Prime Store Card, Macy's Credit Card, Target RedCard, Walmart Rewards Mastercard

Credit Cards Issued By Oil & Gas Companies

• These cards are great for saving money at the gas pump.

Examples: ExxonMobil Smart Card, BP Credit Card, Shell Fuel Rewards Card, Techron Advantage Card (Texaco & Chevron)

Installment Accounts

• Accounts with a fixed monthly payment for a fixed period of time.

• Interest could be fixed or variable.

Examples: Auto Loans, Mortgage Loans, Student Loans, Credit Builder Loans, Personal Loans

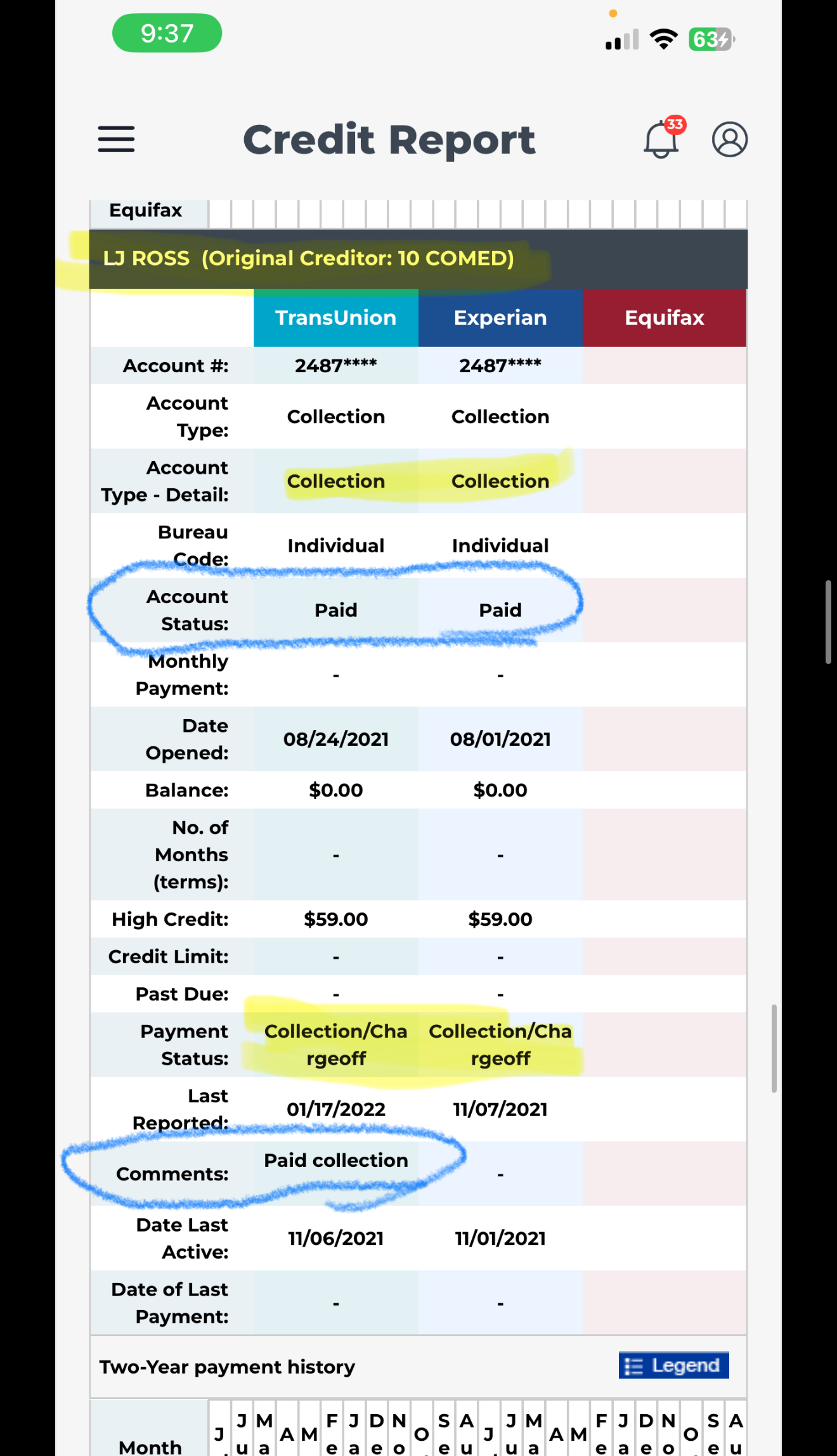

Would It Be Better To Just Pay My Collections Off ?

9/10 If You Have A Collection Your Information Has Been Passed On To A 3rd Party Debt Collector That You NEVER Did Business With So Therefore You DO NOT OWE THEM !!

Why Pay A Company You Don't Owe ? Even If It Were The Original Creditor Paying Them DOES NOT REMOVE IT FROM YOUR CREDIT REPORT.

- If You Fall For That Letter Saying Pay 30-40% Off And We Will Say SETTLE This For You. It Will Still Be On Your Credit Report As A Paid Collection, SETTLED FOR LESS THAN FULL BALANCE Which Is Still A Negative Account And That DOES NOT Help You.

- Not Only Were You Already Behind 120-180 Days But When You Finally Decided To Pay Them, They Didn't Even Get All Of Their Money ? It Doesn't Look Good

- If You Pay Them IN FULL It Will Still Show Up As A PAID COLLECTION Which Is Still A Negative Account And That DOES NOT Help You.

EXAMPLE: Let's Say I Go To Jail For Stealing Money Out Of a Walmart's Register. So I Have Did My Time For It. When I Get Out Of Jail, I Apply To Work For Chase Bank Do You Think They Will Hire Me ? I Can't Say " BUT I WENT TO JAIL FOR IT " Because It Should Never Happened To Begin With. No Difference Here. So You're Better Off Getting It Removed. Paying A Collection Doesn't Help Your Credibility. Would You Continuously Lend Money To Someone Who Never Pays Back On Time ?

The Smart Approach:

Nothing Wrong With Settling A Debt. It's Just WHEN YOU SETTLE IT. Please Allow Me To Explain.

- If You're Ever Behind On an OPEN ACCOUNT Yes it is safe to get on a payment plan etc to pay it down

- But if that account has ALREADY BEEN CLOSED & SENT TO COLLECTIONS It's better to get it removed FIRST & Then Settle The Debt

Fun Fact:

Every state Has a Statute of limitation on when they can collect a debt. Each state sets different time limits for different categories of debt. The clock doesn't run the same for everything.

Common Debt Categories That Matter

Illinois Example (Very Important)

How Statutes of Limitation Actually Work

Each category can have a different statute — even within the same state.

What Starts the Clock?

The statute of limitation clock usually starts at:

- Date of first delinquency (DOFD)

- OR date of last payment (varies by state & debt type)

Any of the following can RESET the clock:

- Making a payment

- Acknowledging the debt in writing

- Entering a payment agreement

A lot Of Times consumers don't realize that they almost are scott free of paying a debt, and when creditors & debt collectors convince you to get on a payment plan and you make that first small payment, THE CLOCK STARTS OVER. This is why clients should NEVER casually agree to pay old debt without advice. If You Pay Them It Will Be Harder To Get Removed Because Why Would Anyone Pay A Debt That Doesn't Belong To Them. So You Look Guilty.

What Is A Collection Account?

A collection account is a negative credit item that appears when a bill goes unpaid for a long period and the original creditor sends or sells the debt to a collection agency.

Common types of collection accounts

- Credit cards

- Medical bills

- Utility bills

- Phone/cable/internet bills

- Auto loan deficiencies

- Apartment or rental balances

Why collections are serious

- They can drop your score 50–150+ points

- They stay on your credit report for 7 years from the first missed payment

They make it harder to get:

- Credit cards

- Auto loans

- Mortgages

- Apartments

Paid vs. unpaid collections

- Unpaid collections obviously will still hurt your score, BUT Paying a collection does NOT guarantee removal

- Paid collection → Settled for less than full balance, A collection is still a collection at the end of the day and needs to be removed from your profile. If you get out of jail for robbery even though you did your time will jobs still look at you sideways?

What Are Student Loans?

A student loan is borrowed money used to pay for education that you must repay—with interest—after (and sometimes during) school.

🏦 The 2 Main Types of Student Loans

1. Federal Student Loans

Issued by the U.S. government

Pros:

- Lower interest rates

- Flexible repayment plans

- Deferment & forbearance options

- Possible loan forgiveness

Cons:

- Still hard to discharge in bankruptcy

Common federal loans: Direct Subsidized Loans, Direct Unsubsidized Loans, PLUS Loans (parents or grad students)

2. Private Student Loans

Issued by banks, credit unions, or lenders

Pros:

- Can cover gaps federal loans don't

- Faster approval sometimes

Cons:

- Higher interest rates

- Credit-based approval

- Fewer protections

- Almost never forgiven

⏳ When Do You Start Paying Them Back?

- Usually 6 months after leaving school (grace period)

- Interest may build while you're still in school

- Payments can last 10–25+ years if not managed properly

📉 How Student Loans Affect Credit

Student loans:

- Appear as installment loans

- Can help credit if paid on time

Can destroy credit if:

- Late

- Defaulted

- Sent to collections

What Is An Eviction?

An eviction is a legal process where a landlord forces a tenant to move out of a rental property—usually because the tenant violated the lease or failed to pay rent.

🏠 Common Reasons Evictions Happen

- Non-payment of rent (most common)

- Repeated late payments

- Violating lease terms (unauthorized occupants, pets, damage)

- Illegal activity

- Staying after the lease ends (holdover tenant)

⚖️ How the Eviction Process Works (Simple Version)

- Notice is given (Pay rent, fix the issue, or leave by a certain date)

- Court filing If the issue isn't resolved, the landlord files an eviction case

- Court judgment A judge decides whether the tenant must leave

- Physical removal (if necessary) Law enforcement may remove the tenant if they don't leave voluntarily

⚠️ You're not officially evicted until there's a court judgment—not just a notice or threat.

📄 Eviction vs Eviction Filing (Important Difference)

- Eviction notice → ⚠️ Warning (not on your record)

- Eviction filing → ⚠️ Court case (can show up in tenant screenings)

- Eviction judgment → ❌ The real damage (harder to remove)

Even dismissed cases can still hurt rental approvals.

⏳ How Long an Eviction Stays on Record

- Tenant screening reports: 7 years

- Court records: varies by state

- Collections tied to eviction: 7 years

That's why evictions hurt housing approvals more than credit cards do.

What Are Medical Bills?

A medical bill is a charge you receive for healthcare services that were provided to you—but not fully paid for by insurance (or not insured at all).

Medical bills can include charges for:

- Doctor visits

- Emergency room visits

- Hospital stays

- Surgeries

- Ambulance rides

- Lab work & imaging (X-rays, MRIs, blood tests)

- Prescriptions

- Mental health services

What happens if a medical bill isn't paid

- Late fees may apply

- It can be sent to collections

- It can appear on your credit report if:

- It's over $500, and

- It's unpaid for 12+ months

What Is A Charge-Off?

A charge-off account is a debt that a lender has decided is unlikely to be collected, so they mark it as a loss in their accounting—but you still owe the money.

How a charge-off happens (simple timeline)

- You miss payments (usually 120–180 days late)

- The lender gives up trying to collect

- They charge off the account as a loss

- The debt may:

- Stay with the original lender, or

- Be sold to a collection agency

Important truths about charge-offs

- Not forgiven – you still legally owe the debt

- Not the same as a collection, but they often come together

- Very negative on your credit

- Can stay on your credit report for 7 years from first delinquency

What Is A Repossession?

A repossession (often called a repo) happens when a lender takes back property you're financing—most commonly a car—because payments weren't made as agreed.

How a repossession happens (simple timeline)

- You finance a vehicle (or other property)

- You miss payments (often 60–90 days late, varies by state & contract)

- The lender declares default

- The vehicle is repossessed (often without warning)

- The lender may:

- Sell the vehicle at auction

- Bill you for the remaining balance (deficiency balance)

Important things to know

- Repossession does NOT erase the debt

- It's a major negative on your credit

- It can stay on your credit report for 7 years from the first missed payment

- You may still owe money after the car is taken

Deficiency balance (very important)

If you owed $18,000 and the car sells for $11,000:

- $7,000 = deficiency balance

- Plus fees (towing, storage, auction costs)

- That balance can be sent to collections or charged off

Voluntary vs involuntary repossession

- Voluntary repo: You turn in the vehicle

- Involuntary repo: The lender takes it

⚠️ Credit impact is the same for both

What Is Bankruptcy?

A bankruptcy is a legal process that gives a person or business relief from overwhelming debt when they can no longer afford to pay what they owe.

90%+ of personal bankruptcies are either:

- Chapter 7

- Chapter 13

Everything else is rare and situational.

⚠️ Credit Impact (Quick Truth)

- Bankruptcy stays on your credit report 7–10 years

- Scores usually drop 150–350+ points

💳 Debts That DO Get Wiped Out (Usually)

These are called dischargeable debts:

- Credit cards

- Medical bills

- Personal loans

- Payday loans

- Collections & charge-offs

- Old utility bills

- Certain business debts

🚫 Debts That DO NOT Get Wiped Out (Usually)

These survive bankruptcy:

- Child support & alimony

- Most student loans

- Recent income taxes

- Court fines & criminal restitution

- Debts from fraud

- Most government-backed loans

Key things people misunderstand

- Paying a public record like bankruptcy for example does not automatically remove it from your credit report

- It doesn't disappear because it's old (until time limits expire)

- Removing it often requires legal accuracy disputes or completion

- Just because your bankruptcy has been Dismissed or discharged doesn't mean it will not report on your credit report

What Are Public Records?

A public record on a credit report is a negative legal or financial event that comes from court filings or government records and is reported to the credit bureaus because it involves unpaid obligations or legal responsibility.

Historically, these included:

- Bankruptcy (Chapter 7, 11, 13) ✅ still reported

- Judgments (court-ordered debts)

- Tax liens (unpaid federal or state taxes)

- Civil lawsuits

- Evictions

⚠️ Important update:

Today, bankruptcy is the main public record that still appears directly on credit reports. Most judgments, tax liens, and civil suits no longer appear due to reporting rule changes—but they can still exist in court records and affect things like employment, housing, or lending decisions.

How public records affect your credit

- Considered major derogatory items

- Can cause large score drops (100+ points)

- Signal high risk to lenders

- Stay on your credit report for a long time

How long public records stay on your credit

- Chapter 7 bankruptcy: 10 years

- Chapter 13 bankruptcy: 7 years (sometimes sooner if completed early)

- Other public records: Usually not reported anymore, but still legally valid elsewhere

Key things people misunderstand

- Paying a public record like bankruptcy for example does not automatically remove it

- It doesn't disappear because it's old (until time limits expire)

- Removing it often requires legal accuracy disputes or completion

What Is ChexSystems?

ChexSystems is a consumer reporting agency that banks and credit unions use to decide whether to approve or deny you for checking and savings accounts.

It's like a credit report—but for bank accounts, not loans or credit cards.

What ChexSystems tracks

ChexSystems collects information about negative banking activity, including:

- Unpaid overdrafts

- Negative balances left unpaid

- Account closures for cause

- Suspected fraud

- Excessive bounced checks

- Abandoned accounts with balances owed

It does NOT track credit cards, loans, or credit scores.

How it affects you

If you have negative info in ChexSystems, banks may:

- Deny you a checking or savings account

- You can NEVER Get a business loan while In chexsystems

- Require a second-chance account

- Limit features (no overdraft, no checks)

- Charge higher fees

- Won't qualify for pay in four options like Afterpay, Klarna, Acima, Zip, Affirm, PayPal Etc

This is why people say: "My credit is good, but the bank still denied me."

How long ChexSystems stays on your record

- Most negative items stay up to 5 years

- Even small amounts (like $50–$200) can block approvals

- Paying the debt does not automatically remove it

What People Don't Realize

If you are in chexsystems or early warning then that means that you have been violated. Read 15 USC 6802- 15 USC 6805. If you read your terms and conditions and privacy agreements of your credit card accounts banking information it tells you that they do not share your personal information with any 3rd party non affiliate….

Third Party Non-Affiliates Include:

- Lexis Nexis

- Experian

- Equifax

- Transunion

- Early Warning System

- ChexSystems

What we don't realize it when we open up these accounts we have the option to opt out so they don't share our information but they don't out right tell us that in plain English either. But in there privacy agreements and terms and conditions it states that they don't but yet they do anyway which is a violation.

What Is Early Warning Services?

Early Warning Services (often just called Early Warning or EWS) is a consumer reporting agency used by banks to decide whether to approve you for checking and savings accounts and to monitor for fraud.

It's similar to ChexSystems—but more powerful—and is heavily used by major banks.

What Early Warning tracks

Early Warning Services collects:

- Bank account openings & closures

- Unpaid negative balances

- Overdraft abuse

- Suspected fraud or identity risk

- Transaction behavior patterns

- Zelle-related activity

- Account misuse flags

Unlike ChexSystems, Early Warning is often real-time and behavior-based.

Many top U.S. banks rely on Early Warning, including:

- Chase

- Bank of America

- Wells Fargo

- Capital One

- PNC

If Early Warning flags you:

- You may be denied instantly

- No explanation from the bank

- Even "second-chance" accounts may be blocked

- Zelle can be restricted or shut down

How long Early Warning stays on your record

- Typically up to 5 years

- Fraud-related flags may last longer

- Paying a balance does not guarantee removal

What Is Debt Consolidation?

Debt consolidation is a financial strategy where you combine multiple debts into one single payment, usually with the goal of lowering your interest rate, reducing your monthly payment, or simplifying your finances.

Why people do it (what's advertised)

- One payment instead of many

- Lower interest rate (sometimes)

- Easier to stay organized

- Can help cash flow each month

Important downsides to know

- Does NOT erase debt — you still owe it

- Can hurt your credit if mismanaged

- Some options require good credit

- Risky if you rack up new debt afterward

- Secured options (like home equity) put assets at risk

🚨 Reasons Why I Don't Recommend Debt Consolidation

So whenever you apply for debt consolidation essentially all they will do is combine all of your debt into one big debt right? Now tell me what's stopping you from doing this yourself?

Then they will give you a monthly fee. And in most cases, debt consolidation does include interest. So you just made your debt even bigger.

What They Don't Tell You:

They don't actually start paying off any debt until everything is paid off. So if that's the case you could have just paid off everything over time yourself.

And to make matters worse — when it's all said and done any open accounts you had will be closed. And that doesn't benefit you at all.

My Recommendation:

I personally do not recommend debt consolidation at all, but debt settlement may be a better approach.

Help Your Kids Build Credit

Adding a child as an authorized user on your credit card can help them begin building their credit history early. This can lead to better credit offers, lower interest rates, auto loans, mortgages, and more as they get older.

Our parents weren't taught about credit—and that's not their fault. But today, we know better. You are responsible for your children's financial future. Getting a credit card with one of these banks and adding them as an authorized user can give your children the head start you never had.

Note: Authorized user reporting policies vary by issuer. Responsible use required.

How To Calculate Your Credit History / Age

Credit Age (also called Length of Credit History) makes up 15% of your credit score and is calculated using multiple factors, not just one account.

CREDIT AGE IS BASED ON:

1. Age of Oldest Account

- The very first account ever opened on your credit report

- Older = better

- This is why closing old accounts can hurt

2. Age of Newest Account

- Your most recently opened account

- Opening new accounts lowers your average age

3. Average Age of Accounts - MOST IMPORTANT

This is what most people miss.

Formula:

(Total age of all accounts) ÷ (Number of accounts)

Example: Let's Say You Only Have 3 Accounts On Your Credit Report

- Account A: 6 years Old

- Account B: 4 years Old

- Account C: 2 years Old

6+4+2 = A Total Of 12 years

12 ÷ 3 accounts = 4-year average credit age

4. Open AND Closed Accounts Count

- Closed accounts still count toward credit age

- They usually remain on your report for up to 10 years

- Once they fall off, your average age can drop

HOW LENDERS & BUREAUS SEE IT

All three bureaus calculate age slightly differently:

- Experian

- Equifax

- TransUnion

That's why one bureau may show 4.2 years while another may show 3.8 years. This is normal.

COMMON ROOKIE MISTAKES

- Closing old cards "because they don't use them"

- Opening too many accounts too fast

- Relying only on authorized user accounts

- Thinking a single old account = strong profile

IN CONCLUSION: Credit age is not about how old ONE account is. It's about how long you've been responsibly managing MULTIPLE accounts over time.

You can have one 10-year-old account and five brand new accounts... and still have a weak average credit age.

Banks & Lenders Like To See Profiles That Have 5 Or More Years Worth Of Credit History/Age

Credit Age Calculator (AAoA Estimator)

Add each account on your credit report (open + closed) and enter its age. The calculator will automatically compute your Average Age of Accounts (AAoA).

Note: This is an estimate. Credit bureaus may calculate age slightly differently and may include closed accounts until they fall off your report.